What is Global Semiconductor Solvent Market?

The Global Semiconductor Solvent Market is a crucial component of the semiconductor industry, which is integral to the production of electronic devices. Semiconductors are the building blocks of modern electronics, and solvents are essential in their manufacturing process. These solvents are used to clean and prepare semiconductor wafers, ensuring that they are free from contaminants that could affect the performance of the final product. The market for semiconductor solvents is driven by the increasing demand for electronic devices, such as smartphones, computers, and other consumer electronics, as well as the growing adoption of advanced technologies like artificial intelligence and the Internet of Things (IoT). As the semiconductor industry continues to evolve, the demand for high-quality solvents that can meet the stringent requirements of semiconductor manufacturing is expected to grow. This market is characterized by a focus on innovation and the development of new solvent formulations that can improve the efficiency and effectiveness of the semiconductor manufacturing process.

Ultra High Purity Reagents, Functional Chemicals in the Global Semiconductor Solvent Market:

Ultra High Purity (UHP) Reagents and Functional Chemicals are pivotal in the Global Semiconductor Solvent Market, serving as essential components in the intricate processes of semiconductor manufacturing. UHP reagents are chemicals that have been purified to the highest standards, ensuring that they contain minimal impurities. These reagents are crucial in the semiconductor industry because even the smallest amount of contamination can lead to defects in semiconductor devices, affecting their performance and reliability. The demand for UHP reagents is driven by the need for precision and accuracy in semiconductor manufacturing, as these reagents are used in processes such as etching, cleaning, and doping. Functional chemicals, on the other hand, are specialized chemicals that perform specific functions in the semiconductor manufacturing process. These chemicals are designed to enhance the performance of semiconductor devices by improving their electrical properties, thermal stability, and mechanical strength. The development of new functional chemicals is a key area of research and innovation in the semiconductor industry, as manufacturers seek to improve the performance and efficiency of their products. The use of UHP reagents and functional chemicals is essential in the production of advanced semiconductor devices, such as microprocessors, memory chips, and sensors, which are used in a wide range of applications, from consumer electronics to automotive and industrial systems. The Global Semiconductor Solvent Market is characterized by a focus on quality and innovation, with manufacturers investing in research and development to create new and improved solvent formulations that can meet the evolving needs of the semiconductor industry. As the demand for advanced semiconductor devices continues to grow, the importance of UHP reagents and functional chemicals in the semiconductor manufacturing process is expected to increase, driving the growth of the Global Semiconductor Solvent Market.

IDM Companies, Foundry Companies in the Global Semiconductor Solvent Market:

The Global Semiconductor Solvent Market plays a vital role in the operations of Integrated Device Manufacturers (IDM) and Foundry Companies, which are two key segments of the semiconductor industry. IDM companies are responsible for designing, manufacturing, and selling semiconductor products, while foundry companies focus on manufacturing semiconductor devices for other companies. Both types of companies rely heavily on semiconductor solvents to ensure the quality and performance of their products. In IDM companies, semiconductor solvents are used in various stages of the manufacturing process, including wafer cleaning, etching, and photoresist stripping. These solvents help to remove impurities and contaminants from the semiconductor wafers, ensuring that the final products meet the required specifications and performance standards. The use of high-quality solvents is essential in IDM companies, as any defects or impurities in the semiconductor devices can lead to performance issues and product failures. Foundry companies, on the other hand, use semiconductor solvents to manufacture semiconductor devices for other companies. These companies often work with a wide range of clients, each with their own specific requirements and specifications. As a result, foundry companies need to use a variety of solvents to meet the diverse needs of their clients. The use of semiconductor solvents in foundry companies is critical to ensuring the quality and performance of the semiconductor devices they produce. Both IDM and foundry companies are constantly seeking new and improved solvent formulations that can enhance the efficiency and effectiveness of their manufacturing processes. The Global Semiconductor Solvent Market is characterized by a focus on innovation and quality, with manufacturers investing in research and development to create new solvent formulations that can meet the evolving needs of the semiconductor industry. As the demand for advanced semiconductor devices continues to grow, the importance of semiconductor solvents in the operations of IDM and foundry companies is expected to increase, driving the growth of the Global Semiconductor Solvent Market.

Global Semiconductor Solvent Market Outlook:

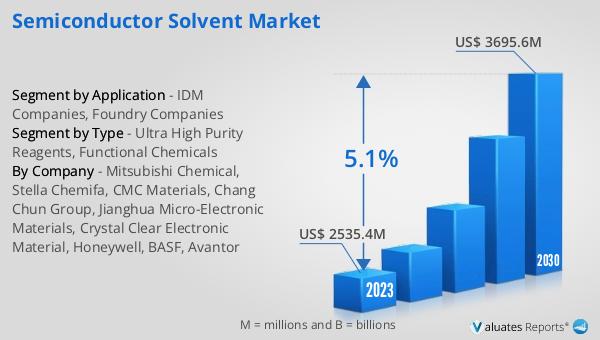

In 2024, the global market for semiconductor solvents was valued at approximately $2,737 million, with projections indicating that it will reach around $4,457 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 7.7% over the forecast period. The market is moderately concentrated, with the top five manufacturers—Mitsubishi Chemical, BASF, Chang Chun Group, Stella Chemifa, and Daicel—accounting for 27.01% of the market's revenue in 2024. This concentration reflects the competitive nature of the market, where a few key players hold significant market shares. These companies are likely to continue playing a crucial role in shaping the market dynamics, given their established presence and expertise in the industry. The growth of the semiconductor solvent market is driven by the increasing demand for electronic devices and the continuous advancements in semiconductor technology. As the industry evolves, the need for high-quality solvents that can meet the stringent requirements of semiconductor manufacturing is expected to grow, further driving the market's expansion. The focus on innovation and the development of new solvent formulations will be key factors in maintaining the market's growth trajectory.

| Report Metric | Details |

| Report Name | Semiconductor Solvent Market |

| Accounted market size in year | US$ 2737 million |

| Forecasted market size in 2031 | US$ 4457 million |

| CAGR | 7.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mitsubishi Chemical, BASF, Chang Chun Group, Stella Chemifa, Daicel, Crystal Clear Electronic Material, Shiny Chemical Industrial, Jianghua Micro-Electronic Materials, Honeywell, Dow Inc, Eastman, KH Neochem, Chemtronics, ICL Performance Products, LG Chem, Entegris, Jiangsu Dynamic Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |