What is Global High Temperature Heat Transfer Fluid Market?

The Global High Temperature Heat Transfer Fluid Market is a specialized segment within the broader industrial fluids market, focusing on fluids that can efficiently transfer heat at elevated temperatures. These fluids are essential in various industrial processes where heat needs to be transferred from one part of a system to another without losing efficiency or causing damage to the equipment. High temperature heat transfer fluids are used in applications where temperatures can exceed 300°C, making them crucial for industries such as oil and gas, chemical processing, and manufacturing. The market is driven by the increasing demand for energy-efficient solutions and the need for reliable thermal management in high-temperature applications. These fluids are designed to maintain their stability and performance under extreme conditions, ensuring that industrial processes run smoothly and efficiently. The market is characterized by a range of products, including synthetic and mineral-based fluids, each offering unique properties and benefits. As industries continue to seek ways to improve efficiency and reduce operational costs, the demand for high temperature heat transfer fluids is expected to grow, making this market an important area of focus for manufacturers and end-users alike.

Synthetic, Mineral in the Global High Temperature Heat Transfer Fluid Market:

In the Global High Temperature Heat Transfer Fluid Market, synthetic and mineral-based fluids play pivotal roles, each offering distinct advantages and applications. Synthetic heat transfer fluids are engineered to provide superior thermal stability, high-temperature performance, and extended service life. These fluids are typically composed of aromatic hydrocarbons, silicones, or other synthetic compounds that allow them to operate efficiently at temperatures exceeding 400°C. Their ability to maintain consistent thermal properties under extreme conditions makes them ideal for demanding applications in industries such as chemical processing, pharmaceuticals, and solar power generation. Synthetic fluids are also known for their low viscosity, which enhances their heat transfer efficiency and reduces energy consumption in pumping systems. Moreover, they exhibit excellent resistance to oxidation and thermal degradation, ensuring long-term reliability and reduced maintenance costs.

On the other hand, mineral-based heat transfer fluids are derived from refined petroleum products and are often used in applications where cost-effectiveness is a primary consideration. These fluids are typically composed of paraffinic or naphthenic hydrocarbons, which provide good thermal stability and heat transfer properties at moderate temperatures, usually up to 300°C. Mineral-based fluids are widely used in industries such as oil and gas, food processing, and plastics manufacturing, where the operating temperatures are within their optimal range. One of the key advantages of mineral-based fluids is their lower initial cost compared to synthetic alternatives, making them an attractive option for budget-conscious operations. However, they may require more frequent replacement and maintenance due to their susceptibility to oxidation and thermal breakdown at higher temperatures.

The choice between synthetic and mineral-based heat transfer fluids often depends on the specific requirements of the application, including temperature range, thermal stability, cost considerations, and environmental impact. Synthetic fluids, while more expensive upfront, offer longer service life and better performance at extreme temperatures, making them suitable for high-demand applications. In contrast, mineral-based fluids provide a cost-effective solution for less demanding environments, where moderate temperatures and shorter fluid lifespans are acceptable. Additionally, environmental considerations play a role in the selection process, as synthetic fluids are often more environmentally friendly due to their lower volatility and reduced emissions compared to mineral-based options.

As the Global High Temperature Heat Transfer Fluid Market continues to evolve, advancements in fluid technology are expected to enhance the performance and sustainability of both synthetic and mineral-based products. Manufacturers are investing in research and development to create fluids with improved thermal stability, lower environmental impact, and enhanced safety features. This ongoing innovation is likely to expand the range of applications for high temperature heat transfer fluids, further driving market growth and offering new opportunities for industries seeking efficient and reliable thermal management solutions.

Oil & Gas Industry, Chemical Industry, Pharmaceutical Industry, Food & Beverage Processing, Plastics & Rubber Manufacturing, Others in the Global High Temperature Heat Transfer Fluid Market:

The Global High Temperature Heat Transfer Fluid Market finds extensive usage across various industries, each with unique requirements and challenges. In the oil and gas industry, these fluids are crucial for maintaining optimal temperatures in processes such as refining, petrochemical production, and natural gas processing. High temperature heat transfer fluids ensure efficient heat exchange, which is vital for maximizing output and minimizing energy consumption. They help in maintaining the stability of the processes, reducing the risk of equipment failure, and ensuring the safety of operations in high-temperature environments.

In the chemical industry, high temperature heat transfer fluids are used in processes such as polymerization, distillation, and chemical synthesis. These fluids provide precise temperature control, which is essential for achieving the desired chemical reactions and product quality. The ability to operate at high temperatures without degrading ensures that chemical processes remain efficient and cost-effective. Additionally, the use of these fluids helps in reducing downtime and maintenance costs, as they are designed to withstand the harsh conditions of chemical processing.

The pharmaceutical industry also relies on high temperature heat transfer fluids for various applications, including the production of active pharmaceutical ingredients (APIs) and the sterilization of equipment. These fluids provide the necessary thermal stability and heat transfer efficiency required for maintaining the integrity of pharmaceutical processes. The use of high temperature heat transfer fluids ensures that the stringent quality and safety standards of the pharmaceutical industry are met, while also optimizing production efficiency.

In the food and beverage processing industry, high temperature heat transfer fluids are used in applications such as frying, baking, and pasteurization. These fluids help in maintaining consistent temperatures, which is crucial for ensuring product quality and safety. The ability to operate at high temperatures without affecting the taste or quality of the food products makes these fluids an essential component of food processing operations. Additionally, they contribute to energy efficiency and cost savings by reducing the need for frequent equipment maintenance and replacement.

Plastics and rubber manufacturing also benefit from the use of high temperature heat transfer fluids, particularly in processes such as extrusion, molding, and vulcanization. These fluids provide the necessary heat transfer capabilities to ensure uniform temperature distribution, which is critical for achieving the desired material properties and product quality. The use of high temperature heat transfer fluids in these industries helps in optimizing production processes, reducing energy consumption, and minimizing waste.

Beyond these industries, high temperature heat transfer fluids are used in a variety of other applications, including renewable energy systems, automotive manufacturing, and electronics production. In each of these areas, the fluids play a vital role in ensuring efficient heat transfer, maintaining process stability, and reducing operational costs. As industries continue to seek ways to improve efficiency and sustainability, the demand for high temperature heat transfer fluids is expected to grow, driving innovation and expansion in this dynamic market.

Global High Temperature Heat Transfer Fluid Market Outlook:

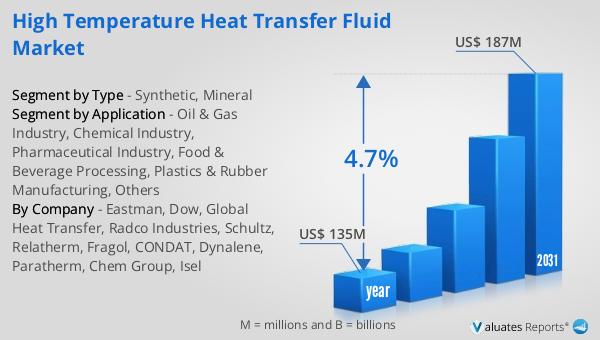

The global market for High Temperature Heat Transfer Fluid was valued at $135 million in 2024 and is anticipated to expand to a revised size of $187 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.7% during the forecast period. This growth trajectory underscores the increasing demand for efficient thermal management solutions across various industries. The market's expansion is driven by the need for reliable and high-performance heat transfer fluids that can operate under extreme temperature conditions. As industries such as oil and gas, chemical processing, and manufacturing continue to evolve, the demand for advanced heat transfer fluids is expected to rise, contributing to the market's growth.

The projected growth of the High Temperature Heat Transfer Fluid Market highlights the importance of these fluids in enhancing operational efficiency and reducing energy consumption. As industries strive to optimize their processes and reduce environmental impact, the adoption of high temperature heat transfer fluids is likely to increase. This growth is further supported by advancements in fluid technology, which are expected to improve the performance and sustainability of these products. As a result, the market is poised for significant expansion, offering new opportunities for manufacturers and end-users alike.

The anticipated growth in the market also reflects the broader trend towards energy efficiency and sustainability in industrial processes. As companies seek to reduce their carbon footprint and comply with environmental regulations, the demand for high-performance heat transfer fluids is expected to rise. This trend is likely to drive innovation in the market, leading to the development of new and improved fluid formulations that offer enhanced thermal stability, lower environmental impact, and improved safety features. Overall, the Global High Temperature Heat Transfer Fluid Market is set to experience robust growth, driven by the increasing demand for efficient and sustainable thermal management solutions.

| Report Metric |

Details |

| Report Name |

High Temperature Heat Transfer Fluid Market |

| Accounted market size in year |

US$ 135 million |

| Forecasted market size in 2031 |

US$ 187 million |

| CAGR |

4.7% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

- Oil & Gas Industry

- Chemical Industry

- Pharmaceutical Industry

- Food & Beverage Processing

- Plastics & Rubber Manufacturing

- Others

|

| Production by Region |

- North America

- Europe

- China

- Japan

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Eastman, Dow, Global Heat Transfer, Radco Industries, Schultz, Relatherm, Fragol, CONDAT, Dynalene, Paratherm, Chem Group, Isel |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |