What is Global Service Mesh Tools Software Market?

The Global Service Mesh Tools Software Market is a rapidly evolving sector within the broader field of cloud computing and microservices architecture. Service mesh tools are designed to manage and secure the communication between microservices, which are small, independent services that work together to form a larger application. These tools provide a dedicated infrastructure layer that handles service-to-service communication, offering features like load balancing, service discovery, and security. As businesses increasingly adopt microservices to enhance scalability and flexibility, the demand for service mesh tools has surged. These tools are crucial for ensuring that microservices can communicate efficiently and securely, without requiring changes to the application code. The market for these tools is driven by the growing complexity of IT environments and the need for robust solutions to manage this complexity. As organizations continue to transition to cloud-native architectures, the Global Service Mesh Tools Software Market is expected to expand significantly, providing essential support for modern application development and deployment.

Kubernetes, Other Environments in the Global Service Mesh Tools Software Market:

Kubernetes is a leading platform in the Global Service Mesh Tools Software Market, renowned for its ability to automate the deployment, scaling, and management of containerized applications. It provides a robust framework for running distributed systems resiliently, with features like self-healing, automated rollouts, and rollbacks. Kubernetes is particularly well-suited for managing microservices architectures, where applications are broken down into smaller, independent services. This modular approach allows for greater flexibility and scalability, as each service can be developed, deployed, and scaled independently. In the context of service mesh tools, Kubernetes plays a pivotal role by providing the underlying infrastructure that supports the deployment and management of these tools. Service mesh tools integrate seamlessly with Kubernetes, leveraging its capabilities to enhance service-to-service communication, security, and observability. Other environments in the Global Service Mesh Tools Software Market include cloud platforms like AWS, Azure, and Google Cloud, which offer managed Kubernetes services to simplify the deployment and management of containerized applications. These platforms provide a range of tools and services that complement service mesh tools, enabling organizations to build and manage complex microservices architectures with ease. Additionally, service mesh tools are increasingly being integrated with other cloud-native technologies, such as serverless computing and edge computing, to provide comprehensive solutions for modern application development. As the Global Service Mesh Tools Software Market continues to evolve, Kubernetes and other environments will play a critical role in shaping the future of cloud-native computing, providing the foundation for scalable, secure, and efficient application architectures.

Large Enterprises, SMEs in the Global Service Mesh Tools Software Market:

The usage of Global Service Mesh Tools Software Market varies significantly between large enterprises and small to medium-sized enterprises (SMEs), reflecting the diverse needs and challenges faced by these organizations. Large enterprises, with their complex IT environments and extensive microservices architectures, are the primary users of service mesh tools. These organizations require robust solutions to manage the communication between hundreds or even thousands of microservices, ensuring that their applications remain scalable, secure, and reliable. Service mesh tools provide the necessary infrastructure to handle this complexity, offering features like traffic management, security, and observability. For large enterprises, the ability to manage service-to-service communication efficiently is crucial for maintaining operational efficiency and delivering high-quality services to their customers. In contrast, SMEs often have simpler IT environments and may not require the full range of features offered by service mesh tools. However, as these organizations grow and adopt more complex architectures, the need for service mesh tools becomes more apparent. SMEs can benefit from the scalability and flexibility provided by these tools, enabling them to compete more effectively with larger organizations. By adopting service mesh tools, SMEs can streamline their operations, improve security, and enhance the performance of their applications. As the Global Service Mesh Tools Software Market continues to expand, both large enterprises and SMEs will increasingly rely on these tools to support their digital transformation efforts and drive business growth.

Global Service Mesh Tools Software Market Outlook:

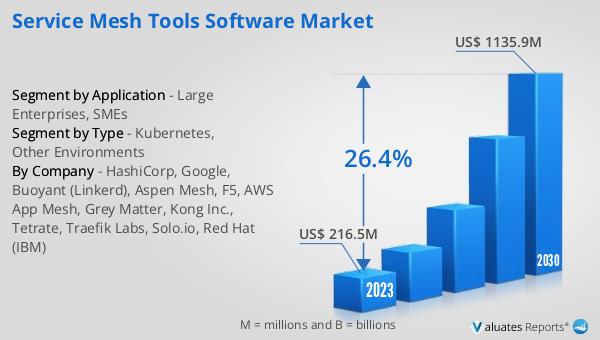

In 2024, the global market for Service Mesh Tools Software was valued at approximately $482 million. By 2031, it is anticipated to grow to a revised size of around $1,732 million, reflecting a compound annual growth rate (CAGR) of 19.8% over the forecast period. The large enterprises sector emerged as the most significant user of these tools, accounting for about 72.3% of the global market share. This dominance is attributed to the complex IT environments and extensive microservices architectures that large enterprises typically manage, necessitating robust solutions for service-to-service communication. North America was the leading region in the market, capturing approximately 65.3% of the global market share. This regional dominance can be linked to the high concentration of large enterprises and advanced technological infrastructure in North America, which drives the demand for service mesh tools. As organizations continue to embrace cloud-native architectures and microservices, the Global Service Mesh Tools Software Market is poised for substantial growth, with large enterprises and North America playing pivotal roles in shaping its trajectory.

| Report Metric | Details |

| Report Name | Service Mesh Tools Software Market |

| Accounted market size in year | US$ 482 million |

| Forecasted market size in 2031 | US$ 1732 million |

| CAGR | 19.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | HashiCorp, Google, Buoyant (Linkerd), IBM Red Hat, F5 (Aspen Mesh), AWS App Mesh, Grey Matter, Kong (Kuma), Tetrate, Traefik Labs, Solo.io |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |