What is Global Non-invasive Glucose Monitoring Device Market?

The Global Non-invasive Glucose Monitoring Device Market represents a significant advancement in diabetes management technology, offering a less intrusive way to monitor blood glucose levels. Unlike traditional methods that require finger pricking, non-invasive devices use innovative technologies such as optical sensors, electromagnetic waves, and ultrasound to measure glucose levels without penetrating the skin. This market is driven by the increasing prevalence of diabetes worldwide, coupled with a growing demand for more comfortable and convenient monitoring solutions. Non-invasive glucose monitoring devices are particularly appealing to individuals who require frequent monitoring, as they reduce the discomfort and inconvenience associated with traditional methods. The market is also fueled by technological advancements and increased investment in healthcare innovation. As awareness of diabetes management grows, so does the demand for these devices, which promise to improve the quality of life for millions of people living with diabetes. The market is expected to expand significantly as more people seek out these user-friendly and efficient monitoring solutions.

Wearable Devices, Non-wearable Devices in the Global Non-invasive Glucose Monitoring Device Market:

In the realm of the Global Non-invasive Glucose Monitoring Device Market, devices are broadly categorized into wearable and non-wearable types, each offering unique benefits and catering to different user needs. Wearable devices are designed to be worn on the body, often resembling a wristwatch or a patch, and continuously monitor glucose levels throughout the day. These devices use advanced sensors to detect glucose levels through the skin, providing real-time data that can be accessed via smartphones or other digital devices. The convenience of wearable devices lies in their ability to offer continuous monitoring without the need for manual intervention, making them ideal for active individuals or those who require constant glucose level tracking. They are particularly beneficial for people with busy lifestyles, as they can seamlessly integrate into daily routines without causing disruption. On the other hand, non-wearable devices are typically handheld or desktop devices that provide glucose readings on demand. These devices are often used in clinical settings or at home, where users can take readings at specific times. Non-wearable devices are generally more affordable than their wearable counterparts and are preferred by individuals who do not require continuous monitoring. They offer a practical solution for those who need to check their glucose levels periodically, such as before meals or bedtime. Both wearable and non-wearable devices are integral to the non-invasive glucose monitoring market, providing options that cater to diverse user preferences and needs. The choice between wearable and non-wearable devices often depends on factors such as lifestyle, budget, and the level of monitoring required. As technology continues to evolve, both types of devices are expected to become more sophisticated, offering enhanced accuracy and user experience. The competition between wearable and non-wearable devices drives innovation in the market, leading to the development of more advanced and user-friendly solutions. This dynamic market landscape ensures that individuals with diabetes have access to a range of options that can be tailored to their specific needs, ultimately improving diabetes management and quality of life.

Hospital, Home Care, Other in the Global Non-invasive Glucose Monitoring Device Market:

The usage of Global Non-invasive Glucose Monitoring Devices spans various settings, including hospitals, home care, and other environments, each benefiting from the unique advantages these devices offer. In hospitals, non-invasive glucose monitoring devices are used to provide continuous and accurate glucose readings for patients, reducing the need for frequent blood draws and minimizing discomfort. These devices are particularly useful in intensive care units, where patients require constant monitoring to manage their glucose levels effectively. The ability to obtain real-time data allows healthcare professionals to make timely and informed decisions regarding patient care, ultimately improving outcomes. In home care settings, non-invasive glucose monitoring devices empower individuals to manage their diabetes independently. These devices offer the convenience of monitoring glucose levels without the need for professional assistance, making them ideal for individuals who prefer to manage their condition in the comfort of their own homes. The ease of use and non-intrusive nature of these devices encourage regular monitoring, which is crucial for effective diabetes management. Additionally, non-invasive devices are beneficial for elderly patients or those with limited mobility, as they eliminate the need for frequent trips to healthcare facilities. Beyond hospitals and home care, non-invasive glucose monitoring devices find applications in other areas such as fitness centers and wellness programs. Athletes and fitness enthusiasts use these devices to monitor their glucose levels during workouts, ensuring optimal performance and recovery. The ability to track glucose levels in real-time allows individuals to make informed decisions about their diet and exercise routines, promoting overall health and well-being. Furthermore, non-invasive glucose monitoring devices are increasingly being integrated into corporate wellness programs, where employees can monitor their glucose levels as part of a broader health initiative. This integration not only promotes employee health but also reduces healthcare costs for employers by encouraging preventive care and early intervention. Overall, the versatility and convenience of non-invasive glucose monitoring devices make them an invaluable tool in various settings, enhancing diabetes management and improving quality of life for individuals worldwide.

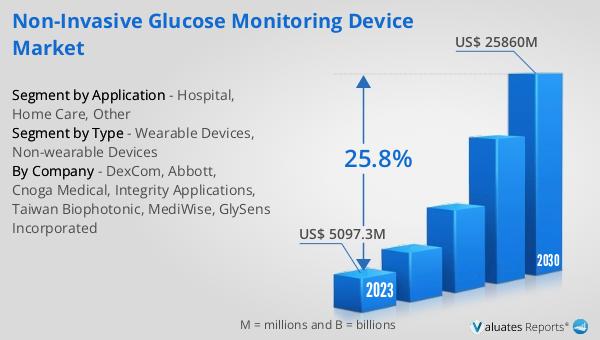

Global Non-invasive Glucose Monitoring Device Market Outlook:

The global market for non-invasive glucose monitoring devices was valued at approximately $12,256 million in 2024, and it is anticipated to grow significantly, reaching an estimated value of $31,463 million by 2031. This growth represents a compound annual growth rate (CAGR) of 14.1% over the forecast period. This impressive expansion is driven by several factors, including the increasing prevalence of diabetes, advancements in technology, and a growing demand for more comfortable and convenient glucose monitoring solutions. As more people become aware of the benefits of non-invasive monitoring, the market is expected to continue its upward trajectory. The shift towards non-invasive devices is largely due to the discomfort and inconvenience associated with traditional glucose monitoring methods, which require frequent finger pricking. Non-invasive devices offer a painless alternative, making them particularly appealing to individuals who require regular monitoring. Additionally, the integration of digital technology and real-time data tracking enhances the user experience, providing valuable insights into glucose levels and enabling better diabetes management. As the market continues to evolve, it is likely to see further innovation and development, leading to even more advanced and user-friendly solutions. This growth not only reflects the increasing demand for non-invasive glucose monitoring devices but also underscores the importance of continued investment in healthcare technology to improve the lives of individuals living with diabetes.

| Report Metric | Details |

| Report Name | Non-invasive Glucose Monitoring Device Market |

| Accounted market size in year | US$ 12256 million |

| Forecasted market size in 2031 | US$ 31463 million |

| CAGR | 14.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Abbott, DexCom, Medtronic, Senseonics Holdings, Cnoga Medical, Meiqi Medical, Medtrum Technologies, MicroTech Medical, POCTech, SIBIONICS, GHA Life, Infinovo Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |