What is Global Alkenyl Succinic Anhydride (ASA) Market?

The Global Alkenyl Succinic Anhydride (ASA) Market is a specialized segment within the chemical industry, focusing on the production and application of ASA compounds. These compounds are primarily used as sizing agents in the paper industry, where they help improve the water resistance and printability of paper products. ASA is also utilized in various other industries, including textiles, adhesives, and coatings, due to its ability to enhance the performance of materials. The market for ASA is driven by the growing demand for high-quality paper products and the increasing use of ASA in other industrial applications. The market is characterized by a few key players who dominate the production and distribution of ASA, ensuring a steady supply to meet the global demand. As industries continue to seek improved material performance and sustainability, the role of ASA in various applications is expected to grow, making it a critical component in the global chemical market.

HDSA, DDSA, ODSA, OSA, Others in the Global Alkenyl Succinic Anhydride (ASA) Market:

Alkenyl Succinic Anhydride (ASA) is a versatile chemical compound with several derivatives, including HDSA, DDSA, ODSA, and OSA, each serving distinct purposes in various industries. HDSA, or Hexadecenyl Succinic Anhydride, is primarily used in the paper industry as a sizing agent, enhancing the water resistance and printability of paper products. Its unique chemical structure allows it to bond effectively with cellulose fibers, making it an essential component in the production of high-quality paper. DDSA, or Dodecenyl Succinic Anhydride, is another important derivative, widely used as a curing agent in the production of epoxy resins. Its ability to improve the mechanical properties and thermal stability of resins makes it a preferred choice in the manufacturing of coatings, adhesives, and composites. ODSA, or Octadecenyl Succinic Anhydride, is known for its lubricating properties, making it suitable for use in the formulation of lubricants and greases. Its ability to reduce friction and wear in mechanical systems enhances the efficiency and longevity of machinery. OSA, or Octenyl Succinic Anhydride, is commonly used in the food industry as an emulsifier and stabilizer, helping to improve the texture and shelf life of various food products. Its compatibility with a wide range of ingredients makes it a valuable additive in the formulation of processed foods. The versatility of ASA derivatives extends beyond these applications, with each compound offering unique benefits that cater to the specific needs of different industries. As the demand for high-performance materials continues to rise, the role of ASA and its derivatives in enhancing the properties of various products is becoming increasingly important. The global market for ASA is characterized by a few key players who dominate the production and distribution of these compounds, ensuring a steady supply to meet the growing demand. With advancements in chemical technology and a focus on sustainability, the development of new ASA derivatives and applications is expected to drive further growth in the market. The ability of ASA compounds to improve the performance and sustainability of materials makes them a critical component in the global chemical industry, with applications spanning across multiple sectors.

Sizing Agent, Curing Agent, Lubricant, Others in the Global Alkenyl Succinic Anhydride (ASA) Market:

The Global Alkenyl Succinic Anhydride (ASA) Market finds its usage in several key areas, including as a sizing agent, curing agent, lubricant, and in other applications. As a sizing agent, ASA is predominantly used in the paper industry to enhance the water resistance and printability of paper products. By forming a hydrophobic layer on the surface of paper fibers, ASA improves the durability and quality of paper, making it suitable for a wide range of applications, from packaging to printing. This property is particularly valuable in the production of high-quality paper products, where performance and appearance are critical. In the realm of curing agents, ASA plays a vital role in the production of epoxy resins. Its ability to enhance the mechanical properties and thermal stability of resins makes it an essential component in the manufacturing of coatings, adhesives, and composites. The use of ASA as a curing agent ensures that the final products exhibit superior strength, durability, and resistance to environmental factors, making them suitable for demanding industrial applications. As a lubricant, ASA is used in the formulation of lubricants and greases, where its ability to reduce friction and wear in mechanical systems is highly valued. By improving the efficiency and longevity of machinery, ASA-based lubricants contribute to the overall performance and reliability of industrial equipment. Beyond these primary applications, ASA is also used in various other industries, including textiles, adhesives, and coatings, where its unique chemical properties enhance the performance and sustainability of materials. The versatility of ASA makes it a valuable additive in the formulation of a wide range of products, catering to the specific needs of different industries. As the demand for high-performance materials continues to grow, the role of ASA in enhancing the properties of various products is becoming increasingly important. The global market for ASA is characterized by a few key players who dominate the production and distribution of these compounds, ensuring a steady supply to meet the growing demand. With advancements in chemical technology and a focus on sustainability, the development of new ASA applications is expected to drive further growth in the market. The ability of ASA to improve the performance and sustainability of materials makes it a critical component in the global chemical industry, with applications spanning across multiple sectors.

Global Alkenyl Succinic Anhydride (ASA) Market Outlook:

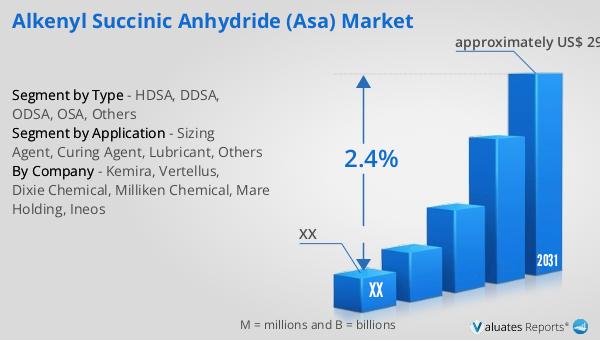

In 2024, the global market size of Alkenyl Succinic Anhydride (ASA) was valued at approximately US$ 249 million. It is projected to grow to around US$ 292 million by 2031, reflecting a compound annual growth rate (CAGR) of 2.4% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold a share exceeding 90%. North America emerges as the largest market, accounting for about 50% of the global share, followed by China, which holds approximately 20%. Among the various products, DDSA stands out as the largest segment, capturing about 40% of the market share. This data highlights the significant role of ASA in various industrial applications and underscores the importance of key players in driving market growth. The dominance of North America and China in the market reflects the strong demand for ASA in these regions, driven by the need for high-performance materials in industries such as paper, coatings, and adhesives. The projected growth of the ASA market indicates a continued focus on enhancing material performance and sustainability, with DDSA playing a crucial role in meeting these demands. As the market evolves, the development of new applications and derivatives is expected to further drive growth and innovation in the ASA industry.

| Report Metric | Details |

| Report Name | Alkenyl Succinic Anhydride (ASA) Market |

| Forecasted market size in 2031 | approximately US$ 292 million |

| CAGR | 2.4% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kemira, Vertellus, Dixie Chemical, Milliken Chemical, Mare Holding, Ineos |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |