What is Global Oil Free Compressor Market?

The global oil-free compressor market is a specialized segment within the broader compressor industry, focusing on compressors that operate without the need for oil lubrication. These compressors are designed to deliver clean, oil-free air, which is crucial for applications where air purity is essential. The market for oil-free compressors is driven by the increasing demand for clean and contaminant-free compressed air in various industries such as food and beverage, pharmaceuticals, and electronics. These compressors are particularly valued for their ability to reduce the risk of oil contamination, which can compromise product quality and safety. Additionally, oil-free compressors are often more environmentally friendly and require less maintenance compared to their oil-lubricated counterparts. The market is characterized by a range of compressor types, including rotary screw, reciprocating, and centrifugal compressors, each offering unique advantages depending on the specific application. As industries continue to prioritize sustainability and efficiency, the demand for oil-free compressors is expected to grow, supported by technological advancements and the increasing adoption of stringent regulatory standards regarding air quality. The global oil-free compressor market is thus poised for significant growth, driven by its critical role in ensuring clean and efficient industrial operations.

Rotary Screw Compressors, Reciprocating Type, Centrifugal Type, Others in the Global Oil Free Compressor Market:

Rotary screw compressors, reciprocating type compressors, centrifugal compressors, and other types of compressors each play a significant role in the global oil-free compressor market, catering to diverse industrial needs. Rotary screw compressors are widely used due to their efficiency and reliability. They operate by using two meshing helical screws, known as rotors, to compress air. This type of compressor is favored for continuous operation and is often employed in large industrial applications where a constant supply of compressed air is required. Their oil-free variants are particularly popular in industries where air purity is paramount, such as food processing and pharmaceuticals, as they ensure that the compressed air is free from oil contamination. Reciprocating type compressors, on the other hand, use a piston driven by a crankshaft to deliver air at high pressure. These compressors are known for their ability to deliver high-pressure air and are often used in applications requiring intermittent use, such as in automotive workshops and small manufacturing units. Oil-free reciprocating compressors are essential in environments where even the slightest oil contamination can lead to product spoilage or equipment malfunction. Centrifugal compressors, meanwhile, utilize a rotating impeller to impart velocity to the air, which is then converted into pressure. These compressors are typically used in large-scale industrial applications due to their ability to handle high volumes of air. The oil-free versions are crucial in industries like electronics and power generation, where the presence of oil can lead to significant operational issues. Other types of oil-free compressors include scroll compressors and diaphragm compressors, each offering unique benefits. Scroll compressors, for instance, are known for their quiet operation and are often used in medical and laboratory settings where noise reduction is important. Diaphragm compressors, which use a flexible diaphragm to compress air, are ideal for applications requiring ultra-clean air, such as in the chemical and pharmaceutical industries. The diversity of compressor types within the oil-free segment highlights the market's adaptability to various industrial requirements, ensuring that businesses can find the right solution for their specific needs. As industries continue to evolve and prioritize clean and efficient operations, the demand for these oil-free compressor types is expected to remain robust, driven by their ability to deliver reliable and contaminant-free compressed air.

Chemical Industry, Oil & Gas Industry, Power Generation, Electronics Industry, Medical and Pharma., Food and Beverage Industry, Automobile & Auto Ancillaries, Others in the Global Oil Free Compressor Market:

The global oil-free compressor market finds extensive usage across a wide range of industries, each benefiting from the unique advantages these compressors offer. In the chemical industry, oil-free compressors are essential for ensuring that the compressed air used in processes is free from oil contamination, which can lead to chemical reactions and compromise product quality. Similarly, in the oil and gas industry, these compressors are used to provide clean air for instrumentation and control systems, where even trace amounts of oil can cause malfunctions. In power generation, oil-free compressors are crucial for maintaining the integrity of air systems used in turbines and other equipment, ensuring efficient and reliable operation. The electronics industry also relies heavily on oil-free compressors, as the presence of oil in compressed air can lead to defects in sensitive electronic components. In the medical and pharmaceutical sectors, the demand for oil-free compressors is driven by the need for sterile and contaminant-free air, which is vital for manufacturing processes and maintaining the integrity of medical equipment. The food and beverage industry similarly benefits from oil-free compressors, as they ensure that the air used in packaging and processing is free from contaminants, thereby safeguarding product quality and safety. In the automobile and auto ancillaries sector, oil-free compressors are used in painting and finishing processes, where oil contamination can lead to defects in the final product. Other industries, such as textiles and pulp and paper, also utilize oil-free compressors to ensure clean and efficient operations. The versatility and reliability of oil-free compressors make them an indispensable tool across these diverse sectors, supporting the growing demand for clean and efficient industrial processes. As industries continue to prioritize sustainability and quality, the usage of oil-free compressors is expected to expand, driven by their ability to deliver reliable and contaminant-free compressed air.

Global Oil Free Compressor Market Outlook:

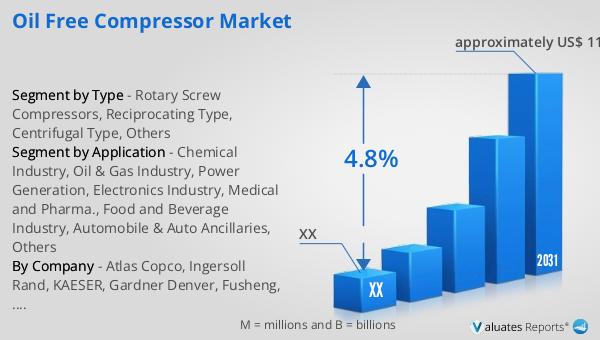

In 2024, the global market size for oil-free compressors was valued at approximately $814 million, with projections indicating it could reach around $1,128 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.8% during the forecast period from 2025 to 2031. The market is dominated by five major manufacturers: Atlas Copco, Ingersoll Rand, Hitachi, Kobelco, and Fusheng, which collectively account for over 60% of the market share. Among these, Atlas Copco leads with nearly 40% of the production value share, followed by Ingersoll Rand at 20% and Hitachi at 7%. The Asia-Pacific region is the largest market, holding a share of over 40%, followed by Europe and North America, with shares of 27% and 20%, respectively. Rotary screw compressors are the leading type, capturing a market share of over 55%. The chemical industry represents the largest segment, accounting for over 15% of the market. This data underscores the significant role of oil-free compressors in various industries and regions, highlighting their importance in ensuring clean and efficient operations. As the demand for oil-free compressors continues to grow, driven by the need for clean and contaminant-free compressed air, the market is poised for further expansion, supported by technological advancements and the increasing adoption of stringent regulatory standards regarding air quality.

| Report Metric | Details |

| Report Name | Oil Free Compressor Market |

| Forecasted market size in 2031 | approximately US$ 1128 million |

| CAGR | 4.8% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Atlas Copco, Ingersoll Rand, KAESER, Gardner Denver, Fusheng, Kobelco, Boge, Aerzen, Mitsui, Hitachi |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |