What is Global Fiber Optic Cables Market?

The global fiber optic cables market is a dynamic and rapidly evolving sector that plays a crucial role in modern telecommunications and data transmission. Fiber optic cables are made of thin strands of glass or plastic fibers that transmit data as light signals, offering high-speed and high-capacity data transfer capabilities. These cables are essential for various applications, including internet services, cable television, and telecommunications, due to their ability to carry large amounts of data over long distances with minimal signal loss. The market is driven by the increasing demand for high-speed internet and the growing need for efficient data transmission in both developed and developing regions. Technological advancements and the expansion of telecommunication infrastructure further fuel the market's growth. Additionally, the rising adoption of fiber optic cables in industries such as healthcare, defense, and energy is contributing to the market's expansion. As the world becomes more interconnected, the demand for reliable and fast data transmission continues to rise, making fiber optic cables an integral part of the global communication infrastructure. The market is characterized by intense competition among key players, with continuous innovations and strategic partnerships shaping its future landscape.

Single-Mode, Multi-Mode in the Global Fiber Optic Cables Market:

In the global fiber optic cables market, two primary types of cables are widely used: single-mode and multi-mode. Single-mode fiber optic cables are designed for long-distance communication, offering a smaller core diameter that allows only one mode of light to propagate. This design minimizes signal attenuation and dispersion, making single-mode cables ideal for transmitting data over vast distances with high bandwidth capabilities. They are commonly used in telecommunication networks, internet backbones, and long-haul data transmission, where maintaining signal integrity over long distances is crucial. The demand for single-mode fiber optic cables is driven by the increasing need for high-speed internet and the expansion of telecommunication infrastructure worldwide. On the other hand, multi-mode fiber optic cables have a larger core diameter, allowing multiple modes of light to propagate simultaneously. This design is suitable for shorter distance communication, such as within buildings or campus networks, where high data transfer rates are required over relatively short distances. Multi-mode cables are often used in local area networks (LANs), data centers, and enterprise networks, where cost-effectiveness and ease of installation are important considerations. The choice between single-mode and multi-mode fiber optic cables depends on factors such as distance, bandwidth requirements, and budget constraints. While single-mode cables offer superior performance for long-distance communication, multi-mode cables provide a cost-effective solution for short-distance applications. The global fiber optic cables market is witnessing a growing demand for both single-mode and multi-mode cables, driven by the increasing need for efficient data transmission in various sectors. As technology continues to advance, the market is expected to see further innovations in fiber optic cable design and manufacturing, enhancing their performance and expanding their applications. The competition among manufacturers is intense, with companies focusing on developing advanced fiber optic solutions to meet the evolving needs of the market. Strategic partnerships and collaborations are also playing a significant role in shaping the market dynamics, as companies seek to leverage each other's strengths and expand their market presence. The global fiber optic cables market is poised for significant growth, driven by the increasing demand for high-speed internet, the expansion of telecommunication infrastructure, and the rising adoption of fiber optic cables in various industries. As the world becomes more interconnected, the importance of reliable and efficient data transmission continues to grow, making fiber optic cables an essential component of the global communication infrastructure.

Long-Distance Communication, FTTx, Local Mobile Metro Network, Other Local Access Network, CATV, Multimode Fiber Applications, Others in the Global Fiber Optic Cables Market:

The global fiber optic cables market finds extensive usage across various sectors, each benefiting from the unique advantages offered by fiber optic technology. In long-distance communication, fiber optic cables are indispensable due to their ability to transmit data over vast distances with minimal signal loss. This makes them ideal for telecommunication networks and internet backbones, where maintaining signal integrity is crucial. Fiber optic cables are also widely used in FTTx (Fiber to the x) applications, which involve delivering fiber optic connections directly to homes, buildings, or other premises. This enhances internet speed and reliability, catering to the growing demand for high-speed broadband services. In local mobile metro networks, fiber optic cables play a vital role in supporting the increasing data traffic generated by mobile devices. They provide the necessary bandwidth and speed to handle the surge in data transmission, ensuring seamless connectivity and improved network performance. Additionally, fiber optic cables are used in other local access networks, where they facilitate efficient data transfer and communication. In the CATV (Cable Television) industry, fiber optic cables are employed to deliver high-quality video and audio signals, offering superior performance compared to traditional coaxial cables. The use of fiber optic cables in multimode fiber applications is also significant, particularly in data centers and enterprise networks, where high data transfer rates are required over shorter distances. These cables provide a cost-effective solution for short-distance communication, ensuring efficient data transmission within buildings or campus networks. Furthermore, fiber optic cables find applications in various other sectors, including healthcare, defense, and energy, where reliable and fast data transmission is essential. The global fiber optic cables market is driven by the increasing demand for high-speed internet, the expansion of telecommunication infrastructure, and the rising adoption of fiber optic technology in diverse industries. As the world becomes more interconnected, the need for efficient data transmission continues to grow, making fiber optic cables a critical component of modern communication systems. The market is characterized by intense competition among key players, with continuous innovations and strategic partnerships shaping its future landscape. As technology advances, the market is expected to see further developments in fiber optic cable design and manufacturing, enhancing their performance and expanding their applications.

Global Fiber Optic Cables Market Outlook:

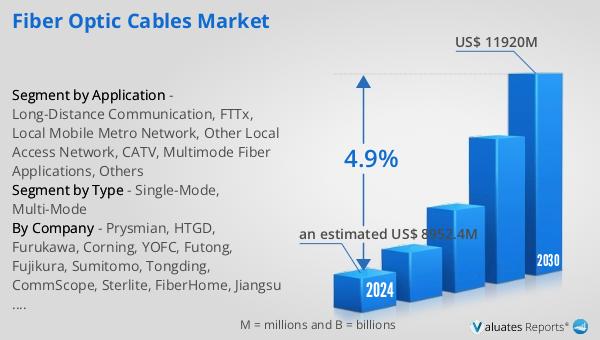

In 2024, the global fiber optic cables market was valued at approximately USD 9,346 million, with projections indicating a rise to around USD 12,980 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.9% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 40% of the market share. The Asia-Pacific region emerges as the largest market, accounting for over 60% of the global share, followed by North America, which holds approximately 16%. In terms of product segmentation, single-mode fiber optic cables represent the largest segment, capturing over 97% of the market share. This dominance is attributed to the increasing demand for high-speed internet and the expansion of telecommunication infrastructure, particularly in the Asia-Pacific region. The market's growth is further fueled by technological advancements and the rising adoption of fiber optic cables in various industries, including healthcare, defense, and energy. As the world becomes more interconnected, the demand for reliable and efficient data transmission continues to rise, making fiber optic cables an essential component of the global communication infrastructure. The market is characterized by intense competition among key players, with continuous innovations and strategic partnerships shaping its future landscape.

| Report Metric | Details |

| Report Name | Fiber Optic Cables Market |

| Forecasted market size in 2031 | approximately US$ 12980 million |

| CAGR | 4.9% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Prysmian, HTGD, Furukawa, Corning, YOFC, Futong, Fujikura, Sumitomo, Tongding, CommScope, Sterlite, FiberHome, Jiangsu Etern, ZTT, Belden, Nexans, Kaile, LS Cable&System |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |