What is Global Sutures Needle Market?

The Global Sutures Needle Market is a crucial segment of the medical devices industry, focusing on the production and distribution of needles used in surgical suturing. These needles are essential tools in various surgical procedures, enabling the precise closure of wounds and incisions. The market encompasses a wide range of needle types, each designed for specific surgical applications, including general surgery, cardiovascular procedures, and cosmetic surgeries, among others. The demand for sutures needles is driven by the increasing number of surgical procedures worldwide, advancements in surgical techniques, and the growing emphasis on patient safety and surgical outcomes. Additionally, the rise in chronic diseases and the aging population contribute to the market's expansion, as these factors lead to a higher volume of surgeries. The market is characterized by continuous innovation, with manufacturers focusing on developing needles that offer enhanced precision, reduced tissue trauma, and improved handling characteristics. As healthcare systems globally strive to improve surgical outcomes and reduce recovery times, the Global Sutures Needle Market plays a vital role in supporting these objectives by providing high-quality, reliable surgical tools.

Corner Needle, Shovel Needle, Straight Needle, Round Needle, Other in the Global Sutures Needle Market:

In the Global Sutures Needle Market, various types of needles are utilized, each serving distinct purposes in surgical procedures. Corner needles are specifically designed for suturing in tight or difficult-to-reach areas, such as the corners of wounds or incisions. Their unique shape allows surgeons to maneuver easily in confined spaces, ensuring precise closure and minimizing the risk of complications. Shovel needles, on the other hand, are characterized by their flat, broad design, which is particularly useful in procedures requiring the suturing of large, flat surfaces. This design provides stability and control, allowing for even distribution of tension across the suture line, which is crucial in maintaining the integrity of the wound closure. Straight needles are among the most commonly used types in the market, known for their versatility and ease of use. They are ideal for straightforward suturing tasks, providing a direct path through tissue, which simplifies the suturing process and reduces the likelihood of needle breakage. Round needles, another significant segment in the market, are designed with a circular cross-section, making them suitable for delicate tissues where minimizing tissue trauma is essential. These needles are often used in cardiovascular and ophthalmic surgeries, where precision and care are paramount. The round design allows for smooth passage through tissue, reducing the risk of tearing or damage. Other types of needles in the market include specialized designs tailored for specific surgical applications, such as cutting needles for tougher tissues or taper-point needles for soft, easily penetrable tissues. Each type of needle is crafted with precision, using high-quality materials to ensure durability, sharpness, and reliability during surgical procedures. The diversity of needle types in the Global Sutures Needle Market reflects the complexity and variety of surgical needs, highlighting the importance of having the right tool for each specific task. As surgical techniques continue to evolve, the demand for specialized needles is expected to grow, driving further innovation and development in the market.

Hospital, Clinic, ASCs in the Global Sutures Needle Market:

The usage of sutures needles in hospitals, clinics, and ambulatory surgical centers (ASCs) is integral to the delivery of effective surgical care. In hospitals, sutures needles are used extensively across various departments, including general surgery, orthopedics, cardiology, and obstetrics. Hospitals, being the primary centers for complex and high-risk surgeries, rely heavily on a wide range of sutures needles to cater to diverse surgical needs. The availability of different needle types ensures that surgeons can select the most appropriate tool for each procedure, enhancing surgical precision and patient outcomes. In clinics, where minor surgical procedures and wound care are more common, sutures needles are essential for tasks such as stitching small lacerations, performing biopsies, and conducting minor cosmetic surgeries. Clinics often require needles that are versatile and easy to handle, as they cater to a broad spectrum of procedures with varying levels of complexity. The use of sutures needles in clinics is crucial for ensuring quick and effective wound closure, minimizing the risk of infection, and promoting faster healing. Ambulatory surgical centers (ASCs) represent a growing segment in the healthcare industry, offering a convenient and cost-effective alternative to hospital-based surgeries. ASCs perform a wide range of outpatient procedures, from orthopedic surgeries to gastrointestinal endoscopies, and rely on sutures needles for efficient and precise wound closure. The use of high-quality sutures needles in ASCs is vital for maintaining surgical standards and ensuring patient safety, as these centers often handle a high volume of procedures with quick turnaround times. The demand for sutures needles in ASCs is driven by the increasing preference for outpatient surgeries, which offer shorter recovery times and reduced healthcare costs. Across all these settings, the Global Sutures Needle Market plays a critical role in supporting surgical practices by providing reliable and effective tools that meet the diverse needs of healthcare providers.

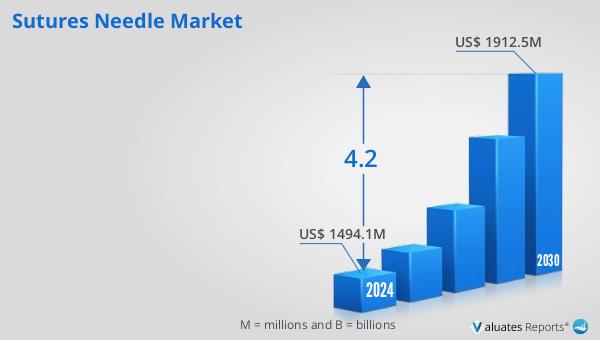

Global Sutures Needle Market Outlook:

In 2024, the global market size for sutures needles was valued at approximately US$ 1,551 million, with projections indicating a growth to around US$ 2,060 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 65% of the market share. North America emerges as the largest regional market, accounting for approximately 35% of the total market share, followed closely by Europe with a 30% share. Among the various product segments, the round needle stands out as the largest, capturing about 40% of the market. This data underscores the significant role of the Global Sutures Needle Market in the healthcare industry, driven by the increasing demand for surgical procedures and the continuous advancements in surgical techniques. The market's growth trajectory reflects the ongoing efforts to enhance surgical outcomes and patient safety, with manufacturers focusing on innovation and quality to meet the evolving needs of healthcare providers worldwide. As the market continues to expand, it is poised to play a pivotal role in supporting the global healthcare system by providing essential tools for surgical care.

| Report Metric | Details |

| Report Name | Sutures Needle Market |

| CAGR | 4.2% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Johnson & Johnson, Medtronic, B.Braun, Teleflex, Hu-Friedy, Peters Surgical, Shanghai Jinhuan, Aurolab, WEIHAI WEGO, FSSB, Kono Seisakusho, DemeTech, Dolphin (Futura Surgicare), Gore Medical, Unik Surgical Sutures MFG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |