What is Global Ether Amine Market?

The Global Ether Amine Market is a dynamic and rapidly evolving sector within the chemical industry. Ether amines are a type of amine compound characterized by the presence of an ether group. These compounds are primarily used as curing agents in epoxy resins, which are essential in various industrial applications due to their excellent mechanical properties and chemical resistance. The market for ether amines is driven by their increasing demand in industries such as construction, automotive, and electronics, where they are used to enhance the performance and durability of products. Additionally, the rise in shale gas exploration activities has further boosted the demand for ether amines, as they are used in the formulation of shale gas fracturing fluids. The market is also witnessing growth due to advancements in technology and the development of new applications for ether amines. As industries continue to seek materials that offer superior performance and sustainability, the Global Ether Amine Market is poised for significant growth in the coming years.

Poly Ether Amine MW 230, Poly Ether Amine MW 2000, Poly Ether Amine MW 400, Other in the Global Ether Amine Market:

Poly Ether Amine MW 230, Poly Ether Amine MW 2000, and Poly Ether Amine MW 400 are specific types of ether amines that vary in molecular weight and are used for different applications based on their unique properties. Poly Ether Amine MW 230 is a low molecular weight amine that is often used in applications requiring fast curing times and high reactivity. Its low viscosity makes it ideal for use in coatings and adhesives where quick setting is essential. On the other hand, Poly Ether Amine MW 2000 is a high molecular weight amine that provides flexibility and toughness to the materials it is used in. This makes it suitable for applications in the production of flexible foams, elastomers, and sealants. Its ability to impart elasticity and resilience is highly valued in industries such as automotive and construction, where materials are subjected to dynamic stresses. Poly Ether Amine MW 400 falls between the two in terms of molecular weight and offers a balance of properties. It is commonly used in applications that require a moderate level of flexibility and toughness, such as in the production of coatings and adhesives. The versatility of these poly ether amines allows them to be tailored to specific applications, making them valuable components in the formulation of high-performance materials. Other ether amines in the market also play significant roles in various applications. These include specialty amines that are designed for specific industrial processes or to meet particular performance criteria. The diversity of ether amines available in the market enables manufacturers to select the most appropriate compound for their needs, ensuring optimal performance and efficiency in their products. As the demand for high-performance materials continues to grow across various industries, the role of poly ether amines in meeting these demands becomes increasingly important. Their ability to enhance the properties of materials, such as strength, flexibility, and chemical resistance, makes them indispensable in the development of advanced industrial products.

Epoxy Coating, Polyurea, Shale Gas Fracturing Fluid, Fuel Additives in the Global Ether Amine Market:

The Global Ether Amine Market finds extensive usage in several key areas, including epoxy coatings, polyurea, shale gas fracturing fluid, and fuel additives. In the realm of epoxy coatings, ether amines serve as crucial curing agents that facilitate the hardening process of epoxy resins. This results in coatings that are not only durable but also resistant to chemicals and environmental degradation. Such properties are essential in industries like construction and automotive, where protective coatings are required to withstand harsh conditions and extend the lifespan of structures and vehicles. In polyurea applications, ether amines contribute to the formation of elastomeric coatings and linings that offer exceptional flexibility and abrasion resistance. These coatings are widely used in infrastructure projects, such as bridges and tunnels, where they provide a protective barrier against moisture and corrosion. The rapid curing time of polyurea coatings, facilitated by ether amines, also allows for quick application and minimal downtime, making them highly desirable in time-sensitive projects. In the energy sector, ether amines play a pivotal role in the formulation of shale gas fracturing fluids. These fluids are essential in the hydraulic fracturing process, where they help to create fractures in rock formations, allowing for the extraction of natural gas. Ether amines enhance the performance of fracturing fluids by improving their viscosity and stability, ensuring efficient gas extraction. Additionally, in the realm of fuel additives, ether amines are used to improve the performance and efficiency of fuels. They help to reduce engine deposits, enhance combustion, and improve fuel economy, making them valuable in the automotive and aviation industries. The versatility and effectiveness of ether amines in these diverse applications underscore their importance in the Global Ether Amine Market. As industries continue to seek innovative solutions to enhance product performance and sustainability, the demand for ether amines is expected to grow, driving further advancements and applications in this dynamic market.

Global Ether Amine Market Outlook:

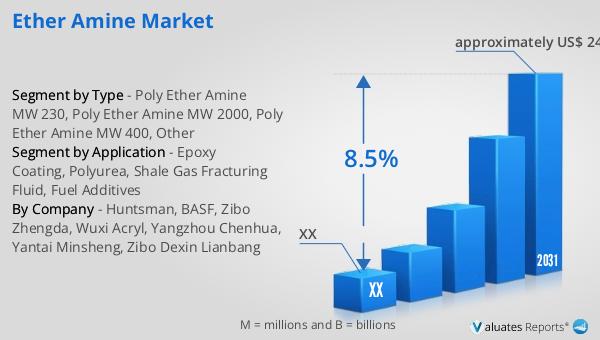

In 2024, the global market for Ether Amine was valued at approximately USD 1,390 million. Looking ahead, it is projected to expand significantly, reaching an estimated value of around USD 2,441 million by 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 8.5% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold a substantial share of about 90%. Geographically, North America and Asia are the largest markets for ether amines, each accounting for approximately 35% of the global market share. Europe follows closely, with a market share of about 25%. This distribution highlights the widespread demand for ether amines across different regions, driven by their diverse applications in industries such as construction, automotive, and energy. The robust growth forecast for the Global Ether Amine Market underscores the increasing importance of these compounds in various industrial applications. As manufacturers continue to innovate and develop new uses for ether amines, the market is poised for continued expansion, offering significant opportunities for growth and development in the coming years.

| Report Metric | Details |

| Report Name | Ether Amine Market |

| Forecasted market size in 2031 | approximately US$ 2441 million |

| CAGR | 8.5% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Huntsman, BASF, Zibo Zhengda, Wuxi Acryl, Yangzhou Chenhua, Yantai Minsheng, Zibo Dexin Lianbang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |