What is Global Vitamin B1 (Thiamine Mononitrate) Market?

The Global Vitamin B1 (Thiamine Mononitrate) Market is a significant segment within the broader nutritional and pharmaceutical industries. Thiamine, also known as Vitamin B1, is an essential nutrient that plays a crucial role in energy metabolism and the proper functioning of the nervous system. The market for Vitamin B1, particularly in its mononitrate form, is driven by its widespread application across various sectors, including food and beverages, pharmaceuticals, animal feed, and cosmetics. The demand for Vitamin B1 is primarily fueled by the increasing awareness of health and wellness among consumers, leading to a higher consumption of dietary supplements and fortified foods. Additionally, the growing prevalence of lifestyle-related diseases has prompted a surge in the use of Vitamin B1 in pharmaceutical formulations. The market is characterized by a high concentration of manufacturers, with the top four companies holding a significant share. Geographically, China dominates the market, accounting for the majority of the global production and consumption, followed by Europe. The market is expected to continue its growth trajectory, driven by ongoing research and development activities aimed at enhancing the bioavailability and efficacy of Vitamin B1 products.

Thiamine Nitrate Type, Thiamine Hydrochloride Type in the Global Vitamin B1 (Thiamine Mononitrate) Market:

Thiamine Nitrate and Thiamine Hydrochloride are two primary types of Vitamin B1 used in the global market, each with distinct characteristics and applications. Thiamine Nitrate is a stable, water-soluble form of Vitamin B1 that is commonly used in dietary supplements and fortified foods. Its stability makes it an ideal choice for products that require a longer shelf life. Thiamine Nitrate is particularly favored in the food industry due to its ability to withstand high temperatures during processing, ensuring that the vitamin's potency is retained in the final product. This form of Vitamin B1 is also used in the pharmaceutical industry, where it is incorporated into various formulations to treat and prevent thiamine deficiency-related conditions such as beriberi and Wernicke-Korsakoff syndrome. On the other hand, Thiamine Hydrochloride is another water-soluble form of Vitamin B1, known for its rapid absorption and bioavailability. It is often used in clinical settings for the treatment of acute thiamine deficiency, as it can quickly replenish thiamine levels in the body. Thiamine Hydrochloride is also used in the production of injectable solutions, providing a fast-acting option for patients in need of immediate supplementation. In the animal feed industry, both Thiamine Nitrate and Thiamine Hydrochloride are used to enhance the nutritional profile of feed products, supporting the growth and health of livestock. The choice between these two forms of Vitamin B1 often depends on the specific requirements of the application, such as stability, absorption rate, and cost-effectiveness. Despite their differences, both Thiamine Nitrate and Thiamine Hydrochloride play a crucial role in meeting the global demand for Vitamin B1, contributing to the overall growth of the market.

Feed Additive, Food Additive, Pharmaceutical, Supplement and Cosmetics in the Global Vitamin B1 (Thiamine Mononitrate) Market:

The Global Vitamin B1 (Thiamine Mononitrate) Market finds extensive usage across various sectors, including feed additives, food additives, pharmaceuticals, supplements, and cosmetics. In the feed additive industry, Vitamin B1 is used to enhance the nutritional value of animal feed, promoting healthy growth and development in livestock. It plays a vital role in energy metabolism, helping animals convert carbohydrates into energy, which is essential for their overall health and productivity. In the food additive sector, Vitamin B1 is commonly used to fortify processed foods, such as cereals, bread, and pasta, to ensure that consumers receive adequate levels of this essential nutrient. The fortification of foods with Vitamin B1 is particularly important in regions where dietary intake may be insufficient, helping to prevent deficiencies and associated health issues. In the pharmaceutical industry, Vitamin B1 is used in the formulation of various medications and supplements aimed at treating and preventing thiamine deficiency-related conditions. It is also used in combination with other B vitamins to support overall health and well-being. In the supplement industry, Vitamin B1 is a popular ingredient in multivitamin formulations, catering to the growing consumer demand for health and wellness products. Finally, in the cosmetics industry, Vitamin B1 is used for its antioxidant properties, helping to protect the skin from oxidative stress and improve its overall appearance. The versatility of Vitamin B1 and its wide range of applications make it a valuable component in various industries, driving the growth of the global market.

Global Vitamin B1 (Thiamine Mononitrate) Market Outlook:

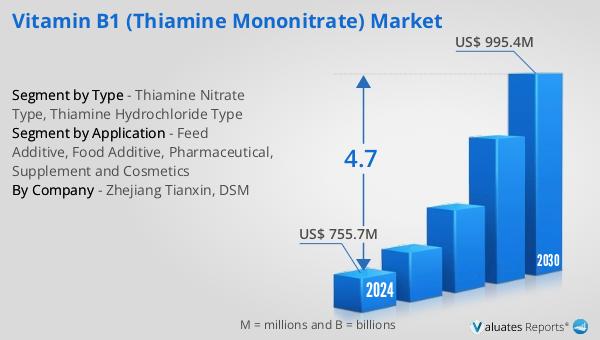

In 2024, the global market size for Vitamin B1 Thiamine Mononitrate was valued at approximately US$ 788 million, with projections indicating it could reach around US$ 1081 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.7% during the forecast period from 2025 to 2031. The market is highly concentrated, with the top four manufacturers collectively holding about 95% of the market share. China emerges as the largest market, commanding a significant share of approximately 90%, followed by Europe, which holds around 10% of the market. In terms of product segmentation, the Thiamine Nitrate Type is the most prominent, accounting for about 70% of the market share. This dominance is attributed to its stability and suitability for various applications, making it a preferred choice among manufacturers and consumers alike. The market dynamics are influenced by factors such as increasing health awareness, the rising prevalence of lifestyle-related diseases, and the growing demand for dietary supplements and fortified foods. As the market continues to evolve, manufacturers are focusing on research and development to enhance the efficacy and bioavailability of Vitamin B1 products, catering to the diverse needs of consumers across the globe.

| Report Metric | Details |

| Report Name | Vitamin B1 (Thiamine Mononitrate) Market |

| CAGR | 4.7% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Brother Enterprises, Huazhong Pharma, Zhejiang Tianxin, DSM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |