What is Global Brass Bars Market?

The Global Brass Bars Market is a significant segment within the metal industry, characterized by its diverse applications and widespread demand across various sectors. Brass bars are primarily composed of copper and zinc, offering a unique combination of strength, corrosion resistance, and workability. These properties make brass bars an essential material in manufacturing and construction. The market for brass bars is driven by their extensive use in producing components for machinery, automotive parts, and electrical appliances. Additionally, the aesthetic appeal of brass, with its golden hue, makes it a popular choice for decorative applications. The global market is influenced by factors such as industrial growth, technological advancements, and the increasing demand for durable and efficient materials. As industries continue to evolve, the need for high-quality brass bars is expected to rise, further propelling market growth. The market is also shaped by the presence of key manufacturers who play a crucial role in meeting the global demand and setting industry standards. Overall, the Global Brass Bars Market is poised for steady growth, driven by its versatile applications and the ongoing expansion of end-use industries.

Ordinary Brass Bars, Neutral Brass Bars, High Precision Brass Bars in the Global Brass Bars Market:

Ordinary Brass Bars, Neutral Brass Bars, and High Precision Brass Bars each serve distinct roles within the Global Brass Bars Market, catering to various industrial needs. Ordinary Brass Bars are the most commonly used type, known for their excellent machinability and moderate strength. They are typically used in applications where high corrosion resistance is not a primary concern, such as in plumbing fixtures, musical instruments, and low-stress mechanical components. Their ease of fabrication and cost-effectiveness make them a popular choice for general-purpose applications. On the other hand, Neutral Brass Bars offer a balanced composition that provides a good mix of strength, ductility, and corrosion resistance. These bars are often used in environments where moderate exposure to corrosive elements is expected, such as in marine hardware and architectural fittings. Their versatility makes them suitable for a wide range of applications, from decorative items to functional components in various industries. High Precision Brass Bars, as the name suggests, are engineered for applications requiring high dimensional accuracy and superior surface finish. These bars are used in precision engineering, where tight tolerances and high performance are critical, such as in the manufacturing of intricate components for the aerospace and electronics industries. The production of high precision brass bars involves advanced manufacturing techniques to ensure consistency and quality, making them a premium choice for specialized applications. The demand for each type of brass bar is influenced by the specific requirements of the end-use industries, with factors such as mechanical properties, environmental conditions, and cost considerations playing a crucial role in determining the choice of material. As industries continue to innovate and develop new technologies, the need for specialized brass bars is expected to grow, driving further advancements in the production and application of these materials. The Global Brass Bars Market is thus characterized by its diversity, with each type of brass bar offering unique benefits and catering to specific industrial needs.

Machines, Automotive, Electric Appliances in the Global Brass Bars Market:

The usage of brass bars in machines, automotive, and electric appliances highlights the versatility and importance of this material in modern manufacturing. In the machinery sector, brass bars are valued for their excellent machinability and durability. They are used to produce components such as gears, bearings, and valves, where precision and reliability are paramount. The ability of brass to withstand wear and tear, coupled with its resistance to corrosion, makes it an ideal choice for machine parts that operate under high stress and in challenging environments. In the automotive industry, brass bars play a crucial role in the production of various components, including radiator cores, fuel systems, and connectors. The material's thermal conductivity and resistance to corrosion are particularly beneficial in automotive applications, where performance and longevity are critical. Brass bars are also used in the manufacturing of decorative elements, such as trim and badges, due to their aesthetic appeal and ease of fabrication. In the realm of electric appliances, brass bars are essential for producing electrical connectors, terminals, and switches. The excellent electrical conductivity of brass ensures efficient power transmission, while its durability and resistance to oxidation contribute to the longevity of electrical components. The use of brass in electric appliances is driven by the need for reliable and efficient materials that can withstand the demands of modern technology. Overall, the Global Brass Bars Market is integral to the functioning of machines, automotive, and electric appliances, providing essential materials that enhance performance, durability, and efficiency across these sectors. As industries continue to evolve and demand more advanced and reliable materials, the role of brass bars in these applications is expected to grow, further solidifying their importance in the global market.

Global Brass Bars Market Outlook:

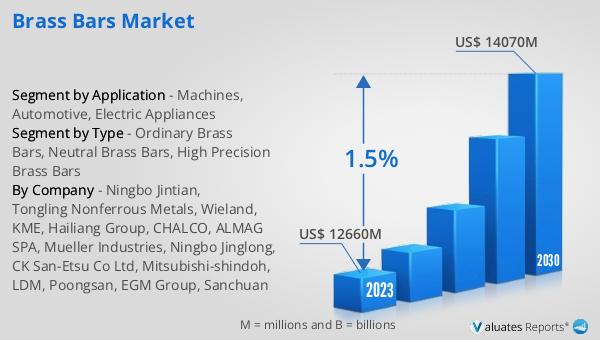

In 2024, the global market size of brass bars was estimated to be valued at approximately US$ 13,040 million, with projections indicating a growth to around US$ 14,450 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 1.5% during the forecast period from 2025 to 2031. Key players in the industry include Ningbo Jintian, Tongling Nonferrous Metals, Wieland, KME, and ALMAG SPA, who collectively hold about 50% of the market share among the top 10 manufacturers. These companies are instrumental in shaping the market dynamics, leveraging their expertise and resources to meet the growing demand for brass bars across various industries. The market's steady growth can be attributed to the increasing demand for durable and efficient materials in sectors such as machinery, automotive, and electrical appliances. As these industries continue to expand and innovate, the need for high-quality brass bars is expected to rise, further driving market growth. The presence of key manufacturers ensures a competitive landscape, fostering innovation and the development of new products to meet the evolving needs of end-users. Overall, the Global Brass Bars Market is poised for steady growth, supported by the ongoing expansion of key industries and the strategic efforts of leading manufacturers.

| Report Metric | Details |

| Report Name | Brass Bars Market |

| CAGR | 1.5% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ningbo Jintian, Tongling Nonferrous Metals, Wieland, KME, Hailiang Group, CHALCO, ALMAG SPA, Mueller Industries, Ningbo Jinglong, CK San-Etsu Co Ltd, Mitsubishi-shindoh, LDM, Poongsan, EGM Group, Sanchuan |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |