What is Global Progressing Cavity Pumps Market?

The Global Progressing Cavity Pumps Market is a dynamic and essential segment within the broader industrial equipment landscape. Progressing cavity pumps, also known as screw pumps, are specialized devices designed to handle a variety of fluids, including those with high viscosity or containing solids. These pumps operate on the principle of positive displacement, where a helical rotor turns within a double helix stator, creating cavities that move the fluid from the pump's inlet to its outlet. This unique mechanism allows for a smooth, non-pulsating flow, making them ideal for applications requiring precise fluid handling. The market for these pumps is driven by their versatility and efficiency in industries such as oil and gas, water and wastewater management, and food and beverage processing. As industries continue to seek reliable and efficient pumping solutions, the demand for progressing cavity pumps is expected to grow, supported by technological advancements and the need for sustainable and energy-efficient systems. The market's expansion is also influenced by the increasing focus on infrastructure development and the need for effective fluid management solutions across various sectors.

Dosing Pump, Flanged Pump, Hopper Pump, Food Grade, Others in the Global Progressing Cavity Pumps Market:

Progressing cavity pumps are categorized into several types based on their design and application, including dosing pumps, flanged pumps, hopper pumps, food-grade pumps, and others. Dosing pumps are precision devices used to inject a specific volume of fluid into a process stream. They are crucial in applications where accurate dosing of chemicals or additives is required, such as in water treatment, chemical processing, and pharmaceuticals. These pumps ensure that the right amount of fluid is delivered consistently, which is vital for maintaining process integrity and product quality. Flanged pumps, on the other hand, are designed with flanged connections, making them suitable for integration into existing piping systems. They are commonly used in industrial settings where robust and secure connections are necessary to prevent leaks and ensure operational safety. Hopper pumps are equipped with a hopper at the inlet, allowing them to handle highly viscous or solid-laden fluids. This design makes them ideal for applications in the food and beverage industry, where they can efficiently transport thick pastes, slurries, and other challenging materials. Food-grade pumps are specifically designed to meet the stringent hygiene and safety standards required in food processing. They are constructed from materials that are safe for contact with food products and are easy to clean and maintain. These pumps play a critical role in ensuring that food products are handled safely and efficiently throughout the production process. Other types of progressing cavity pumps include specialized designs for niche applications, such as those used in the oil and gas industry for handling crude oil and other hydrocarbons. Each type of pump offers unique advantages and is selected based on the specific requirements of the application, such as flow rate, pressure, and fluid characteristics. The versatility and adaptability of progressing cavity pumps make them a valuable asset in a wide range of industries, providing reliable and efficient solutions for fluid handling challenges.

Oil & Gas, Food & Beverage, Water & Wastewater Management, Others in the Global Progressing Cavity Pumps Market:

The Global Progressing Cavity Pumps Market finds extensive application across various industries, including oil and gas, food and beverage, water and wastewater management, and others. In the oil and gas sector, these pumps are used for the extraction and transportation of crude oil, natural gas, and other hydrocarbons. Their ability to handle high-viscosity fluids and solids makes them ideal for pumping crude oil from wells, especially in challenging environments where other pump types may struggle. The smooth, non-pulsating flow provided by progressing cavity pumps ensures efficient and reliable operation, reducing the risk of downtime and maintenance costs. In the food and beverage industry, these pumps are used to transport a wide range of products, from liquids to highly viscous materials like dough, pastes, and slurries. Their gentle handling of products helps maintain the quality and integrity of food items, making them an essential component in food processing and production lines. The pumps' hygienic design and ease of cleaning also make them suitable for applications where food safety is a top priority. In water and wastewater management, progressing cavity pumps are used for the transfer of sludge, slurry, and other challenging fluids. Their ability to handle abrasive and corrosive materials makes them ideal for use in wastewater treatment plants, where they help in the efficient processing and disposal of waste materials. The pumps' robust construction and reliable performance ensure that they can withstand the harsh conditions often encountered in these environments. Other industries that benefit from the use of progressing cavity pumps include chemical processing, pharmaceuticals, and mining. In each of these sectors, the pumps provide a reliable and efficient solution for handling a wide range of fluids, contributing to improved operational efficiency and reduced costs. The versatility and adaptability of progressing cavity pumps make them a valuable asset in any industry where fluid handling is a critical component of the production process.

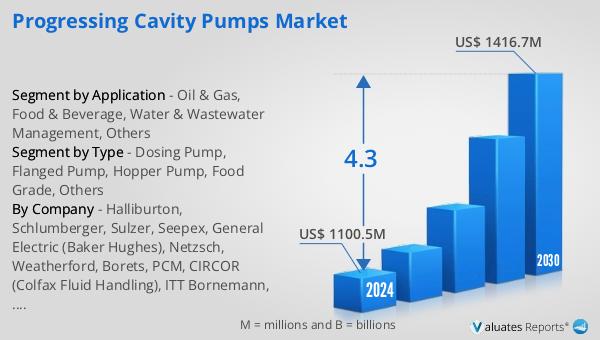

Global Progressing Cavity Pumps Market Outlook:

In 2024, the global market size for Progressing Cavity Pumps was valued at approximately US$ 1,088 million. It is projected to grow to around US$ 1,442 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.1% during the forecast period from 2025 to 2031. This growth is driven by the increasing demand for efficient and reliable fluid handling solutions across various industries. North America stands out as the largest consumer of progressing cavity pumps, accounting for about 30% of the global market share. This dominance is attributed to the region's well-established industrial base and the ongoing need for advanced pumping solutions in sectors such as oil and gas, water and wastewater management, and food and beverage processing. The market's expansion in North America is further supported by technological advancements and the adoption of energy-efficient systems. As industries continue to prioritize sustainability and operational efficiency, the demand for progressing cavity pumps is expected to rise, contributing to the market's overall growth. The market outlook for progressing cavity pumps remains positive, with opportunities for growth and innovation across various regions and industries.

| Report Metric | Details |

| Report Name | Progressing Cavity Pumps Market |

| CAGR | 4.1% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | PCM, Schlumberger, Sulzer, Seepex, Baker Hughes, Netzsch, Weatherford, Levare International, CIRCOR, ITT Bornemann, THE VERDER, Csf, JOHSTADT, Pumpenfabrik Wangen, Nova rotors, VARISCO, BELLIN, Sydex, Lutz Pumpen, mono (NOV), Xinglong Pump, Shanhai Sunshine Pump, Zhejiang Nanchi Pump, Jiangsu Huaqiang Pump, Mingjie Pump, Tianjin Pump Machinery Group Co., Ltd. (CTP), RSP Manufacturing |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |