What is Global Organic Dairy Products Market?

The Global Organic Dairy Products Market is a rapidly growing segment within the broader dairy industry, driven by increasing consumer awareness and demand for healthier, environmentally friendly, and ethically produced food options. Organic dairy products are derived from livestock that are raised according to organic farming standards, which typically include the absence of synthetic pesticides, fertilizers, antibiotics, and growth hormones. These products are perceived as healthier alternatives to conventional dairy products, as they are believed to contain higher levels of beneficial nutrients such as omega-3 fatty acids, antioxidants, and vitamins. The market encompasses a wide range of products, including liquid milk, milk powder, cheese, butter, and ice cream, all of which are produced using organic methods. The growth of this market is fueled by factors such as rising health consciousness, increasing disposable incomes, and a growing preference for organic food products. Additionally, stringent regulations and certifications ensure the authenticity and quality of organic dairy products, further boosting consumer confidence and market growth. As more consumers prioritize sustainability and animal welfare, the Global Organic Dairy Products Market is expected to continue its upward trajectory, offering a diverse array of products to meet the evolving needs of health-conscious consumers worldwide.

Liquid Milk, Milk Powder, Cheese & Butter, Ice Cream in the Global Organic Dairy Products Market:

Liquid milk is one of the most prominent segments within the Global Organic Dairy Products Market. It is a staple in many households and is consumed daily by millions of people around the world. Organic liquid milk is produced from cows that are fed organic feed and are not treated with synthetic hormones or antibiotics. This ensures that the milk is free from harmful chemicals and is rich in essential nutrients. The demand for organic liquid milk is driven by consumers' growing awareness of the health benefits associated with organic products, as well as concerns about the environmental impact of conventional dairy farming. Milk powder, another significant segment, is a versatile product used in various applications, including infant formula, confectionery, and bakery products. Organic milk powder is produced by evaporating water from organic liquid milk, resulting in a shelf-stable product that retains the nutritional benefits of fresh milk. The demand for organic milk powder is increasing due to its convenience, long shelf life, and the rising popularity of organic infant formula. Cheese and butter are also key products in the organic dairy market. Organic cheese is made from milk that comes from cows raised on organic farms, ensuring that the cheese is free from artificial additives and preservatives. The variety of organic cheeses available, from cheddar to mozzarella, caters to diverse consumer preferences. Organic butter, known for its rich flavor and creamy texture, is made from the cream of organic milk. It is a popular choice among consumers who prefer natural and wholesome ingredients in their cooking and baking. Lastly, organic ice cream is a growing segment within the market, appealing to consumers who seek indulgent treats made from high-quality, organic ingredients. Organic ice cream is made using organic milk, cream, and natural flavorings, offering a delicious and guilt-free dessert option. The increasing demand for organic dairy products across these categories is a testament to the shifting consumer preferences towards healthier and more sustainable food choices.

in the Global Organic Dairy Products Market:

The Global Organic Dairy Products Market finds applications across various sectors, driven by the increasing demand for organic and sustainable food options. One of the primary applications is in the retail sector, where organic dairy products are sold in supermarkets, health food stores, and online platforms. Consumers are increasingly seeking organic options for their daily dairy needs, including milk, cheese, butter, and yogurt, due to the perceived health benefits and environmental advantages. The foodservice industry is another significant application area, with restaurants, cafes, and catering services incorporating organic dairy products into their menus to cater to health-conscious customers. Organic dairy products are used in a wide range of dishes, from coffee and smoothies to gourmet meals, enhancing the flavor and nutritional value of the offerings. The bakery and confectionery industry also utilizes organic dairy products, such as milk, butter, and cream, to create high-quality baked goods and sweets that appeal to consumers looking for natural and wholesome ingredients. Additionally, the infant nutrition sector is a crucial application area, with organic milk powder being a key ingredient in organic infant formula. Parents are increasingly opting for organic options for their babies, driven by concerns about the potential health risks associated with conventional dairy products. The cosmetics and personal care industry is another emerging application area, with organic dairy ingredients being used in skincare and haircare products for their nourishing and moisturizing properties. Overall, the diverse applications of organic dairy products across these sectors highlight the growing consumer preference for organic and sustainable options, driving the expansion of the Global Organic Dairy Products Market.

Global Organic Dairy Products Market Outlook:

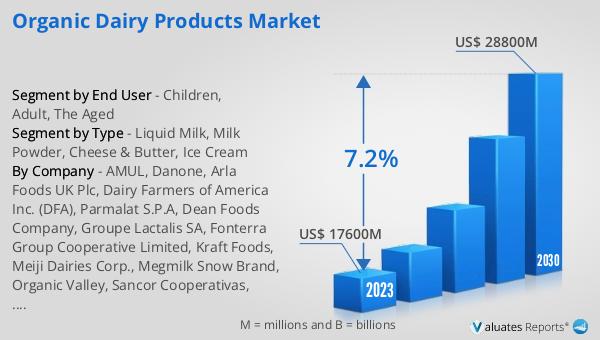

In 2024, the global market size for Organic Dairy Products was valued at approximately US$ 20,200 million. This market is projected to grow significantly, reaching an estimated value of around US$ 32,650 million by 2031, with a compound annual growth rate (CAGR) of 7.2% during the forecast period from 2025 to 2031. North America stands as the largest producer of Organic Dairy Products, holding a substantial market share of about 55%. Following closely is Europe, which accounts for approximately 35% of the market share. The industry is dominated by key players such as Danone, Arla Foods Plc., Dairy Farmers of America Inc., Parmalat S.P.A, and Groupe Lactalis SA, who collectively hold around 40% of the market share. These companies have established themselves as leaders in the industry, leveraging their expertise and resources to meet the growing demand for organic dairy products. The market's growth is driven by increasing consumer awareness of the health benefits associated with organic products, as well as the rising demand for sustainable and ethically produced food options. As consumers continue to prioritize health and sustainability, the Global Organic Dairy Products Market is poised for continued expansion, offering a wide range of products to meet the evolving needs of consumers worldwide.

| Report Metric | Details |

| Report Name | Organic Dairy Products Market |

| CAGR | 7.2% |

| Segment by Type |

|

| Segment by End User |

|

| By Region |

|

| By Company | AMUL, Danone, Arla Foods UK Plc, Dairy Farmers of America Inc. (DFA), Parmalat S.P.A, Dean Foods Company, Groupe Lactalis SA, Fonterra Group Cooperative Limited, Kraft Foods, Meiji Dairies Corp., Megmilk Snow Brand, Organic Valley, Sancor Cooperativas, Royal FrieslandCampina N.V., Unilever |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |