What is Global Bar Type Display Market?

The Global Bar Type Display Market refers to a specialized segment within the broader display technology industry, focusing on elongated, narrow screens that are often used in environments where traditional display formats are impractical. These displays are characterized by their unique aspect ratios, which make them ideal for specific applications such as digital signage, transportation, and advertising. Unlike conventional displays, bar type displays are designed to fit into tight spaces and provide information in a clear and concise manner. They are commonly used in public transportation systems, retail environments, and industrial settings where space is limited but information needs to be conveyed effectively. The market for these displays is driven by the increasing demand for innovative and space-efficient display solutions across various industries. As technology advances, the capabilities of bar type displays continue to expand, offering higher resolutions, better color accuracy, and enhanced durability. This makes them an attractive option for businesses looking to improve their communication and engagement with customers. The Global Bar Type Display Market is expected to grow significantly in the coming years, driven by technological advancements and the increasing adoption of digital signage solutions worldwide.

Less than 28 Inches, 28 Inches ~ 38 Inches, More than 38 Inches in the Global Bar Type Display Market:

In the Global Bar Type Display Market, the size of the display plays a crucial role in determining its application and effectiveness. Displays that are less than 28 inches are typically used in environments where space is extremely limited, such as in small retail stores, kiosks, or on public transportation vehicles like buses and trains. These smaller displays are ideal for providing essential information such as schedules, advertisements, or product details in a compact format. They are designed to be energy-efficient and cost-effective, making them a popular choice for businesses looking to implement digital signage without a significant investment. Displays that range from 28 inches to 38 inches offer a balance between size and visibility, making them suitable for a wider range of applications. These displays are often used in larger retail environments, airports, and train stations where they can provide more detailed information without taking up too much space. The increased size allows for better visibility from a distance, making them ideal for displaying advertisements, wayfinding information, or real-time updates. Displays that are more than 38 inches are typically used in environments where visibility is a top priority. These larger displays are often found in airports, shopping malls, and large public venues where they can capture the attention of a large audience. The increased size allows for more detailed and dynamic content, making them ideal for advertising and promotional purposes. These displays are often equipped with advanced features such as touch interactivity, high-resolution graphics, and robust connectivity options, allowing businesses to engage with their audience in innovative ways. The choice of display size in the Global Bar Type Display Market is largely determined by the specific needs of the application and the environment in which it will be used. Businesses must consider factors such as viewing distance, content type, and installation space when selecting the appropriate display size for their needs. As the market continues to evolve, manufacturers are developing new technologies and features to enhance the performance and versatility of bar type displays, making them an increasingly attractive option for businesses across various industries.

Transportation, Advertising, Others in the Global Bar Type Display Market:

The Global Bar Type Display Market finds extensive usage across various sectors, with transportation, advertising, and other industries being the primary areas of application. In the transportation sector, bar type displays are commonly used in public transit systems, including buses, trains, and subways, to provide passengers with real-time information such as schedules, route maps, and service updates. These displays are designed to be durable and reliable, capable of withstanding the rigors of daily use in high-traffic environments. Their elongated shape allows them to fit seamlessly into the limited space available in vehicles, making them an ideal solution for conveying important information to passengers. In the advertising sector, bar type displays are used to create dynamic and eye-catching digital signage that can capture the attention of consumers in retail environments, shopping malls, and public spaces. Their unique aspect ratio allows for creative content presentation, enabling businesses to deliver targeted messages and promotions effectively. These displays can be integrated with advanced technologies such as touch interactivity and motion sensors, allowing for engaging and interactive advertising experiences. In addition to transportation and advertising, bar type displays are also used in a variety of other applications, including industrial settings, hospitality, and healthcare. In industrial environments, they are used to display critical information such as production metrics, safety alerts, and equipment status updates. In the hospitality industry, bar type displays are used for wayfinding, menu boards, and event information, enhancing the guest experience by providing clear and concise information. In healthcare settings, these displays are used to convey important information to patients and staff, such as appointment schedules, wayfinding directions, and health alerts. The versatility and adaptability of bar type displays make them a valuable tool for businesses looking to improve communication and engagement with their audience. As technology continues to advance, the capabilities of these displays are expected to expand, offering new opportunities for innovation and growth in the Global Bar Type Display Market.

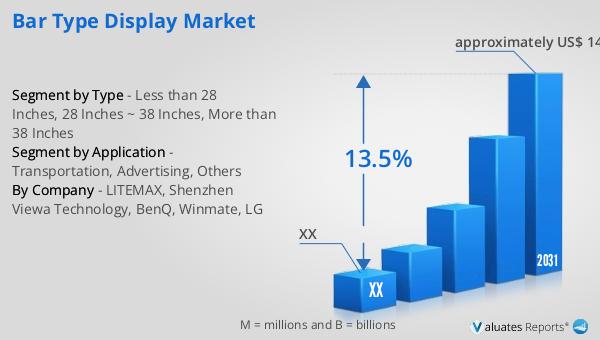

Global Bar Type Display Market Outlook:

In 2024, the global market size of Bar Type Display was valued at approximately US$ 60.4 million, with projections indicating a growth to around US$ 145 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 13.5% during the forecast period from 2025 to 2031. Taiwan is recognized as the largest producer of Bar Type Displays, holding a market share of about 50%, followed closely by China with a 40% share. The industry is dominated by key manufacturers such as Fin Fun, Mertailor, Sun Tail Mermaid, Dubai Mermaids, and Swimtails, which collectively account for approximately 60% of the market share. These companies are at the forefront of innovation and production, driving the market forward with their advanced technologies and high-quality products. The competitive landscape of the Global Bar Type Display Market is characterized by a focus on technological advancements, product differentiation, and strategic partnerships. As the demand for digital signage solutions continues to grow, manufacturers are investing in research and development to enhance the performance and capabilities of their displays. This includes improvements in resolution, color accuracy, and connectivity options, as well as the integration of advanced features such as touch interactivity and motion sensors. The market is also witnessing an increasing trend towards customization, with businesses seeking tailored solutions that meet their specific needs and requirements. This has led to the development of a wide range of display sizes and configurations, catering to various applications and environments. As the Global Bar Type Display Market continues to evolve, it presents significant opportunities for growth and innovation, driven by the increasing adoption of digital signage solutions across various industries.

| Report Metric | Details |

| Report Name | Bar Type Display Market |

| Forecasted market size in 2031 | approximately US$ 145 million |

| CAGR | 13.5% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | LITEMAX, Shenzhen Viewa Technology, BenQ, Winmate, LG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |