What is Global Overall Turbochargers Market?

The Global Overall Turbochargers Market is a dynamic and rapidly evolving sector that plays a crucial role in enhancing the efficiency and performance of internal combustion engines. Turbochargers are devices that increase an engine's power output by forcing extra compressed air into the combustion chamber, allowing more fuel to be burned. This results in improved engine efficiency and reduced emissions, making turbochargers a vital component in modern automotive and industrial applications. The market for turbochargers is driven by the increasing demand for fuel-efficient vehicles, stringent emission regulations, and the growing adoption of turbocharging technology in various sectors. With advancements in technology, turbochargers have become more compact, efficient, and reliable, further boosting their adoption across different industries. The market is characterized by intense competition among key players, continuous innovation, and a focus on developing eco-friendly and high-performance turbocharging solutions. As the automotive industry shifts towards greener technologies, the turbocharger market is expected to witness significant growth, driven by the need for sustainable and efficient powertrain solutions.

Mono Turbo, Twin Turbo in the Global Overall Turbochargers Market:

Mono Turbo and Twin Turbo are two prominent types of turbocharging systems that have gained significant traction in the Global Overall Turbochargers Market. A Mono Turbo system, as the name suggests, utilizes a single turbocharger to boost the engine's power. This type of turbocharger is typically used in smaller engines or applications where space and cost constraints are a concern. Mono Turbo systems are known for their simplicity, cost-effectiveness, and ease of installation. They provide a noticeable increase in power and efficiency, making them a popular choice for entry-level and mid-range vehicles. However, they may not offer the same level of performance as more complex systems, such as Twin Turbo setups. On the other hand, Twin Turbo systems employ two turbochargers to enhance engine performance. These systems can be configured in various ways, such as sequential, parallel, or staged, depending on the desired performance characteristics. Sequential Twin Turbo systems use one small turbocharger for low engine speeds and a larger one for higher speeds, providing a smooth and responsive power delivery across the entire RPM range. Parallel Twin Turbo systems, meanwhile, use two identical turbochargers to split the engine's exhaust flow, offering improved performance and efficiency. Staged Twin Turbo systems combine the benefits of both sequential and parallel setups, delivering exceptional power and responsiveness. Twin Turbo systems are often found in high-performance vehicles and sports cars, where maximum power and efficiency are paramount. They offer superior performance compared to Mono Turbo systems, but at a higher cost and complexity. The choice between Mono Turbo and Twin Turbo systems depends on various factors, including the vehicle's intended use, performance requirements, and budget constraints. As the Global Overall Turbochargers Market continues to evolve, manufacturers are focusing on developing innovative turbocharging solutions that cater to the diverse needs of consumers. This includes the integration of advanced materials, improved aerodynamics, and electronic controls to enhance the performance and efficiency of both Mono and Twin Turbo systems. Additionally, the growing trend towards downsizing engines while maintaining or improving performance is driving the demand for more efficient and compact turbocharging solutions. As a result, both Mono Turbo and Twin Turbo systems are expected to play a crucial role in the future of the turbocharger market, offering a range of options for consumers seeking enhanced performance and efficiency.

Automotive, Engineering Machinery, Others in the Global Overall Turbochargers Market:

The Global Overall Turbochargers Market finds extensive applications across various sectors, including automotive, engineering machinery, and others. In the automotive industry, turbochargers are widely used to improve the performance and efficiency of internal combustion engines. They enable smaller engines to produce the same power as larger ones, contributing to the trend of engine downsizing. This not only enhances fuel efficiency but also reduces emissions, aligning with stringent environmental regulations. Turbochargers are commonly found in passenger cars, commercial vehicles, and high-performance sports cars, where they provide a significant boost in power and torque. In engineering machinery, turbochargers play a vital role in enhancing the performance of heavy-duty equipment such as construction machinery, agricultural vehicles, and industrial engines. These machines require high power output and efficiency to perform demanding tasks, and turbochargers help achieve these requirements by increasing the engine's power density. This results in improved productivity, reduced fuel consumption, and lower emissions, making turbochargers an essential component in modern engineering machinery. Beyond automotive and engineering machinery, turbochargers are also used in other sectors such as marine, aerospace, and power generation. In marine applications, turbochargers are employed in ship engines to enhance performance and fuel efficiency, contributing to lower operational costs and reduced environmental impact. In the aerospace industry, turbochargers are used in aircraft engines to improve performance at high altitudes, where air density is lower. This ensures optimal engine performance and efficiency, enhancing the overall safety and reliability of aircraft operations. In power generation, turbochargers are used in gas turbines and other power generation equipment to increase efficiency and output, supporting the growing demand for energy worldwide. The versatility and efficiency of turbochargers make them a valuable asset across various industries, driving their adoption and growth in the Global Overall Turbochargers Market.

Global Overall Turbochargers Market Outlook:

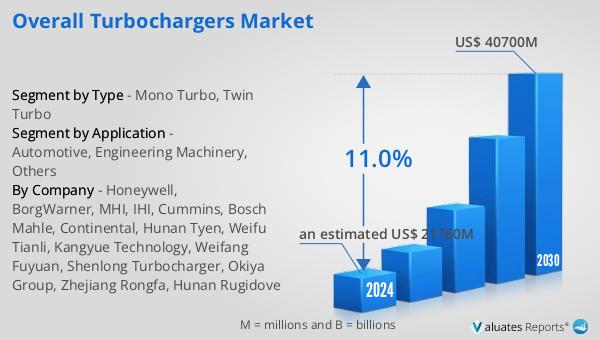

In 2024, the global market size for Overall Turbochargers was valued at approximately US$ 23,910 million, with projections indicating it could reach around US$ 49,160 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 11.0% during the forecast period from 2025 to 2031. The Asia-Pacific region holds the largest share of the Overall Turbochargers market, accounting for about 45% of the total market. Europe follows closely with a 40% market share. The industry is dominated by key manufacturers such as Honeywell, BorgWarner, MHI, IHI, and Cummins, who collectively hold approximately 75% of the market share. These companies are at the forefront of innovation and development in the turbocharger industry, driving advancements in technology and efficiency. The competitive landscape is characterized by continuous research and development efforts, strategic partnerships, and a focus on meeting the evolving demands of consumers and regulatory bodies. As the market continues to expand, these leading manufacturers are expected to play a pivotal role in shaping the future of the Global Overall Turbochargers Market, contributing to its growth and development.

| Report Metric | Details |

| Report Name | Overall Turbochargers Market |

| Forecasted market size in 2031 | approximately US$ 49160 million |

| CAGR | 11.0% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Honeywell, BorgWarner, MHI, IHI, Cummins, Bosch Mahle, Continental, Hunan Tyen, Weifu Tianli, Kangyue Technology, Weifang Fuyuan, Shenlong Turbocharger, Okiya Group, Zhejiang Rongfa, Hunan Rugidove |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |