What is Global Vinylphosphonic Acid Market?

The Global Vinylphosphonic Acid Market is a niche segment within the broader chemical industry, focusing on the production and application of vinylphosphonic acid (VPA). This compound is a specialized monomer used in various industrial applications due to its unique chemical properties, such as its ability to form polymers with high thermal stability and flame retardancy. VPA is primarily utilized in the production of coatings, adhesives, and flame retardants, making it a valuable component in industries that require materials with enhanced durability and safety features. The market for vinylphosphonic acid is driven by the growing demand for high-performance materials in sectors such as construction, automotive, and electronics. Additionally, the increasing focus on sustainable and environmentally friendly products has led to the development of bio-based VPA, further expanding its market potential. Despite its specialized nature, the Global Vinylphosphonic Acid Market is expected to grow steadily, supported by technological advancements and the continuous exploration of new applications. The market's growth is also influenced by regional factors, with Europe being the largest consumer due to its well-established industrial base and stringent regulatory standards. Overall, the Global Vinylphosphonic Acid Market represents a dynamic and evolving segment with significant opportunities for innovation and expansion.

VPA 80%, VPA 90%, Others in the Global Vinylphosphonic Acid Market:

Vinylphosphonic Acid (VPA) is available in various grades, primarily distinguished by their purity levels, such as VPA 80% and VPA 90%, among others. These grades are crucial in determining the suitability of VPA for different applications. VPA 80% refers to a grade where the acid is present at 80% purity, with the remaining 20% typically consisting of water and other minor impurities. This grade is often used in applications where ultra-high purity is not critical but where the unique properties of VPA, such as its ability to enhance adhesion and improve flame retardancy, are still required. For instance, VPA 80% is commonly used in the formulation of adhesives and sealants, where it helps improve the bonding strength and durability of the final product. On the other hand, VPA 90% is a higher purity grade, containing 90% vinylphosphonic acid. This grade is preferred in applications that demand higher performance and where the presence of impurities could negatively impact the product's effectiveness. Industries such as electronics and advanced coatings often require VPA 90% due to its superior properties, including enhanced thermal stability and resistance to harsh environmental conditions. The higher purity level ensures that the final products meet stringent quality standards, making VPA 90% a preferred choice for high-end applications. Beyond these standard grades, there are other specialized forms of VPA that cater to specific industrial needs. These may include customized formulations or blends that incorporate additional functional groups to enhance certain properties. For example, in the field of polymer chemistry, modified VPA can be used to create copolymers with tailored characteristics, such as improved flexibility or increased resistance to chemical degradation. The versatility of VPA in its various forms makes it a valuable component in the development of innovative materials and solutions across multiple industries. The choice between VPA 80%, VPA 90%, and other specialized forms depends largely on the specific requirements of the application and the desired performance characteristics. Manufacturers and end-users must carefully consider factors such as purity, cost, and compatibility with other materials when selecting the appropriate grade of VPA for their needs. As the demand for high-performance materials continues to grow, the availability of different VPA grades provides the flexibility needed to meet diverse industrial challenges and drive innovation in product development.

Coating, Printing, Water Treatment & Oil Well, Fuel Cells, Medical Care, Others in the Global Vinylphosphonic Acid Market:

Vinylphosphonic Acid (VPA) finds extensive usage across various industries due to its unique chemical properties, which make it an ideal component for enhancing the performance of different products. In the coatings industry, VPA is used to improve the adhesion, durability, and flame retardancy of coatings applied to surfaces such as metals, plastics, and textiles. Its ability to form strong chemical bonds with substrates ensures that coatings remain intact and effective even under harsh environmental conditions. This makes VPA a valuable additive in the production of protective coatings for automotive, aerospace, and construction applications, where long-lasting performance is critical. In the printing industry, VPA is utilized to enhance the quality and durability of printed materials. It is often incorporated into inks and printing formulations to improve adhesion to various substrates, such as paper, plastic, and metal. This results in sharper, more vibrant prints that are resistant to smudging and fading, making VPA an essential component in the production of high-quality printed products. Additionally, VPA's flame-retardant properties make it a valuable additive in the formulation of fire-resistant inks and coatings, further expanding its applications in the printing sector. In the field of water treatment and oil well applications, VPA is used as a scale inhibitor and corrosion inhibitor. Its ability to form stable complexes with metal ions helps prevent the formation of scale deposits in pipelines and equipment, ensuring efficient operation and reducing maintenance costs. In oil well applications, VPA is used to enhance the performance of drilling fluids and improve the stability of wellbore structures. Its corrosion-inhibiting properties also help protect equipment from damage, extending the lifespan of critical infrastructure in the oil and gas industry. VPA is also gaining attention in the field of fuel cells, where it is used as a proton-conducting material in the development of advanced fuel cell membranes. Its high thermal stability and chemical resistance make it an ideal candidate for use in fuel cells that operate at elevated temperatures, improving the efficiency and durability of these energy systems. In the medical care industry, VPA is used in the development of biocompatible materials and drug delivery systems. Its ability to form stable polymers with tailored properties makes it suitable for use in medical devices, implants, and controlled-release formulations. VPA's versatility and unique properties continue to drive its adoption across a wide range of applications, making it a valuable component in the development of innovative solutions for various industrial challenges.

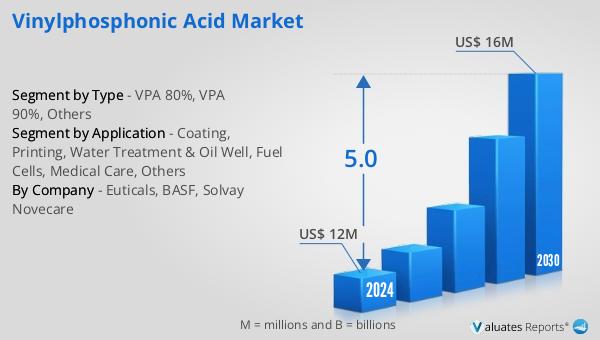

Global Vinylphosphonic Acid Market Outlook:

In 2024, the global market size for Vinylphosphonic Acid was valued at approximately US$ 12.1 million, with projections indicating growth to around US$ 17 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.0% during the forecast period from 2025 to 2031. The market is dominated by key players such as Euticals, BASF, and Solvay Novecare, with the top three manufacturers collectively holding a significant market share of about 99%. Europe emerges as the largest market for Vinylphosphonic Acid, accounting for approximately 92% of the global market share. This dominance is attributed to the region's well-established industrial base, stringent regulatory standards, and a strong focus on innovation and sustainability. The Asia Pacific region follows, with a market share of over 7%, driven by the growing demand for high-performance materials in emerging economies. The market outlook for Vinylphosphonic Acid highlights the importance of technological advancements and the continuous exploration of new applications in driving market growth. As industries increasingly seek materials with enhanced performance characteristics, the demand for Vinylphosphonic Acid is expected to rise, supported by its unique properties and versatility. The market's growth trajectory underscores the potential for innovation and expansion in this niche segment, offering significant opportunities for manufacturers and end-users alike.

| Report Metric | Details |

| Report Name | Vinylphosphonic Acid Market |

| Forecasted market size in 2031 | approximately US$ 17 million |

| CAGR | 5.0% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Euticals, BASF, Solvay Novecare |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |