What is Global Infant Formula Foods Market?

The Global Infant Formula Foods Market is a rapidly growing sector within the broader food and nutrition industry. This market primarily focuses on producing and distributing formula foods designed to meet the nutritional needs of infants who are not breastfed. These products are crucial for ensuring that infants receive the necessary nutrients for healthy growth and development during their early months and years. The market is driven by several factors, including increasing awareness of infant nutrition, rising disposable incomes, and a growing number of working mothers who require convenient feeding solutions. Additionally, advancements in formula composition, which aim to closely mimic the nutritional profile of breast milk, have further fueled market growth. The market is highly competitive, with numerous global and regional players striving to innovate and capture market share. As a result, the Global Infant Formula Foods Market is characterized by a diverse range of products, catering to various dietary needs and preferences, including organic, hypoallergenic, and specialized formulas for infants with specific health conditions. This dynamic market continues to evolve, driven by ongoing research and development efforts and changing consumer preferences.

Infant Formula Powder, Infant Complementary Foods in the Global Infant Formula Foods Market:

Infant Formula Powder and Infant Complementary Foods are two critical segments within the Global Infant Formula Foods Market, each serving distinct purposes in infant nutrition. Infant Formula Powder is a substitute for breast milk, designed to provide essential nutrients to infants who are not breastfed. It is typically made from cow's milk or soy protein, fortified with vitamins, minerals, and other nutrients to support an infant's growth and development. The powder form allows for easy storage and preparation, making it a convenient option for parents. Manufacturers have developed various formulations to cater to different needs, such as lactose-free, hypoallergenic, and organic options, ensuring that infants with specific dietary requirements are adequately nourished. On the other hand, Infant Complementary Foods are introduced to an infant's diet as they transition from exclusive milk feeding to solid foods, usually around six months of age. These foods are designed to complement breast milk or formula, providing additional nutrients that are not sufficiently supplied by milk alone. Complementary foods include pureed fruits and vegetables, cereals, and protein-rich foods, which help infants develop taste preferences and learn to chew and swallow solid foods. The introduction of complementary foods is a critical phase in an infant's development, as it lays the foundation for healthy eating habits and nutritional adequacy. The Global Infant Formula Foods Market has seen significant innovation in both segments, with manufacturers focusing on enhancing the nutritional profile, taste, and convenience of their products. For instance, there is a growing trend towards organic and natural ingredients, reflecting consumer demand for healthier and more sustainable options. Additionally, advancements in packaging technology have improved the shelf life and portability of these products, making them more appealing to busy parents. The market is also witnessing increased investment in research and development, aimed at understanding the complex nutritional needs of infants and developing products that closely mimic the benefits of breast milk. This has led to the introduction of formulas enriched with probiotics, prebiotics, and other bioactive compounds that support gut health and immune function. Furthermore, the rise of e-commerce has transformed the way these products are marketed and distributed, providing consumers with greater access to a wide range of options. Online platforms offer detailed product information, reviews, and recommendations, empowering parents to make informed choices about their infant's nutrition. As the Global Infant Formula Foods Market continues to expand, it is expected to play a crucial role in addressing the nutritional needs of infants worldwide, contributing to their overall health and well-being.

0-6 Months, 6-12 Months, 12-36 Months in the Global Infant Formula Foods Market:

The usage of Global Infant Formula Foods Market products varies significantly across different age groups, specifically 0-6 months, 6-12 months, and 12-36 months, each with unique nutritional requirements. For infants aged 0-6 months, formula milk serves as the primary source of nutrition, especially for those who are not breastfed. During this critical period, infants require a balanced intake of proteins, fats, carbohydrates, vitamins, and minerals to support rapid growth and development. Infant formula is carefully formulated to mimic the nutritional composition of breast milk, providing essential nutrients such as DHA, ARA, and iron, which are crucial for brain development and overall health. As infants transition to the 6-12 months age group, their nutritional needs evolve, and complementary foods are introduced alongside formula or breast milk. This stage marks the beginning of solid food consumption, where infants start exploring different tastes and textures. Complementary foods, such as pureed fruits, vegetables, and cereals, are introduced to provide additional nutrients like fiber, vitamins, and minerals that are not adequately supplied by milk alone. The introduction of complementary foods is essential for meeting the increased energy and nutrient demands of growing infants. For toddlers aged 12-36 months, the focus shifts towards a more varied diet that includes a wider range of solid foods. During this stage, formula milk may still be used as a supplementary source of nutrition, particularly for picky eaters or those with specific dietary needs. However, the emphasis is on encouraging a balanced diet that includes fruits, vegetables, grains, proteins, and dairy products to ensure adequate nutrient intake. The Global Infant Formula Foods Market plays a vital role in supporting the nutritional needs of infants and toddlers across these age groups, offering a diverse range of products that cater to different dietary preferences and requirements. As parents become more aware of the importance of early nutrition, the demand for high-quality, nutritionally balanced formula and complementary foods continues to grow, driving innovation and growth in the market.

Global Infant Formula Foods Market Outlook:

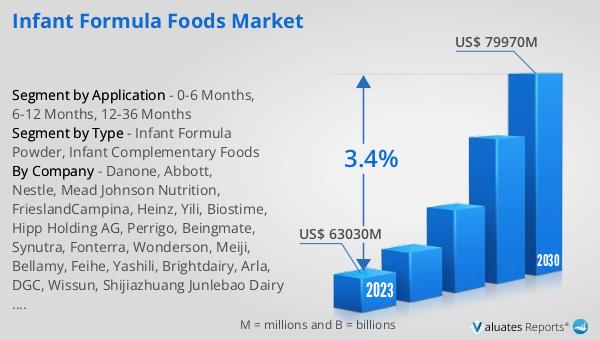

In 2024, the global market for Infant Formula Foods was valued at approximately $67.43 billion, with projections indicating it could reach around $84.93 billion by 2031, growing at a compound annual growth rate (CAGR) of 3.4% from 2025 to 2031. China stands out as the largest market for Infant Formula Foods, holding a significant 30% share of the global market. Following China, Europe accounts for about 20% of the market share. The industry is dominated by major players such as Danone, Abbott, Nestle, Mead Johnson Nutrition, and FrieslandCampina, which collectively control approximately 55% of the market. These companies are at the forefront of innovation and product development, striving to meet the diverse needs of consumers worldwide. The market's growth is driven by factors such as increasing awareness of infant nutrition, rising disposable incomes, and a growing number of working mothers seeking convenient feeding solutions. As the market continues to evolve, it is expected to play a crucial role in addressing the nutritional needs of infants globally, contributing to their overall health and well-being.

| Report Metric | Details |

| Report Name | Infant Formula Foods Market |

| CAGR | 3.4% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Danone, Abbott, Nestle, Mead Johnson Nutrition, FrieslandCampina, Heinz, Yili, Biostime, Hipp Holding AG, Perrigo, Beingmate, Synutra, Fonterra, Wonderson, Meiji, Bellamy, Feihe, Yashili, Brightdairy, Arla, DGC, Wissun, Shijiazhuang Junlebao Dairy Co., Ltd., Westland Milk Products, Pinnacle, Holle baby food GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |