What is Global Mica Tape for Insulation Market?

The Global Mica Tape for Insulation Market is a specialized segment within the broader insulation materials industry, focusing on the use of mica tape as a key component for electrical insulation. Mica, a naturally occurring mineral known for its excellent thermal and electrical insulating properties, is used in the production of mica tape. This tape is primarily utilized in electrical and thermal insulation applications, particularly in industries where high-temperature resistance and electrical insulation are critical. The market for mica tape is driven by its application in various sectors, including electronics, automotive, and energy, where it is used to insulate wires, cables, and other components. The demand for mica tape is influenced by the growth of these industries, technological advancements, and the increasing need for reliable and efficient insulation materials. As industries continue to evolve and expand, the Global Mica Tape for Insulation Market is expected to grow, driven by the need for high-performance insulation solutions that can withstand extreme conditions and ensure the safety and efficiency of electrical systems.

Mica Glass Tape, Mica Polyester Tape in the Global Mica Tape for Insulation Market:

Mica Glass Tape and Mica Polyester Tape are two prominent types of mica tape used in the Global Mica Tape for Insulation Market, each offering unique properties and applications. Mica Glass Tape is composed of mica paper bonded to a glass cloth, providing excellent thermal and electrical insulation. This type of tape is highly resistant to high temperatures and is commonly used in applications where thermal stability is crucial, such as in the insulation of high-voltage cables and electrical equipment. The glass cloth reinforcement enhances the mechanical strength of the tape, making it suitable for use in demanding environments where durability is essential. Mica Glass Tape is often preferred in industries like power generation, aerospace, and automotive, where reliable insulation is critical to ensure the safety and efficiency of electrical systems. On the other hand, Mica Polyester Tape combines mica paper with a polyester film, offering a different set of advantages. The polyester film provides flexibility and ease of handling, making Mica Polyester Tape ideal for applications where conformability and ease of installation are important. This type of tape is often used in the insulation of low to medium voltage cables and electrical components, where its flexibility allows for easy wrapping and installation. Mica Polyester Tape is also valued for its excellent dielectric properties, which make it suitable for use in a wide range of electrical insulation applications. The combination of mica and polyester ensures that the tape can withstand high temperatures while maintaining its insulating properties, making it a versatile choice for various industries. Both Mica Glass Tape and Mica Polyester Tape play crucial roles in the Global Mica Tape for Insulation Market, catering to different needs and applications. The choice between the two depends on the specific requirements of the application, such as the operating temperature, mechanical strength, and flexibility needed. As industries continue to demand more efficient and reliable insulation solutions, the development and innovation of mica tape products are expected to advance, offering enhanced performance and new applications. The versatility and effectiveness of mica tape make it an indispensable component in the insulation of electrical systems, contributing to the safety, efficiency, and longevity of these systems across various industries.

3.3 kV to 6 kV, 6 kV to 10 kV, Above 10 kV in the Global Mica Tape for Insulation Market:

The Global Mica Tape for Insulation Market finds extensive usage across different voltage levels, including 3.3 kV to 6 kV, 6 kV to 10 kV, and above 10 kV, each presenting unique requirements and challenges. In the 3.3 kV to 6 kV range, mica tape is primarily used for insulating medium voltage cables and electrical components. This voltage range is common in industrial and commercial applications, where reliable insulation is crucial to prevent electrical failures and ensure the safe operation of equipment. Mica tape provides excellent thermal and electrical insulation, making it an ideal choice for these applications. Its ability to withstand high temperatures and resist electrical breakdown ensures the longevity and reliability of the insulated components, reducing the risk of downtime and maintenance costs. For the 6 kV to 10 kV range, mica tape is used in more demanding applications, where higher voltage levels require enhanced insulation properties. This range is often found in power distribution systems and industrial machinery, where the risk of electrical failure can have significant consequences. Mica tape's superior insulating properties, combined with its mechanical strength and thermal stability, make it an essential component in these applications. It helps to prevent electrical arcing and short circuits, ensuring the safe and efficient operation of electrical systems. The use of mica tape in this voltage range is critical to maintaining the integrity of power distribution networks and industrial processes, where reliability and safety are paramount. In applications above 10 kV, mica tape is used in high-voltage cables and equipment, where the demands on insulation materials are even greater. This voltage range is typically found in power transmission systems and high-voltage equipment used in industries such as power generation and heavy manufacturing. Mica tape's ability to withstand extreme temperatures and provide excellent electrical insulation is crucial in these applications, where the risk of electrical failure can have severe consequences. The tape's mechanical strength and durability ensure that it can withstand the harsh conditions often encountered in high-voltage environments, providing reliable insulation and protection for critical electrical components. The use of mica tape in this voltage range is essential to ensuring the safety and efficiency of power transmission systems and high-voltage equipment, where the demands on insulation materials are at their highest.

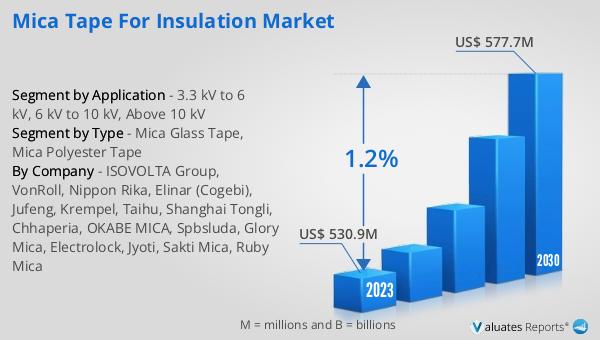

Global Mica Tape for Insulation Market Outlook:

In 2024, the global market size for Mica Tape for Insulation was valued at approximately US$ 544 million, with projections indicating it could reach around US$ 590 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 1.2% during the forecast period from 2025 to 2031. Europe stands out as the leading producer of mica tape for insulation, commanding nearly 45% of the market share. Following Europe, China holds a significant portion of the market with a 25% share. The industry is dominated by a few key players, with the top five manufacturers—ISOVOLTA Group, VonRoll, Elinar, Cogebi, Jufeng, and Krempel—collectively accounting for about 55% of the market share. These companies play a crucial role in shaping the market dynamics, driving innovation, and meeting the growing demand for high-performance insulation materials. The market's steady growth reflects the increasing need for reliable and efficient insulation solutions across various industries, driven by technological advancements and the expansion of sectors such as electronics, automotive, and energy. As the demand for mica tape continues to rise, the market is expected to evolve, offering new opportunities and challenges for manufacturers and stakeholders.

| Report Metric | Details |

| Report Name | Mica Tape for Insulation Market |

| CAGR | 1.2% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | ISOVOLTA Group, VonRoll, Nippon Rika, Elinar (Cogebi), Jufeng, Krempel, Taihu, Shanghai Tongli, Chhaperia, OKABE MICA, Spbsluda, Glory Mica, Electrolock, Jyoti, Sakti Mica, Ruby Mica |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |