What is Global Extraction Condensing Steam Turbines Market?

The Global Extraction Condensing Steam Turbines Market is a specialized segment within the broader steam turbine industry, focusing on turbines that are designed to efficiently convert steam into mechanical energy. These turbines are particularly notable for their ability to extract steam at various stages of the process, which can then be used for heating or other industrial purposes before the remaining steam is condensed and returned to the boiler. This dual functionality makes them highly versatile and efficient, especially in industries where both electricity generation and process steam are required. The market for these turbines is driven by the increasing demand for energy efficiency and the need for sustainable power generation solutions. As industries worldwide strive to reduce their carbon footprint and optimize energy use, extraction condensing steam turbines offer a viable solution. They are widely used in power plants, refineries, and various manufacturing sectors, where they contribute to both energy production and process optimization. The market is characterized by technological advancements, with manufacturers focusing on improving turbine efficiency, reducing emissions, and enhancing operational flexibility. As a result, the Global Extraction Condensing Steam Turbines Market is poised for growth, driven by the ongoing transition towards cleaner and more efficient energy systems.

Single Extraction Condensing Steam Turbine, Multi-Extraction Condensing Steam Turbine in the Global Extraction Condensing Steam Turbines Market:

Single Extraction Condensing Steam Turbines and Multi-Extraction Condensing Steam Turbines are two key types within the Global Extraction Condensing Steam Turbines Market, each serving distinct industrial needs. Single Extraction Condensing Steam Turbines are designed to extract steam at one specific point in the turbine's operation. This extracted steam is typically used for industrial processes or heating applications, while the remaining steam continues through the turbine to generate electricity before being condensed. These turbines are particularly useful in industries where a moderate amount of process steam is required alongside electricity generation. They offer a balance between efficiency and simplicity, making them a popular choice for smaller industrial applications or facilities with less complex steam requirements. On the other hand, Multi-Extraction Condensing Steam Turbines are engineered to extract steam at multiple stages of the turbine's operation. This capability allows for greater flexibility and efficiency, as steam can be extracted at different pressures and temperatures to meet varying industrial needs. These turbines are ideal for large-scale industrial operations or power plants where there is a high demand for process steam at different stages of production. The ability to extract steam at multiple points allows for more precise control over the steam supply, optimizing both energy production and industrial processes. Multi-extraction turbines are often used in complex industrial settings such as chemical plants, refineries, and large manufacturing facilities, where the demand for steam varies significantly throughout the production process. Both types of turbines play a crucial role in enhancing energy efficiency and reducing operational costs. By utilizing the extracted steam for industrial processes, these turbines help industries reduce their reliance on separate boilers or heating systems, leading to significant energy savings. Additionally, the condensing process in these turbines ensures that the maximum amount of energy is extracted from the steam, further enhancing overall efficiency. The choice between single and multi-extraction turbines depends largely on the specific needs of the industry and the complexity of the steam requirements. As industries continue to seek ways to optimize energy use and reduce emissions, the demand for both single and multi-extraction condensing steam turbines is expected to grow. Manufacturers are continually innovating to improve the performance and efficiency of these turbines, incorporating advanced materials, design improvements, and digital technologies to enhance their capabilities. This ongoing innovation is crucial in meeting the evolving needs of industries and supporting the transition towards more sustainable and efficient energy systems.

Chemical and Petrochemical, General Industrial, Others in the Global Extraction Condensing Steam Turbines Market:

The Global Extraction Condensing Steam Turbines Market finds extensive applications across various sectors, including Chemical and Petrochemical, General Industrial, and others, each benefiting from the unique capabilities of these turbines. In the Chemical and Petrochemical sector, extraction condensing steam turbines are integral to operations due to their ability to provide both electricity and process steam. These industries often require large amounts of steam for chemical reactions, distillation, and other processes. The flexibility of extraction condensing turbines allows them to meet these demands efficiently, providing steam at the necessary pressure and temperature while also generating electricity. This dual functionality is particularly valuable in chemical plants, where energy efficiency and process optimization are critical for maintaining competitiveness and reducing environmental impact. In the General Industrial sector, extraction condensing steam turbines are used in a wide range of applications, from manufacturing to food processing. Industries in this category often require steam for heating, drying, or other processes, alongside electricity generation. The ability to extract steam at various stages of the turbine's operation allows these industries to optimize their energy use, reducing reliance on separate boilers or heating systems. This not only leads to cost savings but also enhances operational efficiency and sustainability. The versatility of these turbines makes them suitable for a broad spectrum of industrial applications, supporting the diverse energy needs of the sector. Beyond these specific sectors, extraction condensing steam turbines are also used in other areas such as district heating, pulp and paper production, and waste-to-energy plants. In district heating systems, these turbines provide a reliable source of steam for heating residential and commercial buildings, contributing to energy efficiency and sustainability. In the pulp and paper industry, they are used to generate the steam required for various production processes, while also producing electricity to power the facility. Waste-to-energy plants utilize extraction condensing steam turbines to convert waste into energy, providing a sustainable solution for waste management and energy production. The ability to efficiently convert steam into mechanical energy, while also providing process steam, makes these turbines a valuable asset in these diverse applications. As industries continue to prioritize energy efficiency and sustainability, the demand for extraction condensing steam turbines is expected to grow across these sectors. Manufacturers are responding to this demand by developing advanced turbine technologies that offer improved efficiency, reduced emissions, and greater operational flexibility. This ongoing innovation is essential in meeting the evolving needs of industries and supporting the transition towards more sustainable and efficient energy systems.

Global Extraction Condensing Steam Turbines Market Outlook:

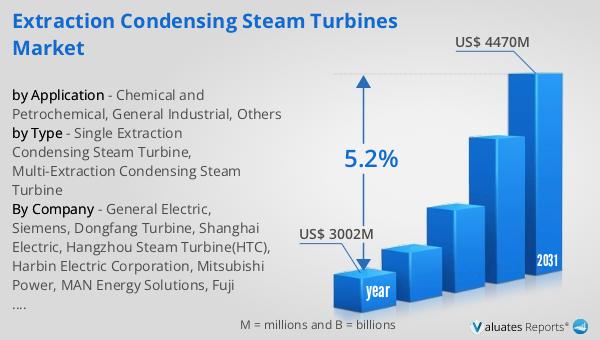

The global market for Extraction Condensing Steam Turbines was valued at $3,002 million in 2024, with projections indicating a growth to $4,470 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.2% over the forecast period. This upward trend reflects the increasing demand for energy-efficient solutions and the growing emphasis on sustainable power generation across various industries. As industries worldwide strive to optimize energy use and reduce their carbon footprint, extraction condensing steam turbines offer a viable solution. These turbines are particularly valued for their ability to provide both electricity and process steam, making them an ideal choice for industries with complex energy needs. The market's growth is also driven by technological advancements, with manufacturers focusing on improving turbine efficiency, reducing emissions, and enhancing operational flexibility. As a result, the Global Extraction Condensing Steam Turbines Market is poised for significant growth, driven by the ongoing transition towards cleaner and more efficient energy systems. This growth is expected to continue as industries increasingly prioritize energy efficiency and sustainability, creating new opportunities for manufacturers and stakeholders in the market.

| Report Metric | Details |

| Report Name | Extraction Condensing Steam Turbines Market |

| Accounted market size in year | US$ 3002 million |

| Forecasted market size in 2031 | US$ 4470 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | General Electric, Siemens, Dongfang Turbine, Shanghai Electric, Hangzhou Steam Turbine(HTC), Harbin Electric Corporation, Mitsubishi Power, MAN Energy Solutions, Fuji Electric, Ebara Elliott, Doosan, Ansaldo, Kawasaki Heavy Industries, Power Machines |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |