What is Global Direct Drive (Gearless) Wind Turbine Sales Market?

The Global Direct Drive (Gearless) Wind Turbine Sales Market represents a significant segment within the renewable energy industry, focusing on the production and sale of wind turbines that operate without a gearbox. These turbines are designed to convert wind energy into electricity more efficiently by eliminating the mechanical complexity and maintenance issues associated with traditional gear-driven turbines. The absence of a gearbox reduces the number of moving parts, leading to lower maintenance costs and increased reliability. This market is driven by the growing demand for sustainable energy solutions and the need to reduce carbon emissions globally. As countries strive to meet their renewable energy targets, the adoption of direct drive wind turbines is expected to rise. These turbines are particularly advantageous in offshore wind farms where maintenance can be challenging and costly. The market is characterized by technological advancements, with manufacturers focusing on improving turbine efficiency and durability. The global push towards clean energy, coupled with government incentives and policies supporting renewable energy projects, is expected to fuel the growth of the direct drive wind turbine market in the coming years.

in the Global Direct Drive (Gearless) Wind Turbine Sales Market:

The Global Direct Drive (Gearless) Wind Turbine Sales Market caters to a diverse range of customers, each with specific needs and preferences. One of the primary types of direct drive wind turbines is the permanent magnet synchronous generator (PMSG) turbine. These turbines are favored for their high efficiency and reliability, making them suitable for both onshore and offshore applications. PMSG turbines are particularly popular among utility companies and large-scale energy producers who require robust and efficient solutions to meet their energy demands. Another type is the electrically excited synchronous generator (EESG) turbine, which offers the advantage of variable speed operation and improved grid compatibility. EESG turbines are often chosen by customers who prioritize flexibility and adaptability in their energy systems. Additionally, there are hybrid direct drive turbines that combine the benefits of both PMSG and EESG technologies. These turbines are designed to optimize performance and efficiency, making them an attractive option for customers looking to maximize their return on investment. The choice of turbine type often depends on factors such as location, wind conditions, and specific energy requirements. For instance, offshore wind farms may prefer PMSG turbines due to their durability and low maintenance needs, while onshore projects might opt for EESG turbines for their adaptability to varying wind speeds. Furthermore, the market also includes small-scale direct drive turbines designed for residential or community use. These turbines are typically used by individual homeowners or small businesses looking to generate their own renewable energy. They are compact, easy to install, and require minimal maintenance, making them an ideal choice for those seeking a sustainable energy solution without the need for large-scale infrastructure. The growing awareness of environmental issues and the increasing demand for clean energy have led to a rise in the adoption of direct drive wind turbines across various sectors. As technology continues to advance, the market is expected to see the development of more efficient and cost-effective turbine solutions, catering to a wider range of customers and applications.

in the Global Direct Drive (Gearless) Wind Turbine Sales Market:

The applications of the Global Direct Drive (Gearless) Wind Turbine Sales Market are vast and varied, reflecting the diverse needs of different sectors seeking sustainable energy solutions. One of the primary applications is in large-scale wind farms, both onshore and offshore. These wind farms are typically operated by utility companies and large energy producers who require reliable and efficient energy generation to meet the demands of their customers. Direct drive wind turbines are particularly well-suited for these applications due to their high efficiency, low maintenance requirements, and ability to operate in challenging environments. Offshore wind farms, in particular, benefit from the use of direct drive turbines, as they are less susceptible to the harsh conditions and maintenance challenges associated with offshore installations. Another significant application of direct drive wind turbines is in community and residential energy projects. These smaller-scale installations are designed to provide renewable energy to local communities or individual households, reducing their reliance on traditional energy sources and lowering their carbon footprint. Direct drive turbines are ideal for these applications due to their compact size, ease of installation, and minimal maintenance needs. They offer a practical and cost-effective solution for those looking to generate their own clean energy and contribute to a more sustainable future. In addition to these applications, direct drive wind turbines are also used in industrial and commercial settings. Businesses and industries with high energy demands can benefit from the efficiency and reliability of direct drive turbines, reducing their energy costs and environmental impact. These turbines can be integrated into existing energy systems, providing a stable and consistent source of renewable energy. As more companies prioritize sustainability and seek to reduce their carbon emissions, the adoption of direct drive wind turbines in industrial and commercial applications is expected to increase. Furthermore, direct drive wind turbines are increasingly being used in hybrid energy systems, where they are combined with other renewable energy sources such as solar power. These systems offer a more balanced and reliable energy supply, taking advantage of the complementary nature of wind and solar energy. By integrating direct drive turbines into hybrid systems, energy producers can optimize their energy generation and reduce their reliance on fossil fuels. Overall, the applications of direct drive wind turbines are diverse and continue to expand as technology advances and the demand for clean energy grows.

Global Direct Drive (Gearless) Wind Turbine Sales Market Outlook:

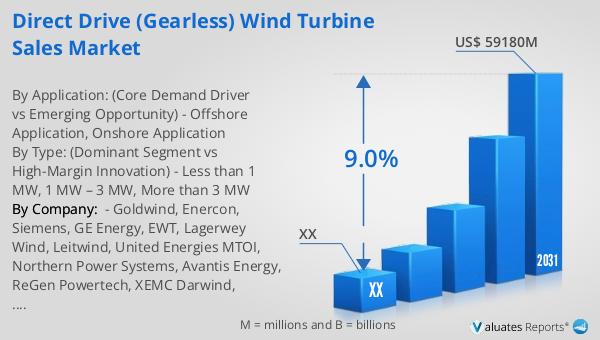

The wind turbine market, valued at approximately $32.64 billion in 2024, is projected to grow significantly, reaching an estimated $59.18 billion by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 9.0% from 2025 to 2031. A notable aspect of this market is the dominance of the top five global players, who collectively hold around 65% of the market share. This concentration indicates a competitive landscape where a few key players drive innovation and market trends. Within the product segments, turbines with a capacity of 1 MW to 3 MW represent the largest share, accounting for approximately 85% of the market. This segment's prominence suggests a strong demand for medium-capacity turbines, which are likely favored for their balance of efficiency and cost-effectiveness. The market's growth is driven by increasing investments in renewable energy and the global push towards sustainable energy solutions. As countries strive to meet their renewable energy targets and reduce carbon emissions, the demand for wind turbines, particularly those in the 1 MW to 3 MW range, is expected to rise. This market outlook highlights the potential for continued growth and innovation in the wind turbine industry, as manufacturers and energy producers work to meet the evolving needs of the global energy market.

| Report Metric | Details |

| Report Name | Direct Drive (Gearless) Wind Turbine Sales Market |

| Forecasted market size in 2031 | US$ 59180 million |

| CAGR | 9.0% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Goldwind, Enercon, Siemens, GE Energy, EWT, Lagerwey Wind, Leitwind, United Energies MTOI, Northern Power Systems, Avantis Energy, ReGen Powertech, XEMC Darwind, American Superconductor Corp., VENSYS Energy, Ghrepower Green Energy |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |