What is Global Chlorinated Polyvinylchloride (CPVC) Sales Market?

The Global Chlorinated Polyvinylchloride (CPVC) Sales Market is a significant segment within the broader plastics industry, focusing on the production and distribution of CPVC materials. CPVC is a thermoplastic produced by chlorinating polyvinyl chloride (PVC) resin, which enhances its temperature and chemical resistance. This makes CPVC an ideal choice for applications requiring durability and reliability under harsh conditions. The market for CPVC is driven by its extensive use in various industries, including construction, chemical processing, and water treatment. As urbanization and industrialization continue to rise globally, the demand for CPVC products is expected to grow. The market is characterized by a diverse range of products, catering to different industrial needs, and is supported by advancements in manufacturing technologies that improve the quality and performance of CPVC materials. The global CPVC market is competitive, with numerous players striving to innovate and expand their product offerings to capture a larger market share.

in the Global Chlorinated Polyvinylchloride (CPVC) Sales Market:

The Global Chlorinated Polyvinylchloride (CPVC) Sales Market offers a variety of types tailored to meet the diverse needs of its customers. One of the primary types is the Injection Grade CPVC, which is predominantly used in the manufacturing of fittings and valves. This type is favored for its excellent flow characteristics and ease of processing, making it suitable for complex shapes and designs. Injection Grade CPVC is particularly popular in the plumbing industry, where precision and reliability are crucial. Another significant type is the Extrusion Grade CPVC, which is used in the production of pipes and sheets. This type is valued for its ability to withstand high temperatures and pressures, making it ideal for hot and cold water distribution systems. Extrusion Grade CPVC is also used in industrial applications where chemical resistance is essential. Additionally, there is the CPVC Compound, which is a blend of CPVC resin with various additives to enhance its properties. This type is used in specialized applications where specific performance characteristics are required, such as in fire sprinkler systems and chemical processing equipment. The versatility of CPVC types allows manufacturers to cater to a wide range of industries, each with its unique requirements. For instance, in the construction industry, CPVC is used for its durability and resistance to corrosion, while in the chemical industry, it is chosen for its ability to handle aggressive chemicals. The automotive industry also utilizes CPVC for its lightweight and heat-resistant properties, which contribute to fuel efficiency and safety. Furthermore, the electrical industry benefits from CPVC's insulating properties, using it in cable insulation and conduit systems. The diversity of CPVC types ensures that there is a suitable solution for almost every application, making it a vital material in modern industrial and commercial sectors. As the demand for sustainable and efficient materials continues to grow, the CPVC market is poised to expand, driven by innovation and the development of new applications. Manufacturers are continually exploring new formulations and processing techniques to enhance the performance and sustainability of CPVC products, ensuring that they meet the evolving needs of their customers. The Global Chlorinated Polyvinylchloride (CPVC) Sales Market is a dynamic and evolving sector, characterized by its ability to adapt to changing market demands and technological advancements.

in the Global Chlorinated Polyvinylchloride (CPVC) Sales Market:

The Global Chlorinated Polyvinylchloride (CPVC) Sales Market finds applications across a wide range of industries, each leveraging the unique properties of CPVC to enhance their operations. In the construction industry, CPVC is extensively used for plumbing systems due to its resistance to corrosion and ability to withstand high temperatures. This makes it an ideal choice for both residential and commercial buildings, where reliable and long-lasting piping systems are essential. CPVC pipes are also used in fire sprinkler systems, where their ability to handle high-pressure water flow is crucial for effective fire suppression. In the chemical processing industry, CPVC is valued for its chemical resistance, making it suitable for transporting aggressive chemicals and corrosive substances. This application is critical in ensuring the safe and efficient operation of chemical plants, where material integrity is paramount. The water treatment industry also benefits from CPVC's durability and resistance to chemical degradation, using it in various components such as tanks, valves, and piping systems. In the automotive industry, CPVC is used for its lightweight and heat-resistant properties, contributing to improved fuel efficiency and safety. It is used in various components, including fuel lines and under-the-hood applications, where high temperatures are common. The electrical industry utilizes CPVC for its excellent insulating properties, using it in cable insulation and conduit systems to ensure safety and reliability in electrical installations. Additionally, CPVC is used in the manufacturing of industrial equipment, where its strength and resistance to wear and tear are essential for maintaining operational efficiency. The versatility of CPVC allows it to be used in a wide range of applications, each benefiting from its unique properties. As industries continue to seek materials that offer a balance of performance, durability, and cost-effectiveness, CPVC remains a popular choice. The ongoing development of new applications and the continuous improvement of CPVC formulations ensure that it remains a relevant and valuable material in various sectors. The Global Chlorinated Polyvinylchloride (CPVC) Sales Market is characterized by its adaptability and ability to meet the diverse needs of its customers, making it a key player in the global materials market.

Global Chlorinated Polyvinylchloride (CPVC) Sales Market Outlook:

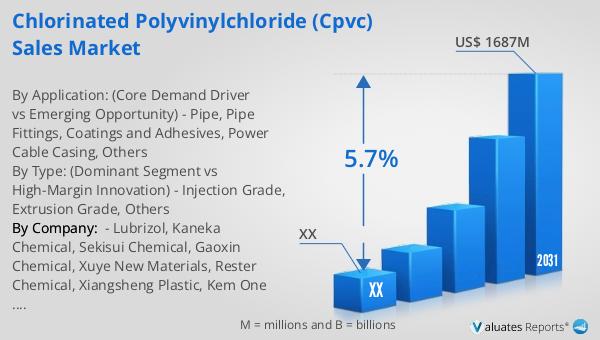

The global market for Chlorinated Polyvinylchloride (CPVC) is projected to grow significantly, with its size estimated at $1,152 million in 2024 and expected to reach an adjusted size of $1,687 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2025 to 2031. The market is dominated by the top three manufacturers, who collectively hold a market share exceeding 60%. North America emerges as the largest regional market, accounting for approximately 38% of the global share. Among the various product types, Injection Grade CPVC stands out as the largest segment, commanding a share of over 79%. This dominance is attributed to its widespread use in the manufacturing of fittings and valves, particularly in the plumbing industry. The market's growth is driven by the increasing demand for durable and reliable materials across various industries, coupled with advancements in manufacturing technologies that enhance the performance and quality of CPVC products. As the market continues to evolve, manufacturers are focusing on innovation and expanding their product offerings to capture a larger share of the growing demand for CPVC materials.

| Report Metric | Details |

| Report Name | Chlorinated Polyvinylchloride (CPVC) Sales Market |

| Forecasted market size in 2031 | US$ 1687 million |

| CAGR | 5.7% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Lubrizol, Kaneka Chemical, Sekisui Chemical, Gaoxin Chemical, Xuye New Materials, Rester Chemical, Xiangsheng Plastic, Kem One (Klesch Group), Shanghai Chlor-Alkali Chemical, Avient, Sundow Polymers, Novista, Jiangsu Tianteng Chemical, Tianchen Chemical, Hanwha Chemical, Shandong Pujie |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |