What is Global Medical 3D Bioprinting Market?

The Global Medical 3D Bioprinting Market is a rapidly evolving sector that combines the innovative technology of 3D printing with the intricate field of biomedicine. This market focuses on the development and application of 3D bioprinting techniques to create complex biological structures that mimic natural tissues and organs. The primary goal is to address the growing demand for organ transplants and the need for advanced medical research tools. By using bio-inks made from living cells, 3D bioprinting can produce tissue-like structures that are used for medical research, drug testing, and potentially, organ transplantation. This technology holds the promise of revolutionizing the healthcare industry by providing more personalized and effective treatment options. It also offers the potential to significantly reduce the time and cost associated with traditional methods of tissue engineering and organ transplantation. As the technology continues to advance, the Global Medical 3D Bioprinting Market is expected to play a crucial role in the future of medicine, offering new solutions to some of the most challenging medical problems.

SLA, FDM, LOM, Others in the Global Medical 3D Bioprinting Market:

In the Global Medical 3D Bioprinting Market, several key technologies are utilized, each with its unique advantages and applications. Stereolithography (SLA) is one of the most widely used 3D printing technologies in the medical field. It works by using a laser to cure liquid resin into solid layers, creating highly detailed and accurate models. SLA is particularly useful for creating intricate structures and is often used in the production of dental models, surgical guides, and hearing aids. Its precision and ability to produce smooth surfaces make it ideal for applications where detail is critical. Fused Deposition Modeling (FDM) is another popular technology in the medical 3D bioprinting market. FDM works by extruding thermoplastic filaments through a heated nozzle, layer by layer, to create a 3D object. This method is known for its versatility and cost-effectiveness, making it suitable for producing prototypes and functional parts. In the medical field, FDM is often used to create custom prosthetics and orthotics, as well as anatomical models for surgical planning and education. Laminated Object Manufacturing (LOM) is a less common but still valuable technology in the 3D bioprinting market. LOM involves layering sheets of material, which are bonded together and cut into the desired shape using a laser or blade. This method is known for its speed and low material costs, making it suitable for producing large-scale models and prototypes. In the medical field, LOM is often used to create anatomical models and surgical guides. Other technologies in the Global Medical 3D Bioprinting Market include Selective Laser Sintering (SLS) and Digital Light Processing (DLP). SLS uses a laser to fuse powdered materials into solid structures, offering high strength and durability. This technology is often used to create functional parts and prototypes in the medical field. DLP, on the other hand, uses a digital light projector to cure liquid resin into solid layers, similar to SLA. DLP is known for its speed and precision, making it ideal for creating detailed models and prototypes. Each of these technologies plays a crucial role in the Global Medical 3D Bioprinting Market, offering unique benefits and applications that contribute to the advancement of medical research and treatment.

Medical Device Manufacturers, Pharmaceutical Companies, Others in the Global Medical 3D Bioprinting Market:

The Global Medical 3D Bioprinting Market has a wide range of applications across various sectors, including medical device manufacturers, pharmaceutical companies, and others. Medical device manufacturers are increasingly adopting 3D bioprinting technology to create customized and patient-specific devices. This technology allows for the production of complex geometries and intricate designs that are difficult to achieve with traditional manufacturing methods. By using 3D bioprinting, manufacturers can produce devices that are tailored to the unique anatomy of individual patients, improving the fit and function of implants, prosthetics, and other medical devices. This customization can lead to better patient outcomes and increased satisfaction. Pharmaceutical companies are also leveraging 3D bioprinting technology to enhance drug development and testing processes. By creating 3D-printed tissue models, researchers can study the effects of drugs on human tissues in a more accurate and controlled environment. This can lead to more effective drug formulations and a better understanding of drug interactions and side effects. Additionally, 3D bioprinting can be used to produce personalized medicine, where drugs are tailored to the specific needs of individual patients based on their genetic makeup and medical history. This approach has the potential to revolutionize the pharmaceutical industry by providing more targeted and effective treatments. Beyond medical device manufacturers and pharmaceutical companies, the Global Medical 3D Bioprinting Market also has applications in other areas, such as academic research and healthcare institutions. Academic researchers are using 3D bioprinting technology to study complex biological processes and develop new treatment methods. By creating accurate models of human tissues and organs, researchers can gain valuable insights into disease mechanisms and test new therapies in a controlled environment. Healthcare institutions are also adopting 3D bioprinting technology to improve patient care and outcomes. By using 3D-printed models for surgical planning and education, healthcare professionals can better understand complex procedures and improve surgical precision. This can lead to reduced surgical times, fewer complications, and improved patient outcomes. Overall, the Global Medical 3D Bioprinting Market is playing a crucial role in advancing medical research and treatment, offering new solutions to some of the most challenging medical problems.

Global Medical 3D Bioprinting Market Outlook:

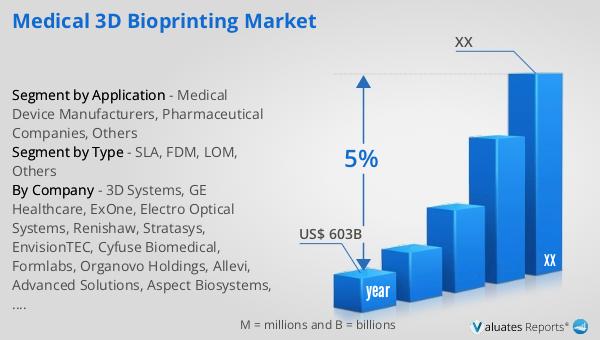

Based on our analysis, the worldwide market for medical devices is projected to reach approximately $603 billion in 2023. This substantial market size reflects the growing demand for advanced medical technologies and innovative solutions in healthcare. Over the next six years, the market is expected to expand at a compound annual growth rate (CAGR) of 5%. This steady growth indicates a robust and dynamic market environment, driven by continuous advancements in medical technology and an increasing focus on improving patient care and outcomes. The rising prevalence of chronic diseases, an aging population, and the growing need for personalized medicine are some of the key factors contributing to this market expansion. Additionally, the integration of cutting-edge technologies such as 3D bioprinting, artificial intelligence, and telemedicine is expected to further drive market growth. As healthcare systems worldwide continue to evolve and adapt to new challenges, the demand for innovative medical devices and solutions is likely to increase, creating new opportunities for market players. This positive market outlook underscores the importance of continued investment in research and development to drive innovation and meet the evolving needs of the healthcare industry.

| Report Metric | Details |

| Report Name | Medical 3D Bioprinting Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | 3D Systems, GE Healthcare, ExOne, Electro Optical Systems, Renishaw, Stratasys, EnvisionTEC, Cyfuse Biomedical, Formlabs, Organovo Holdings, Allevi, Advanced Solutions, Aspect Biosystems, CELLINK, GeSiM, Bio3D Technologies, Regenovo Biotechnology, Optomec, Mecuris, Fluicell, BigRep |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |