What is Global DNA Chip for Agriculture Market?

The Global DNA Chip for Agriculture Market is a rapidly evolving sector that leverages advanced genomic technologies to enhance agricultural productivity and sustainability. DNA chips, also known as microarrays, are tools that allow researchers to analyze the expression of thousands of genes simultaneously. In agriculture, these chips are used to study the genetic makeup of crops and livestock, enabling the identification of desirable traits such as disease resistance, drought tolerance, and improved nutritional content. By providing a comprehensive overview of genetic information, DNA chips facilitate the development of genetically superior plant varieties and animal breeds. This technology is crucial for addressing the challenges of food security and climate change, as it helps in breeding crops that can withstand harsh environmental conditions and produce higher yields. The market for DNA chips in agriculture is driven by the increasing demand for food, the need for sustainable farming practices, and advancements in biotechnology. As the global population continues to grow, the importance of DNA chips in agriculture is expected to rise, making them an indispensable tool for modern farming.

Oligonucleotide DNA Chip, Complementary DNA Chip in the Global DNA Chip for Agriculture Market:

The Global DNA Chip for Agriculture Market encompasses various types of DNA chips, including Oligonucleotide DNA Chips and Complementary DNA (cDNA) Chips, each serving distinct purposes in agricultural research. Oligonucleotide DNA Chips are composed of short, synthetic sequences of nucleotides that are designed to match specific gene sequences in the target organism. These chips are highly specific and are used for detecting single nucleotide polymorphisms (SNPs), which are variations in a single nucleotide that occur at a specific position in the genome. SNPs are crucial for identifying genetic variations that influence traits such as yield, disease resistance, and stress tolerance in crops and livestock. By analyzing SNPs, researchers can select and breed individuals with desirable traits, thereby improving the overall quality and productivity of agricultural products. On the other hand, Complementary DNA Chips are used to study gene expression patterns. These chips contain cDNA sequences that are complementary to the mRNA of the target organism. When mRNA from a sample binds to the cDNA on the chip, it indicates that the corresponding gene is being expressed. This information is vital for understanding how genes are regulated in response to environmental factors, such as drought or pest attacks, and can guide the development of crops that are more resilient to these challenges. Both types of DNA chips play a crucial role in precision agriculture, enabling farmers to make informed decisions based on genetic data. By integrating DNA chip technology into breeding programs, agricultural scientists can accelerate the development of new varieties that meet the demands of a growing population while minimizing the environmental impact of farming. The use of DNA chips also supports the conservation of genetic diversity, as it allows for the identification and preservation of rare and valuable genetic traits. As the agricultural sector continues to embrace biotechnology, the demand for DNA chips is expected to increase, driving innovation and growth in the market.

Potato, Bovine, Sheep, Rice, Others in the Global DNA Chip for Agriculture Market:

The application of Global DNA Chip for Agriculture Market technology spans various areas, including potatoes, bovines, sheep, rice, and other crops and livestock. In potato cultivation, DNA chips are used to identify genes associated with resistance to diseases such as late blight, a major threat to potato production worldwide. By selecting and breeding potato varieties with these resistant genes, farmers can reduce the reliance on chemical pesticides, leading to more sustainable farming practices. In the livestock sector, DNA chips are employed to enhance the genetic quality of bovines and sheep. For bovines, DNA chips help in identifying genetic markers linked to traits such as milk yield, growth rate, and disease resistance. This information is used to select and breed superior animals, improving the efficiency and profitability of dairy and meat production. Similarly, in sheep farming, DNA chips are used to identify genes associated with wool quality, growth, and reproductive performance, enabling the development of high-quality sheep breeds. Rice, a staple food for more than half of the world's population, also benefits from DNA chip technology. Researchers use DNA chips to study the genetic basis of traits such as yield, grain quality, and resistance to pests and diseases. By understanding the genetic factors that influence these traits, scientists can develop rice varieties that are more productive and resilient to environmental stresses. Beyond these specific applications, DNA chips are used in a wide range of other crops and livestock to enhance genetic improvement programs. For instance, in crops like wheat, maize, and soybeans, DNA chips are used to identify genes associated with yield, quality, and stress tolerance. In poultry and swine production, DNA chips help in selecting animals with desirable traits such as growth rate, feed efficiency, and disease resistance. The versatility of DNA chip technology makes it an invaluable tool for modern agriculture, enabling the development of crops and livestock that meet the demands of a growing population while ensuring environmental sustainability.

Global DNA Chip for Agriculture Market Outlook:

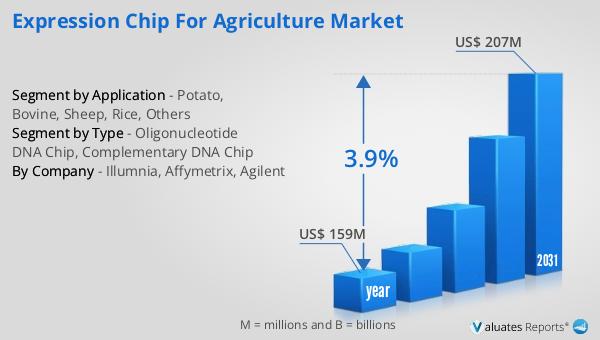

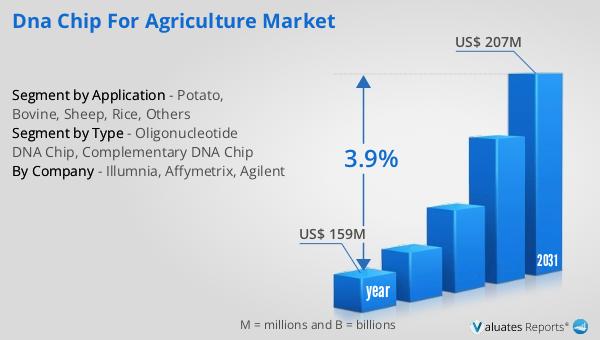

The outlook for the Global DNA Chip for Agriculture Market indicates a promising future, with the market valued at $159 million in 2024 and projected to grow to $207 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.9% during the forecast period. Despite the overall positive growth trajectory, the Asia Pacific region, which is the largest market for DNA chips in agriculture, experienced a decline of 2.0%. In contrast, the Americas showed robust growth, with sales reaching $142.1 billion, marking a 17.0% increase year-on-year. Similarly, Europe and Japan also demonstrated positive growth, with sales in Europe amounting to $53.8 billion, up 12.6% year-on-year, and sales in Japan reaching $48.1 billion, up 10.0% year-on-year. However, the Asia Pacific region, despite being the largest market, saw sales of $336.2 billion, which was a 2.0% decrease year-on-year. This mixed performance across regions highlights the varying dynamics and challenges faced by the DNA chip market in agriculture. Factors such as technological advancements, government policies, and market demand play a significant role in shaping the growth prospects of this market. As the demand for sustainable and efficient agricultural practices continues to rise, the adoption of DNA chip technology is expected to increase, driving further growth in the market.

| Report Metric | Details |

| Report Name | DNA Chip for Agriculture Market |

| Accounted market size in year | US$ 159 million |

| Forecasted market size in 2031 | US$ 207 million |

| CAGR | 3.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Illumnia, Affymetrix, Agilent |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |