What is Global Optical Grade PET Film Market?

The Global Optical Grade PET Film Market is a specialized segment within the broader polyester film industry, focusing on films that possess high optical clarity and are used in various high-tech applications. Optical Grade PET (Polyethylene Terephthalate) films are known for their excellent transparency, dimensional stability, and resistance to moisture and chemicals, making them ideal for applications that require precision and reliability. These films are extensively used in the production of displays, touch screens, and other electronic devices where clarity and durability are paramount. The market for these films is driven by the increasing demand for consumer electronics, advancements in display technologies, and the growing need for high-performance materials in various industrial applications. As technology continues to evolve, the demand for optical grade PET films is expected to rise, driven by innovations in electronics and the need for more efficient and sustainable materials. The market is characterized by a high level of competition, with numerous players striving to develop films with superior properties to meet the ever-growing demands of the industry.

Reflective Film, AR Film, Filter Film, Others in the Global Optical Grade PET Film Market:

Reflective Film, AR Film, Filter Film, and other types of films play crucial roles in the Global Optical Grade PET Film Market, each serving distinct purposes and applications. Reflective films are designed to reflect light, enhancing visibility and brightness in various applications. These films are commonly used in displays, signage, and lighting systems to improve the efficiency and effectiveness of light usage. By reflecting light, these films help in reducing energy consumption and enhancing the visual appeal of products. Anti-Reflective (AR) films, on the other hand, are engineered to minimize glare and reflections on surfaces, making them ideal for use in screens, lenses, and other optical devices. AR films enhance the viewing experience by reducing eye strain and improving clarity, especially in environments with high ambient light. Filter films are used to selectively transmit or block certain wavelengths of light, making them essential in applications like photography, displays, and scientific instruments. These films help in enhancing image quality, protecting sensitive components, and improving the overall performance of optical systems. Other types of films in this market include protective films, which are used to safeguard surfaces from scratches, dust, and other environmental factors. These films are crucial in maintaining the longevity and performance of electronic devices, displays, and other sensitive equipment. The diversity of films within the Global Optical Grade PET Film Market highlights the versatility and adaptability of PET films in meeting the specific needs of various industries. As technology advances, the demand for specialized films with unique properties is expected to grow, driving innovation and development within the market. Companies operating in this space are continually investing in research and development to create films that offer superior performance, durability, and sustainability. The competition in the market is intense, with players striving to differentiate their products through innovation and quality. The Global Optical Grade PET Film Market is poised for growth as industries continue to seek high-performance materials that can meet the demands of modern technology and consumer expectations.

Consumer Electronics, Lithium Battery, Photovoltaic Modules, Others in the Global Optical Grade PET Film Market:

The usage of Global Optical Grade PET Film Market in areas such as Consumer Electronics, Lithium Battery, Photovoltaic Modules, and others is extensive and varied, reflecting the versatility and adaptability of these films. In the realm of Consumer Electronics, optical grade PET films are indispensable due to their excellent clarity, durability, and resistance to environmental factors. They are used in the production of screens, touch panels, and protective covers, enhancing the visual quality and longevity of devices such as smartphones, tablets, and televisions. The demand for high-quality displays and touch interfaces in consumer electronics drives the need for advanced optical films that can deliver superior performance and user experience. In the Lithium Battery sector, optical grade PET films are used as separators and protective layers, contributing to the safety and efficiency of battery systems. These films provide excellent insulation and chemical resistance, ensuring the stability and reliability of lithium batteries used in various applications, including electric vehicles and portable electronics. The growing demand for energy-efficient and sustainable power solutions is fueling the need for high-performance materials like optical grade PET films in battery technology. Photovoltaic Modules also benefit from the use of optical grade PET films, which are used as protective layers to enhance the durability and efficiency of solar panels. These films help in protecting the photovoltaic cells from environmental damage, improving light transmission, and increasing the overall energy conversion efficiency of solar modules. As the demand for renewable energy sources continues to rise, the role of optical grade PET films in enhancing the performance and lifespan of photovoltaic modules becomes increasingly important. Beyond these specific applications, optical grade PET films are used in a variety of other industries, including automotive, healthcare, and packaging, where their unique properties offer significant advantages. In the automotive industry, these films are used in displays, lighting systems, and interior components, contributing to the safety, comfort, and aesthetics of vehicles. In healthcare, optical grade PET films are used in medical devices, diagnostic equipment, and protective barriers, ensuring the safety and effectiveness of healthcare solutions. The packaging industry also benefits from the use of these films, which provide excellent barrier properties, clarity, and printability, enhancing the appeal and functionality of packaging materials. The diverse applications of optical grade PET films across various industries underscore their importance as a high-performance material that meets the evolving needs of modern technology and consumer demands.

Global Optical Grade PET Film Market Outlook:

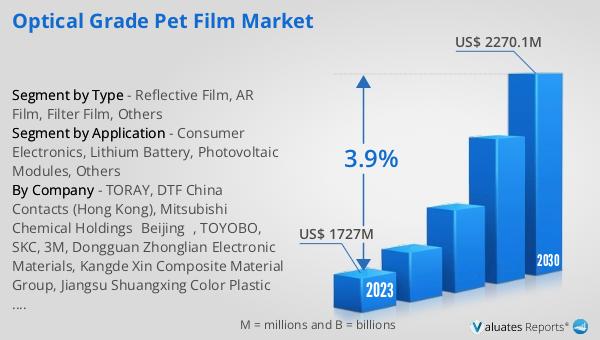

The global market for Optical Grade PET Film was valued at $1,868 million in 2024 and is anticipated to expand to a revised size of $2,432 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.9% over the forecast period. This growth trajectory underscores the increasing demand for high-quality optical films across various industries, driven by advancements in technology and the need for efficient and sustainable materials. Regionally, China stands out as the largest consumer of Optical Polyester Film globally, highlighting its significant role in the market. The rapid industrialization and technological advancements in China contribute to its position as the most promising market, with an impressive growth rate of 11%. This growth is fueled by the country's robust electronics manufacturing sector, increasing investments in renewable energy, and the rising demand for high-performance materials in various applications. The market dynamics in China reflect the broader trends in the global Optical Grade PET Film Market, where innovation, quality, and sustainability are key drivers of growth. As industries continue to evolve and consumer expectations rise, the demand for advanced optical films is expected to increase, creating new opportunities and challenges for market players. The competitive landscape is characterized by intense rivalry, with companies striving to differentiate their products through innovation, quality, and customer service. The future of the Global Optical Grade PET Film Market looks promising, with significant potential for growth and development as industries continue to seek high-performance materials that can meet the demands of modern technology and consumer expectations.

| Report Metric | Details |

| Report Name | Optical Grade PET Film Market |

| Accounted market size in year | US$ 1868 million |

| Forecasted market size in 2031 | US$ 2432 million |

| CAGR | 3.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | TORAY, DTF China Contacts (Hong Kong), Mitsubishi Chemical Holdings(Beijing), TOYOBO, SKC, 3M, Dongguan Zhonglian Electronic Materials, Kangde Xin Composite Material Group, Jiangsu Shuangxing Color Plastic New Materials, Ningbo Exciton Technology, Zhejiang Great Southeast, Sichuan EM Technology, Hangzhou Huasu Industry, China Lucky Group Corporation, Jiangsu Sidike New Materials Science&Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |