What is Global Dry Cider Market?

The Global Dry Cider Market is a fascinating segment of the broader alcoholic beverage industry, characterized by its unique production process and distinct taste profile. Dry cider is made from fermented apple juice, and unlike sweet cider, it contains little to no residual sugar, resulting in a crisp and refreshing taste. This market has been gaining traction worldwide due to the increasing consumer preference for natural and gluten-free alcoholic beverages. The appeal of dry cider lies in its versatility; it can be enjoyed on its own or used as a base for cocktails. The market is driven by a growing awareness of health and wellness, as consumers seek out beverages with lower sugar content. Additionally, the rise of craft cideries has contributed to the market's expansion, as these small-scale producers often focus on quality and innovation, offering unique flavors and blends. The global dry cider market is also influenced by regional preferences, with variations in taste and production methods across different countries. As more consumers become aware of the diverse offerings within the dry cider category, the market is expected to continue its upward trajectory, appealing to a broad range of palates and preferences.

Canned, Bottled in the Global Dry Cider Market:

In the Global Dry Cider Market, packaging plays a crucial role in influencing consumer choices, with canned and bottled options being the most prevalent. Canned dry cider has gained popularity due to its convenience, portability, and environmental benefits. Cans are lightweight, easy to transport, and ideal for outdoor activities such as picnics, barbecues, and festivals. They also offer a longer shelf life by protecting the cider from light and oxygen, which can degrade its quality. Moreover, cans are often seen as a more sustainable option, as they are highly recyclable and have a lower carbon footprint compared to glass bottles. On the other hand, bottled dry cider is often associated with premium quality and tradition. Glass bottles are perceived as more elegant and are typically used for higher-end products or those that emphasize artisanal craftsmanship. Bottles also allow for a more sophisticated presentation, making them a popular choice for formal occasions or gifting. The choice between canned and bottled cider often depends on the target market and brand positioning. Some consumers prefer the classic appeal of bottled cider, while others appreciate the modern convenience of cans. Additionally, the packaging can influence the taste perception of the cider, as some believe that glass bottles preserve the flavor better than cans. However, advancements in canning technology have addressed many of these concerns, ensuring that the taste and quality of canned cider are on par with bottled options. The decision to use cans or bottles also impacts the marketing strategy, as brands must consider factors such as shelf space, branding opportunities, and consumer preferences. For instance, cans offer more surface area for creative designs and branding, which can attract younger consumers looking for trendy and eye-catching products. In contrast, bottles provide a more traditional canvas for labels, appealing to consumers who value heritage and authenticity. Ultimately, the choice between canned and bottled dry cider is a strategic decision that reflects the brand's identity and target audience. As the global dry cider market continues to evolve, both packaging options will play a vital role in shaping consumer perceptions and driving sales.

Online Sales, Offline Sales in the Global Dry Cider Market:

The usage of the Global Dry Cider Market in online and offline sales channels highlights the evolving landscape of consumer purchasing behavior. Online sales have become increasingly important in recent years, driven by the convenience and accessibility of e-commerce platforms. Consumers can easily browse a wide range of dry cider options from the comfort of their homes, compare prices, read reviews, and make informed purchasing decisions. Online sales channels also offer cider producers the opportunity to reach a broader audience, including international markets that may not have access to their products through traditional retail outlets. Additionally, online platforms often provide valuable data and insights into consumer preferences and trends, allowing brands to tailor their offerings and marketing strategies accordingly. On the other hand, offline sales remain a significant component of the global dry cider market, particularly in regions where consumers prefer to purchase alcoholic beverages in person. Brick-and-mortar stores, such as supermarkets, liquor stores, and specialty shops, offer consumers the opportunity to physically examine products, seek advice from knowledgeable staff, and discover new brands through in-store promotions and tastings. Offline sales channels also play a crucial role in building brand loyalty and trust, as consumers often associate physical stores with reliability and quality assurance. Furthermore, the social aspect of shopping in physical stores can enhance the overall purchasing experience, as consumers enjoy browsing with friends or family and making spontaneous buying decisions. The integration of online and offline sales channels, known as omnichannel retailing, is becoming increasingly important in the global dry cider market. Brands that successfully leverage both channels can provide a seamless and cohesive shopping experience, catering to the diverse preferences of modern consumers. For example, some cider producers offer online ordering with in-store pickup options, allowing consumers to enjoy the convenience of online shopping while still experiencing the benefits of offline retail. As the global dry cider market continues to grow, the interplay between online and offline sales channels will be crucial in shaping consumer behavior and driving market expansion.

Global Dry Cider Market Outlook:

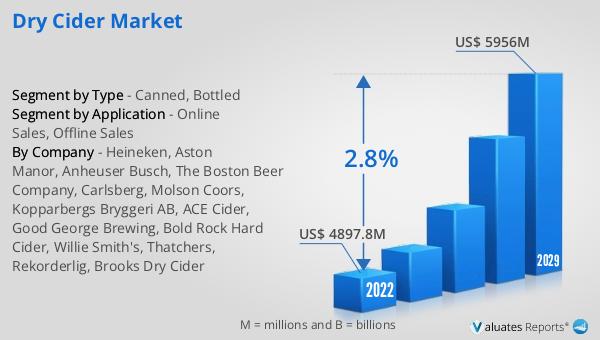

The outlook for the Global Dry Cider Market is promising, with projections indicating significant growth in the coming years. The market is expected to reach a value of approximately $5,956 million by 2029, up from $4,897.8 million in 2022. This growth represents a compound annual growth rate (CAGR) of 2.8% from 2023 to 2029. This upward trend can be attributed to several factors, including the increasing consumer demand for healthier and more natural beverage options. As more people become health-conscious, they are turning to dry cider as a lower-calorie alternative to other alcoholic drinks. Additionally, the rise of craft cideries and the introduction of innovative flavors and blends have attracted a wider audience, further driving market growth. The expansion of distribution channels, both online and offline, has also played a significant role in the market's positive outlook. With the convenience of online shopping and the continued importance of physical retail spaces, consumers have more access to dry cider than ever before. As the market continues to evolve, producers are likely to focus on sustainability and quality, appealing to environmentally conscious consumers and those seeking premium products. Overall, the Global Dry Cider Market is poised for steady growth, driven by changing consumer preferences and the ongoing innovation within the industry.

| Report Metric | Details |

| Report Name | Dry Cider Market |

| Accounted market size in 2022 | US$ 4897.8 million |

| Forecasted market size in 2029 | US$ 5956 million |

| CAGR | 2.8% |

| Base Year | 2022 |

| Forecasted years | 2025 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Heineken, Aston Manor, Anheuser Busch, The Boston Beer Company, Carlsberg, Molson Coors, Kopparbergs Bryggeri AB, ACE Cider, Good George Brewing, Bold Rock Hard Cider, Willie Smith's, Thatchers, Rekorderlig, Brooks Dry Cider |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |