What is Global Airplane Starter Generators Market?

The Global Airplane Starter Generators Market is a crucial segment within the aerospace industry, focusing on the production and distribution of starter generators used in aircraft. These devices are essential for starting the engines of airplanes and providing electrical power during flight. The market encompasses a wide range of products, including both AC (alternating current) and DC (direct current) starter generators, catering to various types of aircraft, from commercial airliners to military jets and private planes. The demand for airplane starter generators is driven by the increasing number of aircraft in operation worldwide, advancements in aviation technology, and the need for reliable and efficient power systems. Manufacturers in this market are continuously innovating to improve the performance, durability, and efficiency of their products, while also focusing on reducing weight and emissions to meet stringent environmental regulations. The market is characterized by a mix of established players and new entrants, with competition based on factors such as product quality, technological innovation, and customer service. As the aviation industry continues to grow, the Global Airplane Starter Generators Market is expected to expand, offering numerous opportunities for companies involved in the production and supply of these critical components.

AC, DC in the Global Airplane Starter Generators Market:

In the Global Airplane Starter Generators Market, AC and DC starter generators play pivotal roles, each with distinct characteristics and applications. AC starter generators are primarily used in larger aircraft, such as commercial airliners and military transport planes, due to their ability to handle higher power loads and provide stable electrical output over long distances. These generators convert mechanical energy from the aircraft's engines into electrical energy, which is then distributed throughout the aircraft's systems. AC systems are favored for their efficiency in transmitting power over long distances and their ability to support complex electrical systems, making them ideal for large aircraft with extensive electrical needs. On the other hand, DC starter generators are commonly used in smaller aircraft, such as private jets and helicopters, where the electrical demands are lower, and the systems are less complex. DC generators are known for their simplicity, reliability, and ease of maintenance, making them a popular choice for smaller aircraft that require a straightforward and dependable power source. The choice between AC and DC starter generators depends on various factors, including the size and type of aircraft, the complexity of its electrical systems, and the specific power requirements. In recent years, there has been a growing trend towards hybrid systems that combine the benefits of both AC and DC technologies, offering enhanced performance and flexibility. These hybrid systems are designed to optimize power distribution and improve overall efficiency, catering to the evolving needs of modern aircraft. As the aviation industry continues to advance, the demand for both AC and DC starter generators is expected to rise, driven by the increasing number of aircraft in operation and the ongoing development of new aviation technologies. Manufacturers in the Global Airplane Starter Generators Market are investing in research and development to create innovative solutions that meet the diverse needs of their customers, while also addressing environmental concerns and regulatory requirements. This focus on innovation and sustainability is shaping the future of the market, with companies striving to deliver high-quality, efficient, and eco-friendly products that enhance the performance and reliability of aircraft worldwide.

Aircraft Utility Management, Configuration Management, Flight Control and Operations in the Global Airplane Starter Generators Market:

The usage of Global Airplane Starter Generators Market extends to several critical areas, including Aircraft Utility Management, Configuration Management, Flight Control, and Operations. In Aircraft Utility Management, starter generators are essential for powering various onboard systems, such as lighting, heating, and air conditioning, ensuring passenger comfort and safety during flights. These generators provide a stable and reliable source of electrical power, enabling the seamless operation of utility systems and enhancing the overall flight experience. In Configuration Management, starter generators play a vital role in maintaining the integrity and performance of an aircraft's electrical systems. They ensure that all components are functioning correctly and efficiently, allowing for precise control and monitoring of the aircraft's configuration. This is particularly important in modern aircraft, where complex electrical systems require constant oversight to maintain optimal performance and safety. In Flight Control, starter generators are crucial for powering the electronic systems that manage the aircraft's flight operations, including navigation, communication, and autopilot functions. These systems rely on a consistent and reliable power supply to operate effectively, and starter generators provide the necessary electrical energy to support these critical functions. In Operations, starter generators are used to start the aircraft's engines and provide power during ground operations, such as taxiing and pre-flight checks. They ensure that the aircraft is ready for takeoff and can operate efficiently throughout the flight, minimizing delays and enhancing operational efficiency. The Global Airplane Starter Generators Market is integral to the aviation industry, providing the essential power systems that enable safe, efficient, and reliable aircraft operations. As the demand for air travel continues to grow, the market for starter generators is expected to expand, driven by the need for advanced and efficient power solutions that meet the evolving requirements of modern aircraft.

Global Airplane Starter Generators Market Outlook:

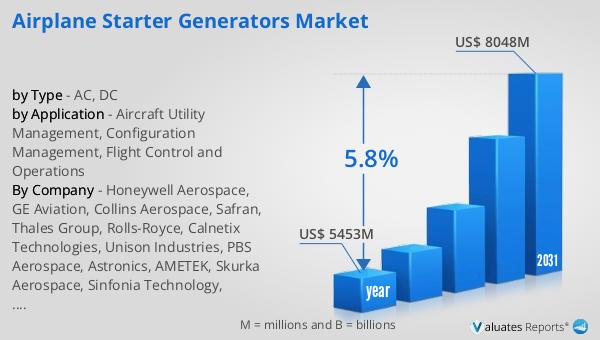

The global market for Airplane Starter Generators was valued at $5,453 million in 2024, and it is anticipated to grow significantly, reaching an estimated value of $8,048 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.8% over the forecast period. The increasing demand for air travel, coupled with advancements in aviation technology, is driving the expansion of this market. As more aircraft are introduced into service, the need for reliable and efficient starter generators becomes paramount, fueling market growth. Additionally, the focus on reducing emissions and improving fuel efficiency is prompting manufacturers to develop innovative solutions that meet stringent environmental regulations. The market is characterized by intense competition, with companies striving to offer high-quality products that enhance the performance and reliability of aircraft. As the aviation industry continues to evolve, the Global Airplane Starter Generators Market is poised for significant growth, offering numerous opportunities for companies involved in the production and supply of these critical components.

| Report Metric | Details |

| Report Name | Airplane Starter Generators Market |

| Accounted market size in year | US$ 5453 million |

| Forecasted market size in 2031 | US$ 8048 million |

| CAGR | 5.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Honeywell Aerospace, GE Aviation, Collins Aerospace, Safran, Thales Group, Rolls-Royce, Calnetix Technologies, Unison Industries, PBS Aerospace, Astronics, AMETEK, Skurka Aerospace, Sinfonia Technology, ePropelled, Denis Ferranti Group, Plane-Power, NAASCO, TAE Aerospace, HEICO Repair Group, Aerotech of Louisville |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |