What is Global IoT-Enabled Smart Lighting Market?

The Global IoT-Enabled Smart Lighting Market refers to the rapidly evolving sector that integrates the Internet of Things (IoT) technology with lighting systems to create intelligent, energy-efficient, and automated lighting solutions. This market is driven by the increasing demand for energy conservation, the need for enhanced security, and the growing adoption of smart city initiatives worldwide. IoT-enabled smart lighting systems allow for remote control and monitoring of lighting fixtures through connected devices such as smartphones, tablets, or computers. These systems can adjust lighting based on occupancy, daylight availability, and user preferences, leading to significant energy savings and reduced operational costs. Additionally, they offer features like dimming, color tuning, and scheduling, which enhance user comfort and convenience. The integration of IoT technology in lighting systems also facilitates data collection and analysis, enabling predictive maintenance and improved asset management. As urbanization continues to rise and technology advances, the Global IoT-Enabled Smart Lighting Market is poised for substantial growth, transforming how we illuminate our homes, offices, and public spaces.

Wi-Fi, Z-Wave, ZigBee, Bluetooth, Enocean in the Global IoT-Enabled Smart Lighting Market:

In the Global IoT-Enabled Smart Lighting Market, various communication protocols play a crucial role in ensuring seamless connectivity and interoperability among devices. Wi-Fi is one of the most widely used protocols, offering high-speed internet access and enabling smart lighting systems to connect to the internet and other devices within a network. It allows users to control their lighting systems remotely via mobile apps or voice assistants, providing convenience and flexibility. However, Wi-Fi can consume more power compared to other protocols, which may not be ideal for battery-operated devices. Z-Wave is another popular protocol, known for its low power consumption and reliable mesh networking capabilities. It operates on a different frequency than Wi-Fi, reducing interference and ensuring stable connections. Z-Wave is particularly favored in home automation systems, allowing for easy integration of smart lighting with other IoT devices. ZigBee, similar to Z-Wave, is a low-power, mesh networking protocol that supports a wide range of IoT applications, including smart lighting. It is designed to handle large networks with multiple devices, making it suitable for both residential and commercial settings. ZigBee's interoperability with various manufacturers' products enhances its appeal in the smart lighting market. Bluetooth, traditionally used for short-range communication, has evolved with the introduction of Bluetooth Low Energy (BLE), which offers reduced power consumption and extended range. BLE is increasingly being adopted in smart lighting solutions, enabling direct communication between devices without the need for a central hub. This makes it an attractive option for simple, cost-effective smart lighting setups. Lastly, EnOcean is a unique protocol that focuses on energy harvesting, allowing devices to operate without batteries by utilizing energy from their surroundings, such as light, motion, or temperature changes. EnOcean's self-powered technology is particularly advantageous in smart lighting applications, where maintenance-free operation is desired. Each of these protocols has its strengths and limitations, and the choice of protocol often depends on specific application requirements, such as range, power consumption, and network size. As the Global IoT-Enabled Smart Lighting Market continues to expand, the development and adoption of these communication protocols will play a pivotal role in shaping the future of smart lighting solutions.

Residential, Commercial Buildings, Government Offices and Building, Street Lighting, Others in the Global IoT-Enabled Smart Lighting Market:

The Global IoT-Enabled Smart Lighting Market finds extensive applications across various sectors, including residential, commercial buildings, government offices and buildings, street lighting, and others. In residential settings, smart lighting systems offer homeowners the ability to customize their lighting environments to suit their preferences and lifestyles. Features such as remote control, scheduling, and automation enhance convenience and energy efficiency, allowing users to reduce electricity consumption and lower utility bills. In commercial buildings, smart lighting solutions contribute to creating a productive and comfortable work environment. By integrating with building management systems, these lighting systems can adjust based on occupancy and daylight availability, optimizing energy usage and reducing operational costs. Additionally, smart lighting can enhance security through features like motion detection and integration with surveillance systems. Government offices and buildings benefit from IoT-enabled smart lighting by improving energy efficiency and reducing maintenance costs. These systems can be programmed to operate only when needed, minimizing energy wastage and extending the lifespan of lighting fixtures. In street lighting, smart solutions offer significant advantages in terms of energy savings and improved public safety. IoT-enabled streetlights can adjust brightness based on traffic and pedestrian activity, ensuring well-lit streets while conserving energy. They can also be monitored and controlled remotely, allowing for quick response to maintenance issues and reducing downtime. Other areas where smart lighting is making an impact include industrial facilities, healthcare institutions, and educational campuses. In industrial settings, smart lighting can enhance safety and productivity by providing optimal illumination levels for various tasks. In healthcare, smart lighting systems can support patient well-being by simulating natural light patterns and reducing glare. Educational institutions can benefit from smart lighting by creating adaptable learning environments that improve concentration and comfort for students and staff. Overall, the Global IoT-Enabled Smart Lighting Market is transforming how lighting is utilized across different sectors, offering innovative solutions that enhance energy efficiency, user experience, and operational efficiency.

Global IoT-Enabled Smart Lighting Market Outlook:

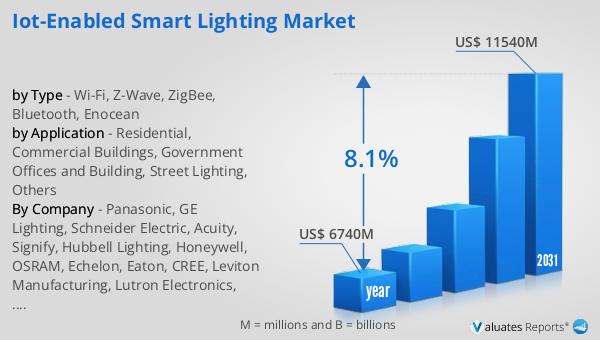

The global market for IoT-Enabled Smart Lighting was valued at $6,740 million in 2024 and is anticipated to grow significantly, reaching an estimated size of $11,540 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 8.1% over the forecast period. The increasing demand for energy-efficient lighting solutions, coupled with the rising adoption of smart city initiatives, is driving this market expansion. IoT-enabled smart lighting systems offer numerous benefits, including reduced energy consumption, enhanced security, and improved user convenience, which are contributing to their growing popularity across various sectors. As urbanization continues to rise and technology advances, the integration of IoT technology in lighting systems is becoming more prevalent, transforming how we illuminate our homes, offices, and public spaces. The market's growth is also supported by the development of advanced communication protocols, such as Wi-Fi, Z-Wave, ZigBee, Bluetooth, and EnOcean, which enable seamless connectivity and interoperability among smart lighting devices. As a result, the Global IoT-Enabled Smart Lighting Market is poised for substantial growth, offering innovative solutions that enhance energy efficiency, user experience, and operational efficiency.

| Report Metric | Details |

| Report Name | IoT-Enabled Smart Lighting Market |

| Accounted market size in year | US$ 6740 million |

| Forecasted market size in 2031 | US$ 11540 million |

| CAGR | 8.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Panasonic, GE Lighting, Schneider Electric, Acuity, Signify, Hubbell Lighting, Honeywell, OSRAM, Echelon, Eaton, CREE, Leviton Manufacturing, Lutron Electronics, TVILIGHT, Cimcon, Telematics, Legrand, Petra Systems |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |