What is Global Photovoltaic N-type Cell Market?

The Global Photovoltaic N-type Cell Market is a rapidly evolving sector within the renewable energy industry, focusing on the development and deployment of advanced solar cell technologies. Photovoltaic N-type cells are a type of solar cell that uses N-type silicon as the base material, which is known for its superior efficiency and performance compared to traditional P-type cells. These cells are designed to convert sunlight into electricity more effectively, making them a popular choice for various solar energy applications. The market for these cells is driven by the increasing demand for clean and sustainable energy solutions, as well as advancements in solar technology that enhance the efficiency and cost-effectiveness of solar panels. As countries around the world strive to reduce their carbon footprint and transition to renewable energy sources, the demand for high-efficiency solar cells like N-type cells is expected to grow significantly. This market is characterized by continuous innovation, with companies investing in research and development to improve cell efficiency, reduce production costs, and expand the applications of photovoltaic technology. Overall, the Global Photovoltaic N-type Cell Market plays a crucial role in the global shift towards sustainable energy and the reduction of greenhouse gas emissions.

TOPCon, HJT, IBC in the Global Photovoltaic N-type Cell Market:

TOPCon, HJT, and IBC are three advanced technologies within the Global Photovoltaic N-type Cell Market, each offering unique benefits and challenges. TOPCon, or Tunnel Oxide Passivated Contact, is a technology that enhances the efficiency of solar cells by reducing recombination losses at the cell's surface. This is achieved by adding a thin layer of oxide between the silicon wafer and the metal contact, which allows for better electron flow and reduces energy loss. TOPCon cells are known for their high efficiency and are increasingly being adopted in large-scale solar projects. HJT, or Heterojunction Technology, combines the best features of crystalline silicon and thin-film solar cells. It involves layering thin-film amorphous silicon on top of crystalline silicon, which results in higher efficiency and better performance in low-light conditions. HJT cells are also known for their lower temperature coefficient, meaning they perform better in high-temperature environments. However, the production process for HJT cells is more complex and costly, which can be a barrier to widespread adoption. IBC, or Interdigitated Back Contact, is another high-efficiency solar cell technology that places all the electrical contacts on the back of the cell. This design eliminates shading on the front of the cell, allowing for more sunlight absorption and higher efficiency. IBC cells are known for their excellent performance and aesthetic appeal, making them a popular choice for residential and commercial applications. However, like HJT, IBC cells are more expensive to produce, which can limit their market penetration. Despite the challenges, these technologies represent significant advancements in solar cell efficiency and are expected to play a key role in the future of the Global Photovoltaic N-type Cell Market. As the demand for renewable energy continues to grow, the development and adoption of these advanced technologies will be crucial in meeting global energy needs and reducing carbon emissions.

PV Power Station, Commercial, Residential in the Global Photovoltaic N-type Cell Market:

The Global Photovoltaic N-type Cell Market finds extensive usage across various sectors, including PV power stations, commercial, and residential applications. In PV power stations, N-type cells are utilized to generate large-scale solar power. These power stations, often referred to as solar farms, are designed to produce electricity on a massive scale, feeding it into the grid to supply power to homes and businesses. The high efficiency and durability of N-type cells make them ideal for such applications, as they can generate more electricity from the same amount of sunlight compared to traditional solar cells. This efficiency translates into lower costs per watt of electricity produced, making solar power stations a viable and competitive alternative to fossil fuel-based power plants. In commercial applications, N-type cells are used to power businesses and industrial facilities. Companies are increasingly turning to solar energy to reduce their carbon footprint and energy costs. The high efficiency of N-type cells means that businesses can generate more power from smaller installations, maximizing the use of available space. This is particularly beneficial for businesses with limited roof space or those located in urban areas where land is at a premium. Additionally, the reliability and long lifespan of N-type cells make them a cost-effective choice for commercial solar installations. In residential applications, N-type cells are used to power homes, providing a clean and sustainable energy source for everyday use. Homeowners are increasingly adopting solar energy to reduce their reliance on the grid and lower their electricity bills. The high efficiency of N-type cells means that homeowners can generate more power from smaller systems, making solar energy accessible to a wider range of households. Furthermore, the aesthetic appeal of certain N-type cell technologies, such as IBC, makes them an attractive option for residential installations. Overall, the Global Photovoltaic N-type Cell Market plays a crucial role in the transition to renewable energy across various sectors, providing efficient and sustainable energy solutions for power stations, businesses, and homes.

Global Photovoltaic N-type Cell Market Outlook:

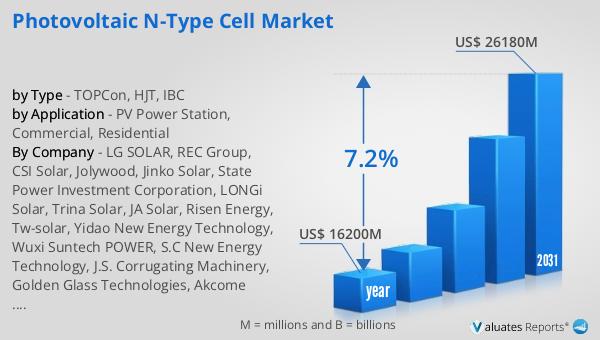

The global market for Photovoltaic N-type Cells was valued at $16.2 billion in 2024 and is anticipated to grow to a revised size of $26.18 billion by 2031, reflecting a compound annual growth rate (CAGR) of 7.2% over the forecast period. This growth is indicative of the increasing demand for high-efficiency solar cells as the world shifts towards renewable energy sources. The market's expansion is driven by technological advancements in solar cell efficiency, cost reductions in production, and the growing need for sustainable energy solutions. As countries worldwide aim to reduce their carbon emissions and transition to cleaner energy, the demand for photovoltaic N-type cells is expected to rise significantly. These cells offer superior performance and efficiency compared to traditional solar cells, making them an attractive option for various applications, including power stations, commercial, and residential installations. The projected growth of the market underscores the importance of continued innovation and investment in solar technology to meet the global energy demand and address environmental challenges. As the market evolves, companies are likely to focus on enhancing cell efficiency, reducing production costs, and expanding the applications of photovoltaic technology to maintain a competitive edge and capitalize on the growing demand for renewable energy.

| Report Metric | Details |

| Report Name | Photovoltaic N-type Cell Market |

| Accounted market size in year | US$ 16200 million |

| Forecasted market size in 2031 | US$ 26180 million |

| CAGR | 7.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | LG SOLAR, REC Group, CSI Solar, Jolywood, Jinko Solar, State Power Investment Corporation, LONGi Solar, Trina Solar, JA Solar, Risen Energy, Tw-solar, Yidao New Energy Technology, Wuxi Suntech POWER, S.C New Energy Technology, J.S. Corrugating Machinery, Golden Glass Technologies, Akcome Science and Technology, Maxwell Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |