What is Global Automotive Fuel Injectors Market?

The Global Automotive Fuel Injectors Market is a crucial segment of the automotive industry, focusing on the development and distribution of fuel injectors used in vehicles worldwide. Fuel injectors are essential components in modern engines, responsible for delivering fuel into the combustion chamber with precision and efficiency. This market has seen significant growth due to the increasing demand for fuel-efficient vehicles and stringent emission regulations imposed by governments globally. Technological advancements have led to the development of more sophisticated fuel injection systems, enhancing engine performance and reducing emissions. The market encompasses various types of fuel injectors, including gasoline and diesel direct injection systems, catering to different vehicle types and engine configurations. As the automotive industry continues to evolve, the demand for advanced fuel injectors is expected to rise, driven by the need for improved fuel economy and reduced environmental impact. The market's growth is also supported by the rising production of vehicles in emerging economies, where the automotive sector is expanding rapidly. Overall, the Global Automotive Fuel Injectors Market plays a vital role in shaping the future of automotive technology, contributing to the development of cleaner and more efficient vehicles.

Gasoline Direct Injection, Diesel Direct Injection in the Global Automotive Fuel Injectors Market:

Gasoline Direct Injection (GDI) and Diesel Direct Injection (DDI) are two prominent technologies within the Global Automotive Fuel Injectors Market, each offering unique benefits and applications. Gasoline Direct Injection is a technology that injects fuel directly into the combustion chamber of each cylinder, allowing for more precise control over the fuel-air mixture. This precision leads to improved fuel efficiency, increased power output, and reduced emissions compared to traditional port fuel injection systems. GDI systems are particularly popular in passenger cars, where manufacturers strive to balance performance with fuel economy. The technology enables engines to operate with higher compression ratios, enhancing thermal efficiency and power delivery. Additionally, GDI systems contribute to a reduction in carbon dioxide emissions, aligning with global efforts to combat climate change. On the other hand, Diesel Direct Injection is a technology used primarily in diesel engines, which are known for their fuel efficiency and torque. DDI systems inject fuel directly into the combustion chamber at high pressure, resulting in better atomization and more complete combustion. This leads to improved fuel efficiency and lower emissions of nitrogen oxides and particulate matter. Diesel engines equipped with DDI systems are commonly found in light and heavy commercial vehicles, where durability and fuel economy are critical. The adoption of DDI technology has been driven by the need to meet stringent emission standards while maintaining the inherent advantages of diesel engines. Both GDI and DDI technologies have undergone significant advancements, with manufacturers investing in research and development to enhance their performance and reliability. Innovations such as turbocharging and variable valve timing have been integrated with these injection systems to further optimize engine efficiency and power output. The Global Automotive Fuel Injectors Market continues to evolve as automakers seek to develop engines that meet the demands of modern consumers and regulatory bodies. As a result, GDI and DDI technologies are expected to play a pivotal role in the future of automotive engineering, contributing to the creation of vehicles that are both environmentally friendly and high-performing.

Passenger Cars, Light Commercial Vehicle, Heavy Commercial Vehicle in the Global Automotive Fuel Injectors Market:

The usage of Global Automotive Fuel Injectors Market spans across various vehicle categories, including passenger cars, light commercial vehicles, and heavy commercial vehicles, each with distinct requirements and applications. In passenger cars, fuel injectors are crucial for achieving the balance between performance and fuel efficiency that consumers demand. Gasoline Direct Injection systems are particularly prevalent in this segment, as they offer the precision needed to optimize fuel consumption and reduce emissions. The integration of advanced fuel injectors in passenger cars has led to the development of smaller, more powerful engines that deliver superior performance without compromising on fuel economy. This is especially important in urban areas, where stop-and-go traffic necessitates efficient fuel management. In light commercial vehicles, which are often used for delivery and transportation services, fuel injectors play a vital role in ensuring reliability and cost-effectiveness. Diesel Direct Injection systems are commonly used in this category due to their ability to provide high torque and fuel efficiency, essential for vehicles that frequently carry heavy loads. The durability and longevity of DDI systems make them ideal for light commercial vehicles, which require engines that can withstand rigorous use over extended periods. In heavy commercial vehicles, such as trucks and buses, fuel injectors are critical for maintaining operational efficiency and meeting stringent emission standards. Diesel engines dominate this segment, and the use of advanced DDI systems ensures that these vehicles can deliver the power and performance needed for long-haul transportation while minimizing fuel consumption and emissions. The Global Automotive Fuel Injectors Market continues to innovate, with manufacturers developing injectors that can handle the demands of modern heavy-duty engines. This includes the ability to operate at higher pressures and temperatures, enhancing combustion efficiency and reducing the environmental impact of heavy commercial vehicles. Overall, the application of fuel injectors across these vehicle categories highlights their importance in the automotive industry, driving advancements in engine technology and contributing to the development of more efficient and sustainable transportation solutions.

Global Automotive Fuel Injectors Market Outlook:

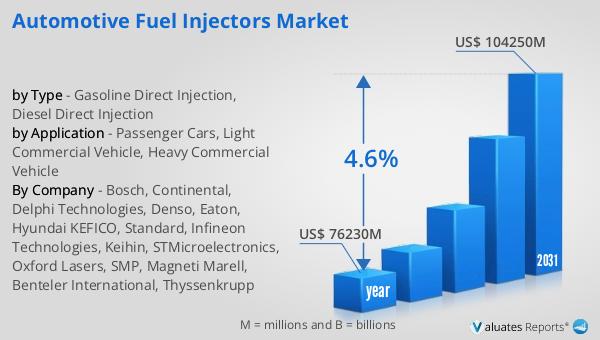

The global market for automotive fuel injectors is experiencing a notable upward trajectory. In 2024, the market was valued at approximately US$ 76,230 million. This substantial valuation underscores the critical role that fuel injectors play in the automotive industry, serving as a key component in enhancing vehicle performance and efficiency. Looking ahead, the market is projected to expand significantly, reaching an estimated size of US$ 104,250 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.6% over the forecast period. The steady increase in market size can be attributed to several factors, including the rising demand for fuel-efficient vehicles, advancements in fuel injection technology, and stringent emission regulations worldwide. As automakers strive to meet these demands, the adoption of advanced fuel injectors is expected to rise, further driving market growth. The projected expansion of the Global Automotive Fuel Injectors Market reflects the ongoing evolution of the automotive industry, where innovation and sustainability are at the forefront. As the market continues to grow, it will play a pivotal role in shaping the future of automotive technology, contributing to the development of cleaner, more efficient vehicles that meet the needs of consumers and regulatory bodies alike.

| Report Metric | Details |

| Report Name | Automotive Fuel Injectors Market |

| Accounted market size in year | US$ 76230 million |

| Forecasted market size in 2031 | US$ 104250 million |

| CAGR | 4.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bosch, Continental, Delphi Technologies, Denso, Eaton, Hyundai KEFICO, Standard, Infineon Technologies, Keihin, STMicroelectronics, Oxford Lasers, SMP, Magneti Marell, Benteler International, Thyssenkrupp |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |