What is Global Tinplate Packaging Market?

The Global Tinplate Packaging Market refers to the worldwide industry focused on the production and utilization of tinplate materials for packaging purposes. Tinplate is a thin steel sheet coated with a layer of tin, which provides a corrosion-resistant, non-toxic, and highly durable surface. This makes it an ideal choice for packaging a wide range of products, including food, beverages, and industrial goods. The market is driven by the increasing demand for sustainable and recyclable packaging solutions, as tinplate is 100% recyclable without any loss of quality. Additionally, the growing consumer preference for convenient and long-lasting packaging options further fuels the market's expansion. Tinplate packaging is widely used in the food and beverage industry for cans, closures, and containers, ensuring product safety and extending shelf life. The market is also influenced by technological advancements in manufacturing processes, which enhance the quality and efficiency of tinplate production. As environmental concerns continue to rise, the Global Tinplate Packaging Market is expected to witness significant growth, driven by the need for eco-friendly packaging alternatives.

Prime Grade Tinplate, Secondary Grade Tinplate, Others in the Global Tinplate Packaging Market:

Prime Grade Tinplate, Secondary Grade Tinplate, and Others are classifications within the Global Tinplate Packaging Market that denote the quality and intended use of the tinplate material. Prime Grade Tinplate is the highest quality tinplate available, characterized by its superior surface finish, uniform thickness, and excellent formability. It is primarily used in applications where aesthetics and performance are critical, such as in the packaging of premium food and beverage products. The high-quality finish of Prime Grade Tinplate ensures that the packaging is not only functional but also visually appealing, making it suitable for products that require a high level of presentation. On the other hand, Secondary Grade Tinplate is a slightly lower quality tinplate that may have minor imperfections or variations in thickness. Despite these minor defects, Secondary Grade Tinplate is still highly functional and is often used in applications where the appearance of the packaging is less critical. This includes industrial packaging, where the primary focus is on durability and protection rather than aesthetics. The cost-effectiveness of Secondary Grade Tinplate makes it an attractive option for manufacturers looking to balance quality and budget. The "Others" category in the Global Tinplate Packaging Market includes various grades of tinplate that do not fit into the Prime or Secondary classifications. This category may encompass specialty tinplates designed for specific applications or those with unique properties tailored to meet particular industry requirements. For instance, some tinplates may be engineered to offer enhanced resistance to corrosion or to withstand extreme temperatures, making them suitable for specialized packaging needs. The diversity within the "Others" category allows manufacturers to select tinplate materials that best align with their specific packaging requirements, ensuring optimal performance and cost-efficiency. Overall, the classification of tinplate into Prime Grade, Secondary Grade, and Others provides manufacturers with a range of options to choose from, depending on their specific needs and budget constraints. This flexibility is crucial in a market where packaging requirements can vary significantly across different industries and product types. As the Global Tinplate Packaging Market continues to evolve, the demand for high-quality, versatile tinplate materials is expected to grow, driven by the need for innovative and sustainable packaging solutions.

Packaging, Electronics, Engineering, Construction, Other in the Global Tinplate Packaging Market:

The Global Tinplate Packaging Market finds extensive usage across various sectors, including Packaging, Electronics, Engineering, Construction, and Others, each leveraging the unique properties of tinplate to meet specific industry needs. In the Packaging sector, tinplate is predominantly used for manufacturing cans, closures, and containers for food and beverages. Its excellent barrier properties protect contents from contamination and extend shelf life, making it a preferred choice for packaging perishable goods. The recyclability of tinplate also aligns with the growing demand for sustainable packaging solutions, further boosting its adoption in the packaging industry. In the Electronics sector, tinplate is used for shielding electronic components from electromagnetic interference and providing structural support. Its conductive properties and durability make it suitable for use in electronic enclosures and housings, ensuring the protection and longevity of sensitive electronic devices. The Engineering sector utilizes tinplate for its strength and formability, which are essential for manufacturing components that require precision and durability. Tinplate's resistance to corrosion and wear makes it ideal for producing parts that are exposed to harsh environments or require a high degree of reliability. In the Construction sector, tinplate is used for roofing, cladding, and other architectural applications where its aesthetic appeal and weather resistance are valued. The versatility of tinplate allows it to be used in both functional and decorative applications, contributing to the overall design and durability of construction projects. The "Others" category encompasses a wide range of applications where tinplate's unique properties are leveraged to meet specific industry requirements. This includes the production of toys, household goods, and automotive components, where tinplate's strength, formability, and corrosion resistance are essential. The diverse applications of tinplate across these sectors highlight its versatility and adaptability, making it a valuable material in the global market. As industries continue to seek innovative and sustainable solutions, the demand for tinplate is expected to grow, driven by its ability to meet the evolving needs of various sectors.

Global Tinplate Packaging Market Outlook:

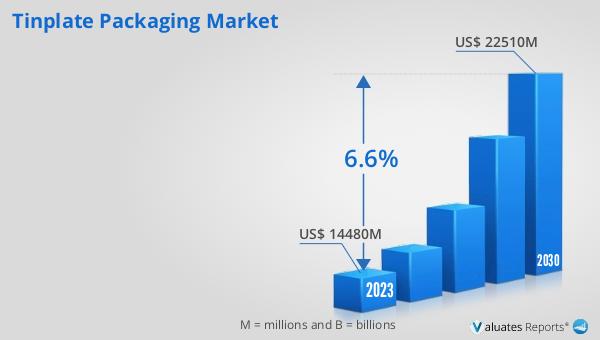

The global Tinplate Packaging market is anticipated to experience significant growth over the coming years. Starting from an estimated value of US$ 15,340 million in 2024, it is projected to reach approximately US$ 22,510 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 6.6% during the forecast period. This upward trend is indicative of the increasing demand for tinplate packaging solutions across various industries. The market's expansion can be attributed to several factors, including the rising consumer preference for sustainable and recyclable packaging options, as well as the growing need for durable and long-lasting packaging materials. Tinplate's unique properties, such as its excellent barrier protection, corrosion resistance, and recyclability, make it an attractive choice for manufacturers looking to enhance the quality and sustainability of their packaging solutions. Additionally, advancements in manufacturing technologies are expected to further boost the market by improving the efficiency and quality of tinplate production. As environmental concerns continue to drive the demand for eco-friendly packaging alternatives, the global Tinplate Packaging market is poised for robust growth, offering significant opportunities for manufacturers and stakeholders in the industry.

| Report Metric | Details |

| Report Name | Tinplate Packaging Market |

| Accounted market size in 2024 | US$ 15340 million |

| Forecasted market size in 2030 | US$ 22510 million |

| CAGR | 6.6 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | ArcelorMittal, NSSMC, U.S. Steel, JFE, ThyssenKrupp, POSCO, TCILTATA Steel, Tonyi, Massilly, Berlin Metal, Toyo Kohan, Titan Steel, Baosteel, Qifeng Group Corporation, Sino East, Guangnan, WISCO, Hebei Iron, Steeland |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |