What is LPDDR Chips - Global Market?

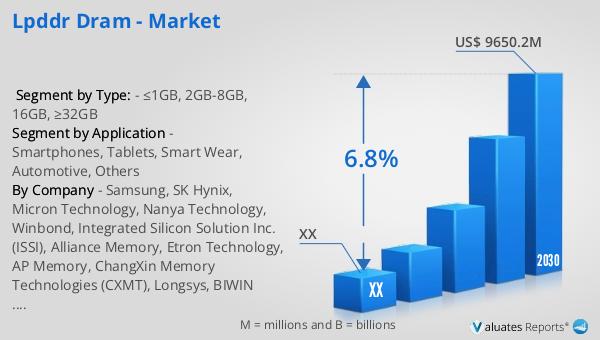

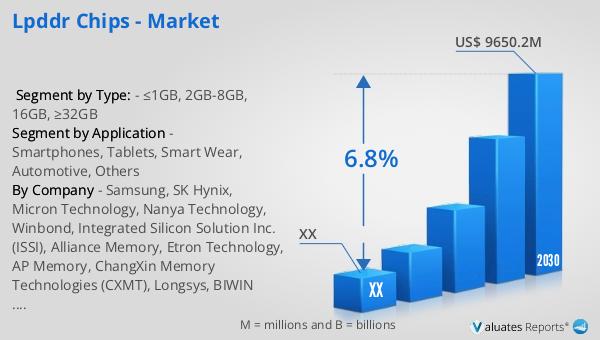

LPDDR chips, or Low Power Double Data Rate chips, are a type of dynamic random-access memory (DRAM) specifically designed to consume less power while maintaining high performance. These chips are crucial in devices where energy efficiency is paramount, such as smartphones, tablets, and other portable electronics. The global market for LPDDR chips has been growing steadily, driven by the increasing demand for energy-efficient memory solutions in various applications. In 2023, the market was valued at approximately US$ 6,817 million, and it is projected to expand to a size of US$ 9,650.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.8% from 2024 to 2030. This growth is fueled by advancements in technology and the rising need for devices that can perform complex tasks without draining battery life quickly. As more industries adopt these chips for their low power consumption and high efficiency, the market is expected to continue its upward trajectory, offering numerous opportunities for innovation and development in the field of memory technology.

≤1GB, 2GB-8GB, 16GB, ≥32GB in the LPDDR Chips - Global Market:

In the LPDDR chips global market, memory capacities are categorized into different segments, including ≤1GB, 2GB-8GB, 16GB, and ≥32GB. Each of these segments serves distinct purposes and caters to various device requirements. The ≤1GB segment is typically used in basic devices where minimal memory is sufficient, such as entry-level smartphones or simple IoT devices. These chips are cost-effective and provide just enough power to handle basic tasks without unnecessary energy consumption. Moving up, the 2GB-8GB range is more common in mid-range smartphones and tablets, where users demand better performance for multitasking and running more complex applications. This segment strikes a balance between cost and performance, making it a popular choice for many consumer electronics. The 16GB segment is often found in high-end smartphones, tablets, and some laptops, where users require substantial memory for gaming, video editing, and other intensive applications. These chips offer enhanced performance and speed, catering to power users who need their devices to handle demanding tasks efficiently. Finally, the ≥32GB segment represents the high-performance end of the spectrum, used in premium devices and specialized applications such as gaming consoles, advanced computing systems, and professional-grade equipment. These chips provide exceptional speed and capacity, supporting the most demanding applications with ease. As technology continues to evolve, the demand for higher memory capacities is expected to grow, pushing the boundaries of what LPDDR chips can achieve in terms of performance and efficiency.

Smartphones, Tablets, Smart Wear, Automotive, Others in the LPDDR Chips - Global Market:

LPDDR chips are integral to various applications, including smartphones, tablets, smart wear, automotive, and other sectors. In smartphones, these chips are essential for managing power consumption while delivering high performance, enabling devices to run multiple applications smoothly without draining the battery quickly. This is particularly important as smartphones become more sophisticated, with users expecting seamless multitasking and high-speed processing. In tablets, LPDDR chips provide the necessary power efficiency and performance to support larger screens and more demanding applications, such as video streaming and gaming. The ability to maintain long battery life while delivering high-quality performance is a key selling point for tablets, making LPDDR chips a crucial component. In the realm of smart wear, such as smartwatches and fitness trackers, LPDDR chips help extend battery life while supporting the various sensors and connectivity features these devices offer. The compact size and low power consumption of these chips make them ideal for wearable technology, where space and energy efficiency are at a premium. In the automotive industry, LPDDR chips are used in infotainment systems, advanced driver-assistance systems (ADAS), and other electronic components that require reliable performance without excessive power draw. As vehicles become more connected and autonomous, the demand for efficient memory solutions like LPDDR chips is expected to rise. Beyond these specific applications, LPDDR chips are also used in a variety of other devices and systems, from smart home gadgets to industrial equipment, where energy efficiency and performance are critical. The versatility and efficiency of LPDDR chips make them a valuable asset in the ever-evolving landscape of technology.

LPDDR Chips - Global Market Outlook:

The global market for LPDDR chips was valued at approximately US$ 6,817 million in 2023, with expectations to reach a revised size of US$ 9,650.2 million by 2030, growing at a compound annual growth rate (CAGR) of 6.8% during the forecast period from 2024 to 2030. LPDDR chips, also known as low-power DDR, are a type of dynamic random-access memory (DRAM) optimized for low power consumption. These chips are designed to provide high performance while minimizing energy usage, making them ideal for portable and battery-operated devices. As the demand for energy-efficient technology continues to rise, LPDDR chips are becoming increasingly important in various applications, from smartphones and tablets to automotive systems and smart wearables. The market's growth is driven by the need for devices that can handle complex tasks without rapidly depleting battery life, as well as advancements in technology that enable more efficient memory solutions. As industries continue to prioritize energy efficiency and performance, the LPDDR chips market is poised for significant growth, offering numerous opportunities for innovation and development in the field of memory technology.

| Report Metric | Details |

| Report Name | LPDDR Chips - Market |

| Forecasted market size in 2030 | US$ 9650.2 million |

| CAGR | 6.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Samsung, SK Hynix, Micron Technology, Nanya Technology, Winbond, Integrated Silicon Solution Inc. (ISSI), Alliance Memory, Etron Technology, AP Memory, ChangXin Memory Technologies (CXMT), Longsys, BIWIN Storage Technology, Dosilicon |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |