What is Direct Fired Radiant-Convection Heater - Global Market?

Direct Fired Radiant-Convection Heaters are specialized heating devices that combine the principles of radiant and convection heating to provide efficient and effective temperature control in various industrial settings. These heaters operate by directly burning fuel to produce heat, which is then transferred to the surrounding environment through both radiation and convection processes. The radiant component of the heater emits infrared energy, which directly warms objects and surfaces in its path, while the convection component circulates warm air throughout the space. This dual-action heating method ensures a more uniform temperature distribution, making it ideal for large or open areas where consistent heating is required. The global market for these heaters is driven by their versatility and efficiency, as they can be used in a wide range of applications, from industrial manufacturing to construction sites. Their ability to provide rapid and targeted heating makes them a valuable asset in environments where maintaining specific temperature conditions is crucial. As industries continue to seek energy-efficient and cost-effective heating solutions, the demand for Direct Fired Radiant-Convection Heaters is expected to grow, reflecting their importance in modern industrial processes.

Single Stage, Two Stage in the Direct Fired Radiant-Convection Heater - Global Market:

Direct Fired Radiant-Convection Heaters are available in different configurations, primarily categorized into single-stage and two-stage models, each offering distinct advantages depending on the application requirements. Single-stage heaters operate at a fixed output level, providing a consistent and steady heat source. They are typically used in environments where a constant temperature is necessary, and the heating demand does not fluctuate significantly. These heaters are straightforward in design, making them reliable and easy to maintain, which is particularly beneficial in industrial settings where downtime can be costly. On the other hand, two-stage heaters offer more flexibility by allowing the user to adjust the heat output between two levels. This capability is particularly advantageous in environments where the heating demand varies, such as in facilities with fluctuating occupancy levels or changing production schedules. By operating at a lower output when full capacity is not needed, two-stage heaters can improve energy efficiency and reduce operational costs. The choice between single-stage and two-stage heaters often depends on the specific heating requirements of the application, as well as considerations such as energy efficiency, cost, and ease of use. In the global market, the demand for these heaters is influenced by factors such as industrial growth, energy prices, and environmental regulations. As industries continue to prioritize energy efficiency and sustainability, the adoption of two-stage heaters is expected to increase, given their ability to optimize energy use and reduce emissions. However, single-stage heaters remain a popular choice in applications where simplicity and reliability are paramount. The global market for Direct Fired Radiant-Convection Heaters is characterized by a diverse range of applications, from large-scale industrial facilities to smaller commercial spaces. In industrial settings, these heaters are often used to maintain optimal working conditions, ensuring that processes are carried out efficiently and safely. In commercial spaces, they provide a comfortable environment for occupants, enhancing productivity and well-being. The versatility of these heaters makes them suitable for a wide range of industries, including manufacturing, warehousing, and logistics. As the global market continues to evolve, manufacturers are focusing on developing innovative solutions that meet the changing needs of their customers. This includes the integration of advanced technologies, such as smart controls and remote monitoring, which enhance the performance and efficiency of these heaters. By leveraging these technologies, users can achieve greater control over their heating systems, optimizing energy use and reducing costs. Overall, the global market for Direct Fired Radiant-Convection Heaters is poised for growth, driven by the increasing demand for efficient and reliable heating solutions across various industries.

Petrochemical, Mining, Construction, Others in the Direct Fired Radiant-Convection Heater - Global Market:

Direct Fired Radiant-Convection Heaters play a crucial role in several key industries, including petrochemical, mining, construction, and others, by providing efficient and reliable heating solutions tailored to the specific needs of each sector. In the petrochemical industry, these heaters are essential for maintaining the precise temperature conditions required for various chemical processes. The ability to deliver consistent and uniform heat is vital in ensuring the quality and safety of petrochemical products. Additionally, the robust design of these heaters allows them to withstand the harsh environments often encountered in petrochemical facilities, such as exposure to corrosive substances and extreme temperatures. In the mining industry, Direct Fired Radiant-Convection Heaters are used to provide warmth in underground mines and other remote locations where traditional heating methods may be impractical. The portability and efficiency of these heaters make them ideal for use in challenging environments, where maintaining a comfortable temperature is crucial for the safety and productivity of workers. In the construction industry, these heaters are commonly used to provide temporary heating on job sites, ensuring that construction activities can continue even in cold weather conditions. Their ability to deliver rapid and targeted heat makes them an invaluable tool for tasks such as curing concrete, drying paint, and thawing frozen ground. Beyond these industries, Direct Fired Radiant-Convection Heaters are also used in a variety of other applications, including agriculture, where they provide warmth for livestock and greenhouses, and in the transportation sector, where they are used to heat large vehicles and equipment. The versatility and efficiency of these heaters make them a popular choice across a wide range of industries, as they offer a cost-effective solution for maintaining optimal temperature conditions in diverse environments. As industries continue to seek innovative and sustainable heating solutions, the demand for Direct Fired Radiant-Convection Heaters is expected to grow, reflecting their importance in modern industrial processes.

Direct Fired Radiant-Convection Heater - Global Market Outlook:

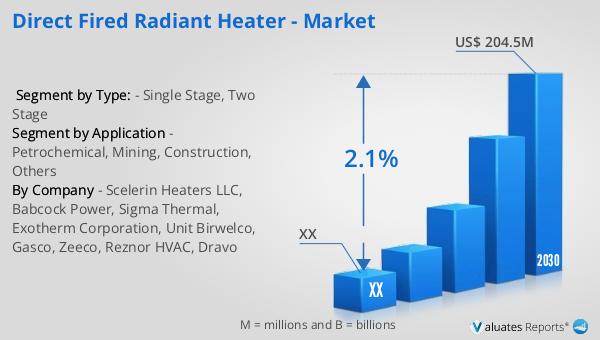

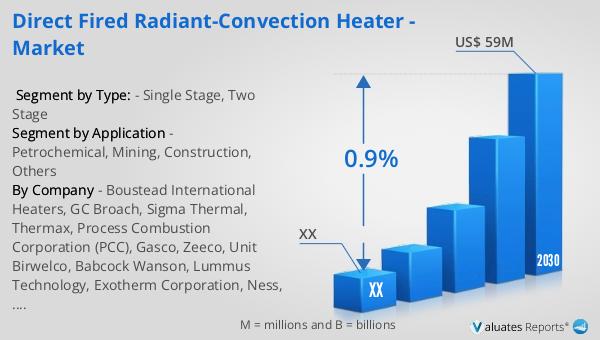

The global market for Direct Fired Radiant-Convection Heaters was valued at approximately $56 million in 2023. It is projected to reach a revised size of $59 million by 2030, growing at a compound annual growth rate (CAGR) of 0.9% during the forecast period from 2024 to 2030. This modest growth reflects the steady demand for these heaters across various industries, driven by their efficiency and versatility. In the construction machinery sector, sales in Europe saw a significant increase of 24% in 2021, highlighting the region's robust demand for construction equipment. By 2022, the revenue from construction machinery in Europe was around $22 billion, while the U.S. market recorded sales of approximately $36 billion in the same year. These figures underscore the importance of efficient heating solutions in supporting the construction industry's growth and development. As the global market for Direct Fired Radiant-Convection Heaters continues to evolve, manufacturers are focusing on developing innovative solutions that meet the changing needs of their customers, ensuring that these heaters remain a vital component of modern industrial processes.

| Report Metric |

Details |

| Report Name |

Direct Fired Radiant-Convection Heater - Market |

| Forecasted market size in 2030 |

US$ 59 million |

| CAGR |

0.9% |

| Forecasted years |

2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

- Petrochemical

- Mining

- Construction

- Others

|

| By Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia) Rest of Europe

- Nordic Countries

- Asia-Pacific (China, Japan, South Korea)

- Southeast Asia (India, Australia)

- Rest of Asia

- Latin America (Mexico, Brazil)

- Rest of Latin America

- Middle East & Africa (Turkey, Saudi Arabia, UAE, Rest of MEA)

|

| By Company |

Boustead International Heaters, GC Broach, Sigma Thermal, Thermax, Process Combustion Corporation (PCC), Gasco, Zeeco, Unit Birwelco, Babcock Wanson, Lummus Technology, Exotherm Corporation, Ness, Scelerin Heaters, Babcock Power |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |