What is Wafer Hybrid Bonding Equipment - Global Market?

Wafer hybrid bonding equipment is a crucial component in the semiconductor manufacturing industry, playing a significant role in the production of advanced electronic devices. This equipment is used to bond wafers, which are thin slices of semiconductor material, typically silicon, that serve as the substrate for microelectronic devices. The hybrid bonding process involves the use of both adhesive and metallic bonding techniques to create a strong and reliable connection between wafers. This method is particularly important for the development of 3D integrated circuits, which require precise alignment and bonding of multiple layers of wafers. The global market for wafer hybrid bonding equipment is driven by the increasing demand for high-performance electronic devices, such as smartphones, tablets, and other consumer electronics. As technology continues to advance, the need for more efficient and compact semiconductor devices grows, further fueling the demand for wafer hybrid bonding equipment. Manufacturers in this market are constantly innovating to improve the precision, speed, and reliability of their equipment, ensuring they meet the evolving needs of the semiconductor industry. The market is characterized by a high level of competition, with numerous players striving to gain a competitive edge through technological advancements and strategic partnerships.

Fully Automatic, Semi-automatic in the Wafer Hybrid Bonding Equipment - Global Market:

In the global market for wafer hybrid bonding equipment, there are two primary types of systems: fully automatic and semi-automatic. Fully automatic wafer hybrid bonding equipment is designed to perform the bonding process with minimal human intervention. These systems are equipped with advanced robotics and automation technologies that allow for precise alignment and bonding of wafers. The fully automatic systems are ideal for high-volume production environments where efficiency and speed are critical. They offer significant advantages in terms of throughput and consistency, as they can operate continuously with minimal downtime. The automation also reduces the risk of human error, ensuring a higher yield of defect-free products. On the other hand, semi-automatic wafer hybrid bonding equipment requires some level of human involvement in the bonding process. These systems are typically used in smaller production environments or for specialized applications where flexibility and customization are more important than speed. Semi-automatic systems offer greater control over the bonding process, allowing operators to make adjustments as needed to achieve the desired results. While they may not match the throughput of fully automatic systems, they provide a cost-effective solution for manufacturers with lower production volumes or those working with complex or delicate materials. Both fully automatic and semi-automatic systems have their place in the global market for wafer hybrid bonding equipment, catering to different needs and preferences of manufacturers. The choice between the two often depends on factors such as production volume, budget, and the specific requirements of the application. As the semiconductor industry continues to evolve, manufacturers are increasingly looking for equipment that offers a balance between automation and flexibility. This has led to the development of hybrid systems that combine elements of both fully automatic and semi-automatic equipment, providing manufacturers with the best of both worlds. These hybrid systems offer the precision and efficiency of fully automatic systems, along with the adaptability and control of semi-automatic systems. They are particularly well-suited for applications that require a high degree of customization or involve complex bonding processes. The global market for wafer hybrid bonding equipment is expected to continue growing as manufacturers seek out new technologies and solutions to meet the demands of the ever-changing semiconductor industry. With the increasing complexity of electronic devices and the push for smaller, more efficient components, the need for advanced bonding equipment will only continue to rise. Manufacturers that can offer innovative, reliable, and cost-effective solutions will be well-positioned to succeed in this competitive market.

200 mm Wafer, 300 mm Wafer in the Wafer Hybrid Bonding Equipment - Global Market:

Wafer hybrid bonding equipment is utilized in the semiconductor industry for bonding wafers of different sizes, including 200 mm and 300 mm wafers. The 200 mm wafer, also known as an 8-inch wafer, is commonly used in the production of various semiconductor devices. These wafers are often employed in the manufacturing of microcontrollers, sensors, and other components used in automotive, industrial, and consumer electronics applications. The use of wafer hybrid bonding equipment in the production of 200 mm wafers allows for the creation of more complex and efficient devices, as it enables the stacking of multiple layers of circuitry. This results in improved performance and functionality of the final product. The 300 mm wafer, or 12-inch wafer, is the standard size for high-volume semiconductor manufacturing. These larger wafers are used in the production of advanced microprocessors, memory chips, and other high-performance electronic components. The use of wafer hybrid bonding equipment in the production of 300 mm wafers is essential for achieving the precision and reliability required for these cutting-edge devices. The larger size of the 300 mm wafer allows for the production of more chips per wafer, resulting in increased efficiency and cost-effectiveness for manufacturers. The global market for wafer hybrid bonding equipment is driven by the growing demand for both 200 mm and 300 mm wafers, as manufacturers seek to meet the needs of various industries and applications. The use of wafer hybrid bonding equipment in the production of these wafers enables manufacturers to create more advanced and efficient devices, which are essential for the development of new technologies and products. As the semiconductor industry continues to evolve, the demand for wafer hybrid bonding equipment is expected to grow, as manufacturers look for ways to improve the performance and functionality of their products. The ability to bond wafers of different sizes and materials is a key advantage of wafer hybrid bonding equipment, as it allows manufacturers to create customized solutions for their specific needs. This flexibility is particularly important in the rapidly changing semiconductor industry, where new technologies and applications are constantly emerging. By investing in wafer hybrid bonding equipment, manufacturers can stay ahead of the competition and continue to innovate in the development of new products and technologies.

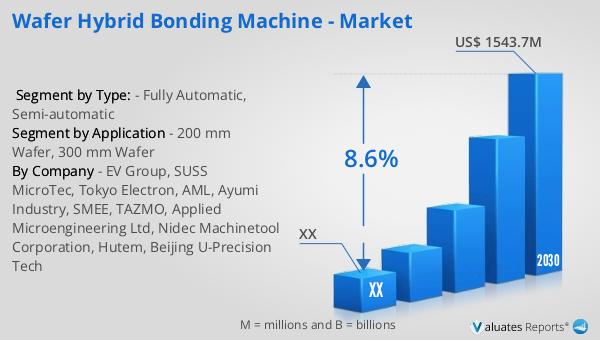

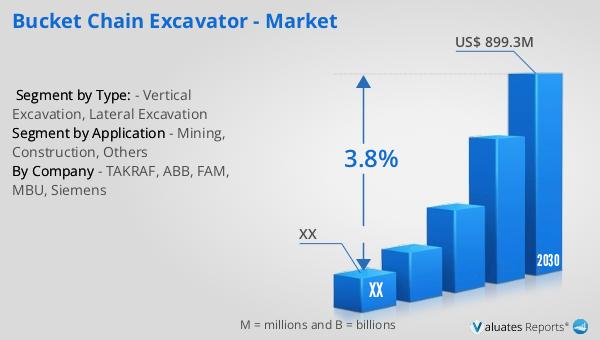

Wafer Hybrid Bonding Equipment - Global Market Outlook:

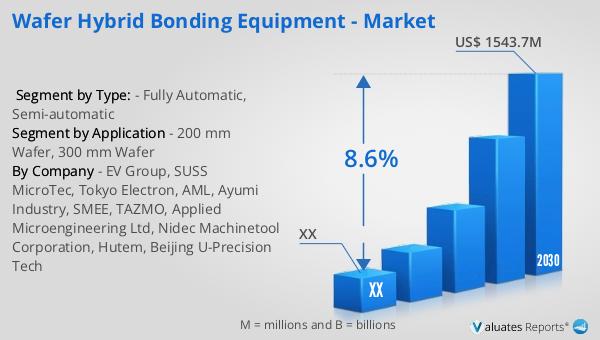

In 2023, the global market for wafer hybrid bonding equipment was valued at approximately $886 million. This market is projected to grow significantly, reaching an estimated size of $1,543.7 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 8.6% during the forecast period from 2024 to 2030. The market's expansion is driven by the increasing demand for advanced semiconductor devices and the need for more efficient and reliable bonding solutions. North America, Europe, and Japan collectively hold a market share of 23%, indicating their significant influence and contribution to the global market. These regions are home to some of the leading manufacturers and technology developers in the semiconductor industry, which drives innovation and growth in the wafer hybrid bonding equipment market. As the demand for high-performance electronic devices continues to rise, manufacturers in these regions are investing in advanced bonding technologies to meet the evolving needs of the industry. The market outlook for wafer hybrid bonding equipment is positive, with continued growth expected as manufacturers seek to improve the performance and efficiency of their products. The increasing complexity of electronic devices and the push for smaller, more efficient components are key factors driving the demand for advanced bonding equipment. As a result, manufacturers that can offer innovative, reliable, and cost-effective solutions will be well-positioned to succeed in this competitive market. The global market for wafer hybrid bonding equipment is poised for significant growth, driven by the ongoing advancements in semiconductor technology and the increasing demand for high-performance electronic devices.

| Report Metric | Details |

| Report Name | Wafer Hybrid Bonding Equipment - Market |

| Forecasted market size in 2030 | US$ 1543.7 million |

| CAGR | 8.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | EV Group, SUSS MicroTec, Tokyo Electron, AML, Ayumi Industry, SMEE, TAZMO, Applied Microengineering Ltd, Nidec Machinetool Corporation, Hutem, Beijing U-Precision Tech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |