What is Interlocking Oilfield Mat - Global Market?

Interlocking oilfield mats are specialized platforms used in the oil and gas industry to provide stable surfaces for heavy equipment and vehicles. These mats are designed to interlock, creating a continuous and secure surface that can withstand the harsh conditions of oilfield environments. The global market for interlocking oilfield mats is driven by the increasing demand for oil and gas exploration and production activities. As these activities often take place in remote and environmentally sensitive areas, there is a growing need for durable and reliable matting solutions that can minimize environmental impact while ensuring operational efficiency. Interlocking oilfield mats are typically made from materials such as wood, metal, or composite materials, each offering unique benefits in terms of strength, durability, and cost-effectiveness. The market is characterized by a diverse range of products catering to different needs and preferences, with manufacturers continuously innovating to improve the performance and sustainability of their offerings. As the oil and gas industry continues to expand, the demand for interlocking oilfield mats is expected to grow, driven by the need for safe and efficient operations in challenging environments.

Composite Mats, Wood & Metal Mats in the Interlocking Oilfield Mat - Global Market:

Composite mats, wood mats, and metal mats are the primary types of interlocking oilfield mats available in the global market, each offering distinct advantages and applications. Composite mats are made from high-density polyethylene or other synthetic materials, providing a lightweight yet robust solution for oilfield operations. These mats are resistant to chemicals, water, and extreme temperatures, making them ideal for use in harsh environments. Their interlocking design ensures a secure fit, reducing the risk of slippage or displacement during use. Composite mats are also environmentally friendly, as they can be recycled and reused multiple times, reducing waste and lowering overall costs. Wood mats, on the other hand, are typically made from hardwoods such as oak or pine, offering a natural and cost-effective solution for temporary roadways and working platforms. These mats are known for their strength and durability, capable of supporting heavy loads and withstanding the rigors of oilfield operations. However, wood mats are susceptible to water damage and decay, requiring regular maintenance and replacement. Metal mats, often made from steel or aluminum, provide the highest level of strength and durability among the three types. These mats are designed to withstand extreme loads and harsh conditions, making them suitable for use in the most demanding oilfield environments. Metal mats are also resistant to corrosion and wear, ensuring a long service life and reducing the need for frequent replacements. However, they are heavier and more expensive than composite or wood mats, which can be a consideration for some operators. Despite these differences, all three types of interlocking oilfield mats share the common goal of providing a stable and reliable surface for oilfield operations, enhancing safety and efficiency while minimizing environmental impact. As the global market for interlocking oilfield mats continues to grow, manufacturers are focusing on developing new materials and designs to meet the evolving needs of the industry, ensuring that operators have access to the best possible solutions for their specific requirements.

Temporary Roadways, Working Platforms in the Interlocking Oilfield Mat - Global Market:

Interlocking oilfield mats play a crucial role in the construction of temporary roadways and working platforms, providing a stable and secure surface for vehicles and equipment in challenging environments. Temporary roadways are essential in oilfield operations, as they enable the safe and efficient transportation of heavy machinery, personnel, and materials to and from remote sites. Interlocking mats are used to create these roadways, offering a durable and reliable solution that can withstand the weight and movement of heavy vehicles. The interlocking design ensures that the mats remain securely in place, reducing the risk of accidents or damage to the underlying terrain. In addition to temporary roadways, interlocking oilfield mats are also used to construct working platforms, providing a stable base for drilling rigs, cranes, and other equipment. These platforms are essential for ensuring the safety and efficiency of oilfield operations, as they prevent equipment from sinking or becoming unstable on soft or uneven ground. The use of interlocking mats in working platforms also helps to minimize environmental impact, as they distribute the weight of the equipment evenly across the surface, reducing soil compaction and damage to vegetation. Furthermore, interlocking mats can be easily installed and removed, allowing for quick and efficient setup and teardown of temporary roadways and working platforms. This flexibility is particularly important in the oil and gas industry, where operations often need to be relocated or adjusted in response to changing conditions. Overall, the use of interlocking oilfield mats in temporary roadways and working platforms is a critical component of modern oilfield operations, enhancing safety, efficiency, and environmental sustainability. As the demand for oil and gas continues to grow, the need for reliable and effective matting solutions is expected to increase, driving further innovation and development in the global market for interlocking oilfield mats.

Interlocking Oilfield Mat - Global Market Outlook:

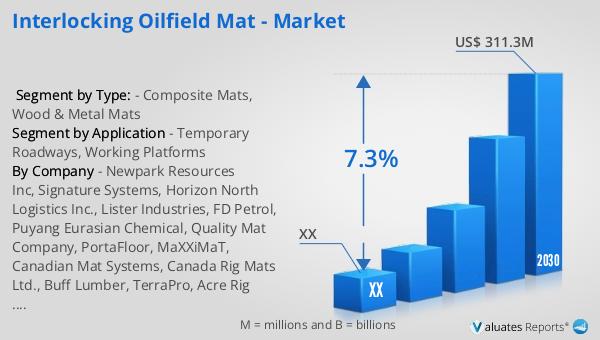

The global market for interlocking oilfield mats was valued at approximately $191 million in 2023, with projections indicating a growth to around $311.3 million by 2030. This represents a compound annual growth rate (CAGR) of 7.3% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for oil and gas exploration and production activities, which require durable and reliable matting solutions to ensure safe and efficient operations. In North America, the market for interlocking oilfield mats is also expected to experience significant growth, although specific figures for this region were not provided. The increasing focus on environmental sustainability and the need to minimize the impact of oilfield operations on sensitive ecosystems are key factors contributing to the growth of the market. Manufacturers are continuously innovating to develop new materials and designs that offer improved performance and sustainability, ensuring that operators have access to the best possible solutions for their specific needs. As the global market for interlocking oilfield mats continues to expand, it is expected to play an increasingly important role in supporting the growth and development of the oil and gas industry, providing the necessary infrastructure for safe and efficient operations in challenging environments.

| Report Metric | Details |

| Report Name | Interlocking Oilfield Mat - Market |

| Forecasted market size in 2030 | US$ 311.3 million |

| CAGR | 7.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Newpark Resources Inc, Signature Systems, Horizon North Logistics Inc., Lister Industries, FD Petrol, Puyang Eurasian Chemical, Quality Mat Company, PortaFloor, MaXXiMaT, Canadian Mat Systems, Canada Rig Mats Ltd., Buff Lumber, TerraPro, Acre Rig Mats, Rig Mats of America, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |