What is Silicon Carbide (SiC) Shell and Tube Heat Exchanger - Global Market?

Silicon Carbide (SiC) Shell and Tube Heat Exchangers are specialized devices used in various industries to transfer heat between two or more fluids. These heat exchangers are constructed using silicon carbide, a material known for its exceptional thermal conductivity, high strength, and resistance to corrosion and thermal shock. The global market for these heat exchangers is expanding due to their ability to operate efficiently under extreme conditions, making them ideal for industries that require robust and reliable heat transfer solutions. The demand for SiC shell and tube heat exchangers is driven by their application in sectors such as chemical processing, power generation, and metal treatment, where they help in optimizing energy use and improving process efficiency. As industries continue to seek sustainable and cost-effective solutions, the adoption of silicon carbide heat exchangers is expected to grow, supported by advancements in manufacturing technologies and increasing awareness of their benefits. The market is characterized by a diverse range of products tailored to meet specific industrial needs, with manufacturers focusing on innovation to enhance performance and durability.

15 Sqm and Below 15 Sqm, Above 15 Sqm in the Silicon Carbide (SiC) Shell and Tube Heat Exchanger - Global Market:

In the global market for Silicon Carbide (SiC) Shell and Tube Heat Exchangers, the size of the heat exchanger plays a crucial role in determining its application and efficiency. Heat exchangers with a surface area of 15 square meters (sqm) and below are typically used in smaller-scale operations or where space is limited. These compact units are favored in industries where precise temperature control is essential, and they offer the advantage of being easier to install and maintain. On the other hand, heat exchangers with a surface area above 15 sqm are designed for larger industrial applications. These units are capable of handling higher volumes of fluid and are often used in processes that require significant heat transfer capabilities, such as in large chemical plants or power stations. The choice between these two categories depends on the specific requirements of the application, including the volume of fluid to be processed, the temperature range, and the available space for installation. As the global market for SiC shell and tube heat exchangers continues to grow, manufacturers are focusing on developing products that cater to both ends of the spectrum, ensuring that they can meet the diverse needs of their customers. This involves not only optimizing the design and materials used in these heat exchangers but also providing customized solutions that can be tailored to specific industrial processes. The versatility of silicon carbide as a material allows for a wide range of applications, making these heat exchangers a valuable asset in industries that demand high performance and reliability. As industries continue to evolve and seek more efficient ways to manage heat transfer, the demand for both small and large SiC shell and tube heat exchangers is expected to increase, driven by the need for sustainable and cost-effective solutions.

Chemical Industry, Metal Pickling, Others in the Silicon Carbide (SiC) Shell and Tube Heat Exchanger - Global Market:

Silicon Carbide (SiC) Shell and Tube Heat Exchangers are extensively used in various industries due to their superior thermal properties and durability. In the chemical industry, these heat exchangers are crucial for processes that involve corrosive substances and high temperatures. They are used in the production of chemicals, where precise temperature control is essential to ensure product quality and process efficiency. The ability of SiC heat exchangers to withstand harsh chemical environments makes them ideal for applications such as acid production, where traditional materials might fail. In metal pickling, SiC shell and tube heat exchangers play a vital role in maintaining the temperature of pickling solutions, which are used to remove impurities from metal surfaces. The high thermal conductivity of silicon carbide ensures that the heat exchangers can efficiently transfer heat, reducing energy consumption and improving the overall efficiency of the pickling process. Additionally, the resistance of SiC to corrosion and thermal shock ensures that these heat exchangers have a long service life, even in the demanding conditions of metal pickling. Beyond these specific industries, SiC shell and tube heat exchangers are also used in a variety of other applications where reliable heat transfer is required. This includes sectors such as power generation, where they are used to improve the efficiency of energy conversion processes, and in the food and beverage industry, where they help maintain the quality and safety of products by ensuring precise temperature control. The versatility and robustness of silicon carbide make these heat exchangers a preferred choice for industries that require high-performance solutions for heat management. As the global market for SiC shell and tube heat exchangers continues to expand, their usage in these and other areas is expected to grow, driven by the need for efficient and sustainable heat transfer solutions.

Silicon Carbide (SiC) Shell and Tube Heat Exchanger - Global Market Outlook:

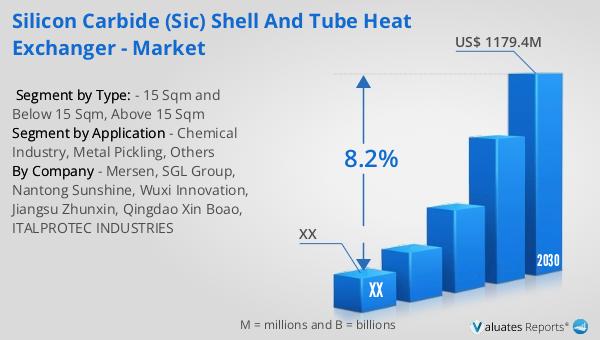

The global market for Silicon Carbide (SiC) Shell and Tube Heat Exchangers was valued at approximately $688 million in 2023. It is projected to grow significantly, reaching an estimated size of $1,179.4 million by 2030, with a compound annual growth rate (CAGR) of 8.2% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for efficient and durable heat transfer solutions across various industries. In North America, the market for SiC shell and tube heat exchangers is also expected to expand, although specific figures for this region were not provided. The anticipated growth in this market is driven by the need for advanced materials that can withstand extreme conditions and improve process efficiency. As industries continue to prioritize sustainability and cost-effectiveness, the adoption of silicon carbide heat exchangers is likely to increase, supported by ongoing technological advancements and a growing awareness of their benefits. The market outlook suggests a positive trajectory for SiC shell and tube heat exchangers, highlighting their importance in meeting the evolving needs of industries worldwide.

| Report Metric | Details |

| Report Name | Silicon Carbide (SiC) Shell and Tube Heat Exchanger - Market |

| Forecasted market size in 2030 | US$ 1179.4 million |

| CAGR | 8.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Mersen, SGL Group, Nantong Sunshine, Wuxi Innovation, Jiangsu Zhunxin, Qingdao Xin Boao, ITALPROTEC INDUSTRIES |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |