What is High Frequency Chip Resistors - Global Market?

High Frequency Chip Resistors are essential components in the electronics industry, designed to handle high-frequency signals with precision and reliability. These resistors are crucial in applications where signal integrity and performance are paramount, such as in telecommunications, aerospace, and advanced computing systems. The global market for High Frequency Chip Resistors is driven by the increasing demand for miniaturized electronic devices and the need for components that can operate efficiently at high frequencies. As technology advances, the need for these resistors continues to grow, with manufacturers focusing on improving their performance, reliability, and cost-effectiveness. The market is characterized by a diverse range of products, each tailored to specific applications and frequency ranges, ensuring that designers and engineers have the right tools to meet their needs. With ongoing research and development, the capabilities of High Frequency Chip Resistors are expected to expand, further solidifying their role in the global electronics landscape.

Metal Film Resistors, Thin Film Chip Resistors, Thick Film Chip Resistors, Others in the High Frequency Chip Resistors - Global Market:

Metal Film Resistors, Thin Film Chip Resistors, and Thick Film Chip Resistors are all integral components within the High Frequency Chip Resistors market, each offering unique characteristics and advantages. Metal Film Resistors are known for their precision and stability, making them ideal for applications requiring high accuracy and low noise. They are constructed by depositing a thin layer of metal onto a ceramic substrate, which allows for tight tolerance and excellent temperature coefficient performance. Thin Film Chip Resistors, on the other hand, are made by depositing a thin resistive film onto an insulating substrate. These resistors are prized for their high precision, low noise, and excellent stability over a wide range of temperatures. They are commonly used in precision applications where performance is critical, such as in medical devices and high-end audio equipment. Thick Film Chip Resistors are manufactured by applying a thick layer of resistive material onto a ceramic base. They are generally more cost-effective than their thin film counterparts and are used in applications where precision is less critical but reliability and durability are still important. These resistors are often found in consumer electronics, automotive applications, and industrial equipment. Each type of resistor plays a vital role in the High Frequency Chip Resistors market, catering to different needs and applications. The choice between metal film, thin film, and thick film resistors depends on factors such as cost, performance requirements, and environmental conditions. As technology continues to evolve, manufacturers are constantly innovating to improve the performance and reliability of these resistors, ensuring they meet the ever-changing demands of the global market. Other types of resistors in this market include wirewound and carbon composition resistors, each with their own set of characteristics and applications. Wirewound resistors are known for their high power handling capabilities and are often used in power supplies and motor control applications. Carbon composition resistors, while less common today, are still used in certain applications where their unique properties are advantageous. Overall, the High Frequency Chip Resistors market is diverse and dynamic, with a wide range of products available to meet the needs of various industries and applications.

Industrial Applications, Aerospace, Medical Industry, Others in the High Frequency Chip Resistors - Global Market:

High Frequency Chip Resistors find extensive usage across various sectors, including industrial applications, aerospace, and the medical industry, among others. In industrial applications, these resistors are crucial for ensuring the reliability and efficiency of electronic systems used in manufacturing, automation, and process control. They help maintain signal integrity and reduce electromagnetic interference, which is vital for the smooth operation of complex machinery and equipment. In the aerospace sector, High Frequency Chip Resistors are used in avionics, communication systems, and radar equipment, where precision and reliability are of utmost importance. These resistors must withstand harsh environmental conditions, including extreme temperatures and vibrations, while maintaining their performance. The medical industry also relies heavily on High Frequency Chip Resistors for various applications, such as in diagnostic equipment, imaging systems, and patient monitoring devices. These resistors ensure accurate signal processing and data transmission, which are critical for patient safety and effective diagnosis. Other sectors that benefit from High Frequency Chip Resistors include telecommunications, automotive, and consumer electronics. In telecommunications, these resistors are used in network infrastructure and mobile devices to ensure high-speed data transmission and connectivity. In the automotive industry, they are used in advanced driver-assistance systems (ADAS), infotainment systems, and electric vehicles, where they contribute to the overall performance and safety of the vehicle. In consumer electronics, High Frequency Chip Resistors are found in smartphones, tablets, and wearable devices, where they help optimize performance and battery life. Overall, the versatility and reliability of High Frequency Chip Resistors make them indispensable in a wide range of applications, driving their demand in the global market.

High Frequency Chip Resistors - Global Market Outlook:

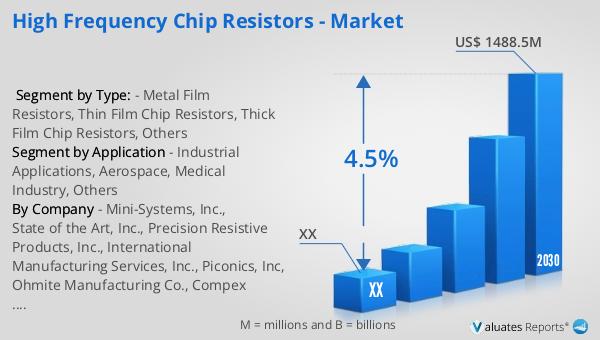

The global market for High Frequency Chip Resistors was valued at approximately $1,089 million in 2023, with projections indicating a growth to around $1,488.5 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030. The North American segment of this market was also valued in 2023, with expectations of reaching a higher value by 2030, although specific figures for this region were not provided. The anticipated growth in the High Frequency Chip Resistors market is driven by the increasing demand for advanced electronic devices and systems that require high precision and reliability. As industries such as telecommunications, aerospace, and medical technology continue to expand and innovate, the need for components that can handle high-frequency signals with accuracy and stability becomes more critical. This market outlook reflects the ongoing advancements in technology and the growing importance of High Frequency Chip Resistors in various applications worldwide. The projected growth underscores the significance of these components in the global electronics industry and highlights the opportunities for manufacturers and suppliers to capitalize on this expanding market.

| Report Metric | Details |

| Report Name | High Frequency Chip Resistors - Market |

| Forecasted market size in 2030 | US$ 1488.5 million |

| CAGR | 4.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Mini-Systems, Inc., State of the Art, Inc., Precision Resistive Products, Inc., International Manufacturing Services, Inc., Piconics, Inc, Ohmite Manufacturing Co., Compex Corp., Vishay, Post Glover Resistors, Altronic Research, Inc., SV Microwave Inc., UPE, Inc., Caddock Electronics, Inc., M-Tron Components, Inc., Cal-Chip Electronics, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |