What is Artificial Crown - Global Market?

Artificial crowns are dental restorations used to cover or "cap" a damaged tooth, restoring its shape, size, strength, and appearance. The global market for artificial crowns is a significant segment within the broader dental industry, driven by increasing awareness of oral health, advancements in dental technology, and a growing aging population that requires dental care. These crowns are typically made from materials such as metal, ceramics, or resin, each offering unique benefits and applications. The demand for artificial crowns is also fueled by the rising prevalence of dental diseases, increased dental tourism, and the growing acceptance of cosmetic dentistry. As more people seek to improve their dental aesthetics and functionality, the market for artificial crowns continues to expand. Additionally, the integration of digital dentistry, such as CAD/CAM technology, has streamlined the production process, making crowns more accessible and affordable for patients worldwide. This market is poised for growth as dental professionals and patients alike recognize the importance of maintaining oral health and the role that artificial crowns play in achieving this goal.

Metal, Ceramics, Resin in the Artificial Crown - Global Market:

Artificial crowns are crafted from various materials, each offering distinct advantages and considerations. Metal crowns, for instance, are known for their durability and strength, making them ideal for molars that endure significant chewing pressure. These crowns are often made from alloys containing gold, palladium, or base-metal alloys like nickel or chromium. While metal crowns are less likely to chip or break, their metallic color makes them less suitable for visible front teeth. On the other hand, ceramic crowns are prized for their natural appearance, as they can be color-matched to the surrounding teeth. Made from porcelain or other ceramic materials, these crowns are an excellent choice for front teeth and are often preferred by patients seeking a more aesthetic solution. However, ceramic crowns may not be as durable as metal crowns and can be more prone to chipping. Resin crowns, meanwhile, are typically less expensive than other types and can be a good option for temporary restorations. They are made from composite materials that can be easily shaped and colored to match natural teeth. However, resin crowns are not as strong or long-lasting as metal or ceramic options and may wear down over time. The choice of material for an artificial crown often depends on the specific needs and preferences of the patient, as well as the location of the tooth being restored. Dental professionals must consider factors such as the patient's bite, the visibility of the tooth, and any allergies or sensitivities to materials when recommending a crown type. As the global market for artificial crowns continues to grow, advancements in material science and dental technology are likely to expand the options available to patients, offering improved aesthetics, durability, and biocompatibility.

Hospital, Dental Clinic, Others in the Artificial Crown - Global Market:

Artificial crowns are widely used in various healthcare settings, including hospitals, dental clinics, and other facilities, to restore damaged teeth and improve oral health. In hospitals, artificial crowns are often part of comprehensive dental care provided to patients with complex medical conditions that may affect their oral health. For instance, patients undergoing cancer treatment or those with chronic illnesses may experience dental issues that require the placement of crowns to protect and restore their teeth. Hospitals with specialized dental departments or collaborations with dental professionals can offer these services as part of a holistic approach to patient care. In dental clinics, artificial crowns are a common procedure performed by dentists to address a range of dental problems, from cavities and fractures to cosmetic enhancements. Dental clinics are equipped with the necessary tools and technology to fabricate and place crowns efficiently, often using digital imaging and CAD/CAM systems to ensure precise fit and aesthetics. Patients visiting dental clinics for crown placement benefit from personalized care and the expertise of dental professionals who can tailor treatments to their specific needs. Other settings where artificial crowns are used include private dental practices, community health centers, and mobile dental units that provide care to underserved populations. These facilities play a crucial role in increasing access to dental care and ensuring that individuals from all walks of life can benefit from the restorative and aesthetic advantages of artificial crowns. As the demand for dental services continues to rise, the use of artificial crowns in these various settings is expected to grow, driven by factors such as increased awareness of oral health, advancements in dental technology, and the desire for improved dental aesthetics.

Artificial Crown - Global Market Outlook:

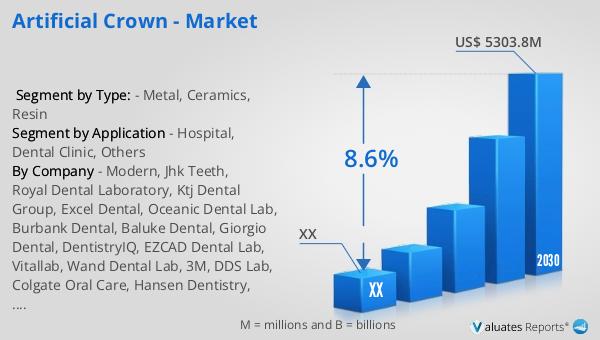

The global market for artificial crowns was valued at approximately US$ 2932 million in 2023, with projections indicating a significant increase to an estimated US$ 5303.8 million by 2030. This growth represents a compound annual growth rate (CAGR) of 8.6% during the forecast period from 2024 to 2030. This upward trend reflects the increasing demand for dental restorations and the growing awareness of oral health worldwide. In comparison, the broader global market for medical devices was estimated at US$ 603 billion in 2023, with a projected CAGR of 5% over the next six years. The artificial crown market's higher growth rate highlights the specific demand for dental solutions and the advancements in dental technology that are driving this segment forward. As more individuals seek to maintain or improve their dental health and aesthetics, the market for artificial crowns is expected to continue its robust growth trajectory, supported by innovations in materials and techniques that enhance the quality and accessibility of dental care.

| Report Metric | Details |

| Report Name | Artificial Crown - Market |

| Forecasted market size in 2030 | US$ 5303.8 million |

| CAGR | 8.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Modern, Jhk Teeth, Royal Dental Laboratory, Ktj Dental Group, Excel Dental, Oceanic Dental Lab, Burbank Dental, Baluke Dental, Giorgio Dental, DentistryIQ, EZCAD Dental Lab, Vitallab, Wand Dental Lab, 3M, DDS Lab, Colgate Oral Care, Hansen Dentistry, Dentsply Sirona, Pymble Medical & Dental Centre, Daniela Dental, Cleveland Clinic, Glidewell Dental, Arcari Dental Lab, Protec Dental |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |