What is Medical UV Disinfection Equipment - Global Market?

Medical UV disinfection equipment is a specialized technology used to eliminate harmful microorganisms, such as bacteria, viruses, and fungi, from various environments. This equipment utilizes ultraviolet (UV) light, specifically UV-C light, which has germicidal properties capable of disrupting the DNA and RNA of microorganisms, rendering them inactive and unable to reproduce. The global market for medical UV disinfection equipment has been expanding due to the increasing awareness of the importance of maintaining sterile environments, especially in healthcare settings. Hospitals, clinics, and laboratories are primary users of this technology, as it helps in reducing the risk of healthcare-associated infections (HAIs). Additionally, the COVID-19 pandemic has further accelerated the demand for effective disinfection solutions, leading to a surge in the adoption of UV disinfection equipment. This market is characterized by continuous innovation, with manufacturers developing more efficient and user-friendly devices to cater to the growing needs of various sectors. The equipment ranges from portable units for small spaces to large-scale systems for comprehensive facility disinfection. As the global emphasis on hygiene and infection control continues to rise, the medical UV disinfection equipment market is poised for significant growth.

High, Medium, Low in the Medical UV Disinfection Equipment - Global Market:

The medical UV disinfection equipment market can be categorized into high, medium, and low segments based on various factors such as intensity, application, and cost. High-intensity UV disinfection equipment is typically used in large healthcare facilities and industrial settings where the need for rapid and thorough disinfection is critical. These systems are designed to deliver a high dose of UV-C light, ensuring the swift elimination of pathogens in high-traffic areas such as operating rooms, intensive care units, and laboratories. The high-intensity equipment is often integrated with advanced features like automated operation, remote monitoring, and data logging, which enhance its efficiency and ease of use. However, these systems tend to be more expensive and require professional installation and maintenance, making them suitable for large-scale operations with substantial budgets. Medium-intensity UV disinfection equipment is commonly used in smaller healthcare facilities, outpatient clinics, and emergency centers. These systems offer a balance between effectiveness and cost, providing adequate disinfection for moderate-sized areas without the need for extensive infrastructure. Medium-intensity equipment is often portable, allowing for flexible use across different locations within a facility. They are designed to be user-friendly, with straightforward controls and minimal maintenance requirements, making them accessible to a wider range of users. This segment of the market is growing as more healthcare providers recognize the benefits of UV disinfection in preventing infections and improving patient safety. Low-intensity UV disinfection equipment is primarily used in household settings and small businesses. These devices are designed for personal use, offering a convenient and affordable solution for maintaining hygiene in everyday environments. Low-intensity equipment includes items like UV sanitizing wands, portable air purifiers, and small UV boxes for disinfecting personal items such as phones, keys, and masks. While these devices may not offer the same level of disinfection as their high-intensity counterparts, they provide an added layer of protection against common germs and viruses. The affordability and ease of use of low-intensity equipment make it an attractive option for consumers looking to enhance their personal hygiene practices. As awareness of the benefits of UV disinfection continues to grow, the demand for low-intensity equipment is expected to increase, particularly in regions with high population density and limited access to healthcare facilities. Overall, the segmentation of the medical UV disinfection equipment market into high, medium, and low categories allows for a diverse range of products that cater to the varying needs and budgets of different users. Each segment plays a crucial role in the broader effort to improve hygiene and reduce the spread of infectious diseases across the globe.

Hospital, Emergency Center, Household in the Medical UV Disinfection Equipment - Global Market:

Medical UV disinfection equipment is utilized in various settings, including hospitals, emergency centers, and households, each with specific needs and applications. In hospitals, UV disinfection equipment is primarily used to maintain sterile environments and prevent healthcare-associated infections (HAIs). Operating rooms, patient wards, and intensive care units are critical areas where UV disinfection is employed to ensure the safety of patients and healthcare workers. The equipment is often used in conjunction with traditional cleaning methods to provide an additional layer of protection against pathogens. Hospitals may use large, high-intensity UV systems that can disinfect entire rooms or smaller, portable units for targeted disinfection of specific areas or equipment. The use of UV disinfection in hospitals has been shown to significantly reduce the incidence of HAIs, leading to improved patient outcomes and reduced healthcare costs. In emergency centers, where the rapid turnover of patients and high-stress environments can increase the risk of infection, UV disinfection equipment plays a vital role in maintaining hygiene. Portable UV devices are commonly used in these settings to quickly disinfect surfaces, medical equipment, and patient transport vehicles. The ability to rapidly deploy UV disinfection technology allows emergency centers to maintain a high standard of cleanliness and reduce the risk of cross-contamination between patients. This is particularly important in situations where patients with infectious diseases are treated, as it helps to prevent the spread of pathogens to other patients and staff. In households, UV disinfection equipment is used to enhance personal hygiene and reduce the risk of infection from everyday germs and viruses. Consumers can choose from a variety of low-intensity UV devices, such as sanitizing wands, air purifiers, and small UV boxes, to disinfect personal items and surfaces. These devices are particularly popular in households with young children, elderly individuals, or immunocompromised family members, as they provide an additional layer of protection against common pathogens. The convenience and affordability of household UV disinfection equipment make it an attractive option for consumers looking to improve their hygiene practices. As awareness of the benefits of UV disinfection continues to grow, the use of these devices in households is expected to increase, contributing to the overall effort to reduce the spread of infectious diseases.

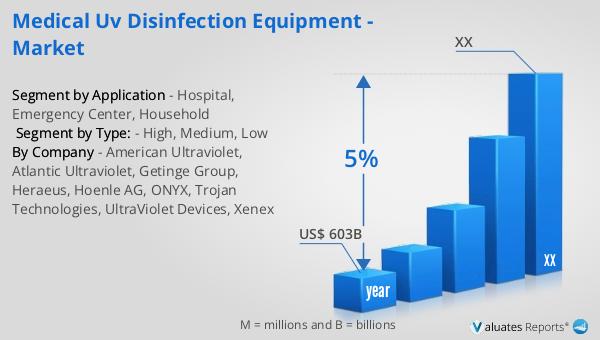

Medical UV Disinfection Equipment - Global Market Outlook:

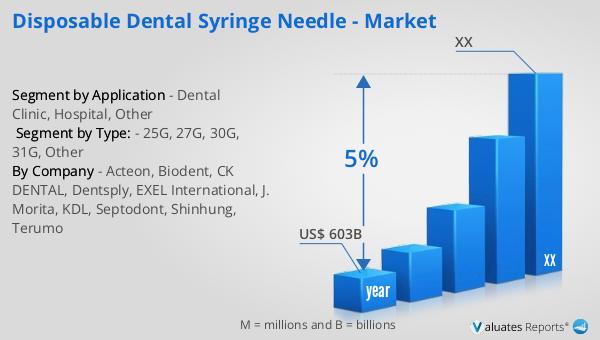

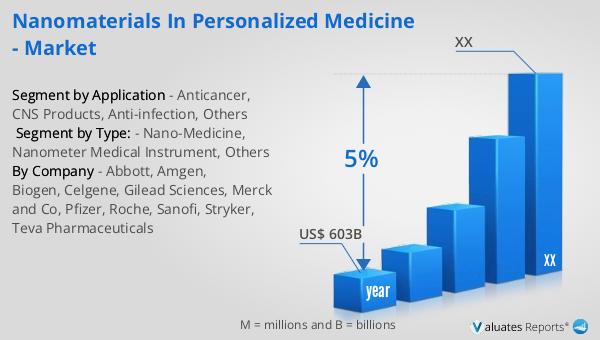

Our research indicates that the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare needs, and a growing emphasis on infection control and hygiene. The medical device industry encompasses a wide range of products, from diagnostic equipment and surgical instruments to advanced disinfection technologies like UV disinfection equipment. As healthcare systems worldwide continue to evolve and adapt to new challenges, the demand for innovative and effective medical devices is expected to rise. The projected growth rate reflects the industry's resilience and ability to meet the changing needs of healthcare providers and patients. Additionally, the increasing focus on patient safety and infection prevention is likely to drive further investment in disinfection technologies, including UV disinfection equipment. This market outlook underscores the importance of continued research and development in the medical device sector to ensure that healthcare providers have access to the tools they need to deliver safe and effective care. As the global population continues to grow and age, the demand for medical devices is expected to remain strong, providing opportunities for companies to innovate and expand their product offerings. The projected growth of the medical device market highlights the critical role that these products play in improving healthcare outcomes and enhancing the quality of life for patients around the world.

| Report Metric | Details |

| Report Name | Medical UV Disinfection Equipment - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | American Ultraviolet, Atlantic Ultraviolet, Getinge Group, Heraeus, Hoenle AG, ONYX, Trojan Technologies, UltraViolet Devices, Xenex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |