What is Denture Disinfectants - Global Market?

Denture disinfectants are specialized products designed to clean and sanitize dentures, ensuring they remain free from harmful bacteria and other microorganisms. These disinfectants are crucial for maintaining oral hygiene for individuals who wear dentures, as they help prevent infections and bad breath. The global market for denture disinfectants has been growing steadily, driven by an increasing awareness of oral health and hygiene, especially among the aging population who are more likely to use dentures. The market includes a variety of products such as tablets, solutions, and wipes, each designed to cater to different user preferences and needs. With advancements in dental care and a growing emphasis on preventive healthcare, the demand for effective denture disinfectants is expected to rise. This market is also influenced by the increasing availability of these products through various distribution channels, including pharmacies and online platforms, making them more accessible to consumers worldwide. As the global population continues to age, the importance of maintaining oral health through products like denture disinfectants is likely to become even more significant.

Powders, Creams, Others in the Denture Disinfectants - Global Market:

In the global market for denture disinfectants, products are typically categorized into powders, creams, and other forms, each offering unique benefits and catering to different consumer preferences. Powders are a popular choice due to their ease of use and effectiveness. They are usually dissolved in water to create a cleaning solution in which dentures can be soaked. This method is highly effective in removing stains and killing bacteria, ensuring that dentures remain clean and hygienic. Powders are often preferred by users who appreciate a straightforward cleaning process that doesn't require scrubbing or manual cleaning. On the other hand, creams offer a more targeted approach to denture cleaning. They are applied directly to the dentures and then brushed off, similar to toothpaste. This method allows users to focus on specific areas that may require more attention, such as stubborn stains or hard-to-reach spots. Creams are often formulated with additional ingredients that help to whiten dentures and improve their appearance, making them a popular choice for those who are concerned about aesthetics. Other forms of denture disinfectants include wipes and sprays, which offer convenience and portability. Wipes are particularly useful for quick clean-ups when traveling or when a full cleaning routine is not feasible. They are pre-moistened with a disinfectant solution and can be used to wipe down dentures, removing food particles and bacteria. Sprays, on the other hand, are designed to be sprayed directly onto the dentures, providing a quick and easy way to disinfect them without the need for soaking or brushing. These alternative forms of denture disinfectants are gaining popularity among consumers who lead busy lifestyles and require quick and efficient cleaning solutions. The choice between powders, creams, and other forms of denture disinfectants often depends on individual preferences and lifestyle needs. Some users may prefer the thorough cleaning provided by soaking powders, while others may opt for the convenience of wipes or sprays. Additionally, the availability of these products in various formulations, such as those with added whitening agents or natural ingredients, allows consumers to choose products that align with their personal values and health considerations. As the market for denture disinfectants continues to grow, manufacturers are likely to innovate and introduce new products that cater to the evolving needs of consumers. This could include the development of more eco-friendly options, as well as products that offer additional benefits such as improved taste or enhanced antibacterial properties. Overall, the global market for denture disinfectants is characterized by a diverse range of products that cater to different consumer preferences and needs, ensuring that individuals who wear dentures have access to effective and convenient cleaning solutions.

Hospital Pharmacy, Retail Pharmacy, E-commerce, Others in the Denture Disinfectants - Global Market:

Denture disinfectants are widely used across various distribution channels, including hospital pharmacies, retail pharmacies, e-commerce platforms, and other outlets. In hospital pharmacies, these products are often recommended by dental professionals as part of a comprehensive oral care routine for patients who wear dentures. Hospital pharmacies provide a reliable source of high-quality denture disinfectants, ensuring that patients have access to products that meet medical standards. This channel is particularly important for individuals who require specialized care or who have specific oral health needs that necessitate the use of certain types of disinfectants. Retail pharmacies also play a significant role in the distribution of denture disinfectants. These pharmacies offer a wide range of products, allowing consumers to choose from various brands and formulations. Retail pharmacies are convenient for consumers who prefer to purchase denture disinfectants in person and who may seek advice from pharmacists regarding the best products for their needs. The availability of denture disinfectants in retail pharmacies makes them accessible to a broad audience, including those who may not have regular access to dental care. E-commerce platforms have become increasingly popular for purchasing denture disinfectants, offering consumers the convenience of shopping from home. Online platforms provide a vast selection of products, often at competitive prices, and allow consumers to easily compare different brands and formulations. The rise of e-commerce has made it easier for consumers to access denture disinfectants, particularly in regions where physical stores may be limited. Additionally, online reviews and ratings provide valuable insights into the effectiveness of different products, helping consumers make informed purchasing decisions. Other distribution channels for denture disinfectants include supermarkets, health stores, and dental clinics. Supermarkets and health stores offer the convenience of purchasing denture disinfectants alongside other household and personal care items, making them a convenient option for consumers who prefer one-stop shopping. Dental clinics may also offer denture disinfectants as part of their services, providing patients with professional recommendations and ensuring that they have access to high-quality products. The diverse range of distribution channels for denture disinfectants reflects the growing demand for these products and the importance of maintaining oral hygiene for individuals who wear dentures. As the market continues to expand, it is likely that new distribution channels will emerge, further increasing the accessibility of denture disinfectants to consumers worldwide.

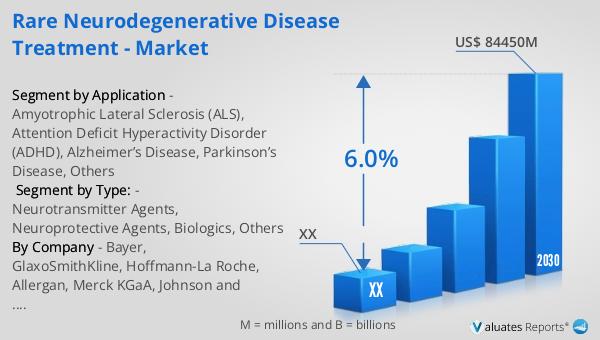

Denture Disinfectants - Global Market Outlook:

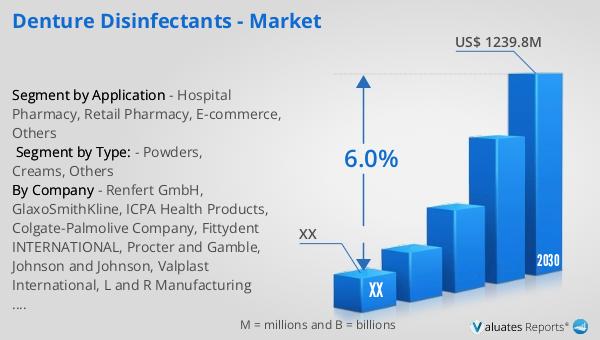

The global market for denture disinfectants was valued at approximately $826 million in 2023. It is projected to grow significantly, reaching an estimated size of $1,239.8 million by 2030. This growth represents a compound annual growth rate (CAGR) of 6.0% during the forecast period from 2024 to 2030. This upward trend in the denture disinfectants market is indicative of the increasing awareness and importance of oral hygiene, particularly among the aging population who are more likely to use dentures. The market's growth is also supported by advancements in dental care and the availability of a wide range of products catering to different consumer needs. In comparison, the global market for medical devices is estimated to be worth $603 billion in 2023, with a projected CAGR of 5% over the next six years. This highlights the significant role that denture disinfectants play within the broader medical devices market, as they contribute to the overall focus on preventive healthcare and improved quality of life for individuals who rely on dentures. The growth in both markets underscores the increasing demand for healthcare products that enhance well-being and address specific health needs.

| Report Metric | Details |

| Report Name | Denture Disinfectants - Market |

| Forecasted market size in 2030 | US$ 1239.8 million |

| CAGR | 6.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Renfert GmbH, GlaxoSmithKline, ICPA Health Products, Colgate-Palmolive Company, Fittydent INTERNATIONAL, Procter and Gamble, Johnson and Johnson, Valplast International, L and R Manufacturing Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |