What is Soybean Soluble Polysaccharide - Global Market?

Soybean Soluble Polysaccharide (SSPS) is a unique component derived from soybeans, primarily used for its functional properties in various industries. It is a type of carbohydrate that dissolves in water, making it highly versatile for different applications. SSPS is known for its ability to stabilize emulsions, improve texture, and enhance the mouthfeel of food and beverage products. Its natural origin and functional benefits make it an attractive ingredient in the global market, especially as consumers increasingly seek out plant-based and clean-label products. The market for SSPS is driven by its use in food and beverages, pharmaceuticals, and other industrial applications. As the demand for healthier and more sustainable ingredients grows, the global market for Soybean Soluble Polysaccharide is expected to expand, offering opportunities for innovation and development in various sectors. The increasing awareness of the health benefits associated with soy-based products further fuels the market's growth, making SSPS a significant player in the global ingredient landscape.

Soybean Polysaccharides -A, Soybean Polysaccharides –B in the Soybean Soluble Polysaccharide - Global Market:

Soybean Polysaccharides are categorized into different types, with Soybean Polysaccharides-A and Soybean Polysaccharides-B being notable variants. These polysaccharides are derived from the cell walls of soybeans and are known for their unique properties that make them suitable for various applications. Soybean Polysaccharides-A is primarily used for its excellent water solubility and ability to form gels, making it ideal for use in food products that require thickening or stabilization. It is often used in dairy products, sauces, and dressings to improve texture and consistency. On the other hand, Soybean Polysaccharides-B is recognized for its emulsifying properties, which help in creating stable emulsions in products like mayonnaise, salad dressings, and certain beverages. The global market for these polysaccharides is influenced by the growing demand for natural and plant-based ingredients, as consumers become more health-conscious and environmentally aware. The versatility of Soybean Polysaccharides-A and B allows manufacturers to innovate and develop new products that cater to these consumer preferences. Additionally, the use of these polysaccharides in non-food applications, such as pharmaceuticals and cosmetics, further expands their market potential. The ability of Soybean Polysaccharides to enhance the functional properties of products while maintaining a clean label appeal makes them a valuable ingredient in the global market. As research continues to uncover new applications and benefits of these polysaccharides, their market presence is expected to grow, offering opportunities for both established companies and new entrants in the industry. The global market for Soybean Polysaccharides is characterized by a competitive landscape, with key players focusing on product innovation and strategic partnerships to strengthen their market position. The increasing demand for sustainable and plant-based ingredients is likely to drive further growth in this market, as consumers seek out products that align with their values and lifestyle choices. Overall, Soybean Polysaccharides-A and B represent a promising segment within the broader Soybean Soluble Polysaccharide market, with significant potential for expansion and development in the coming years.

Rice and Flour, Drinking, Biomedicine, Others in the Soybean Soluble Polysaccharide - Global Market:

Soybean Soluble Polysaccharide finds diverse applications across various sectors, including rice and flour products, beverages, biomedicine, and other industries. In the rice and flour sector, SSPS is used to improve the texture and shelf life of products. It acts as a stabilizer and thickener, enhancing the quality of noodles, bread, and other baked goods. The ability of SSPS to retain moisture and prevent staling makes it a valuable ingredient in this industry, where product freshness is crucial. In the beverage industry, SSPS is utilized for its emulsifying properties, which help in creating stable and homogenous products. It is commonly used in fruit juices, dairy drinks, and plant-based beverages to improve mouthfeel and prevent separation. The natural origin of SSPS aligns with the growing consumer demand for clean-label and plant-based products, making it a popular choice among manufacturers. In the field of biomedicine, SSPS is explored for its potential health benefits, including its role as a dietary fiber and its prebiotic properties. Research suggests that SSPS may support gut health and improve digestion, making it an attractive ingredient for functional foods and supplements. Additionally, SSPS is used in other industries, such as cosmetics and personal care, where its moisturizing and film-forming properties are valued. The versatility of Soybean Soluble Polysaccharide allows it to be used in a wide range of applications, catering to the diverse needs of consumers and industries alike. As the demand for sustainable and health-promoting ingredients continues to rise, the usage of SSPS in these areas is expected to grow, offering opportunities for innovation and development in the global market.

Soybean Soluble Polysaccharide - Global Market Outlook:

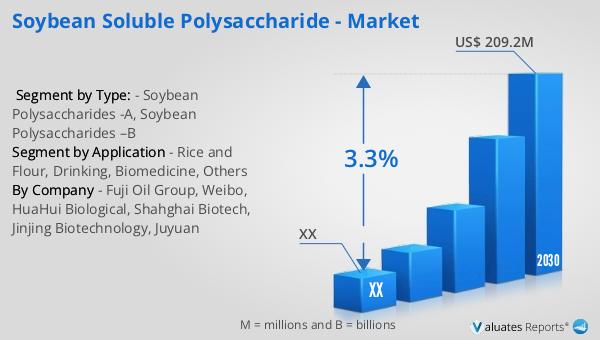

The global market for Soybean Soluble Polysaccharide was valued at approximately US$ 165.9 million in 2023, with projections indicating a growth to about US$ 209.2 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2024 to 2030. Japan currently holds the largest share of the Soluble Soybean Polysaccharides market, accounting for around 61% of the market share. Following Japan, China is a significant player in the market, with approximately 35% market share. The market is highly concentrated, with the top three companies occupying about 89% of the market share. This concentration indicates a competitive landscape where a few key players dominate the market. The growth of the Soybean Soluble Polysaccharide market is driven by the increasing demand for natural and plant-based ingredients across various industries. As consumers become more health-conscious and environmentally aware, the demand for sustainable and functional ingredients like SSPS is expected to rise. The market outlook suggests a positive trajectory for SSPS, with opportunities for innovation and expansion in the coming years.

| Report Metric | Details |

| Report Name | Soybean Soluble Polysaccharide - Market |

| Forecasted market size in 2030 | US$ 209.2 million |

| CAGR | 3.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Fuji Oil Group, Weibo, HuaHui Biological, Shahghai Biotech, Jinjing Biotechnology, Juyuan |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |