What is Bentonite for Paper Retention Aid - Global Market?

Bentonite is a naturally occurring clay that has found significant application in the paper industry as a retention aid. Retention aids are crucial in paper production as they help in retaining fine particles and fillers during the paper-making process, thereby improving the quality and efficiency of paper production. Bentonite, with its unique properties, enhances the retention of fibers and fillers, leading to better paper formation and reduced raw material loss. The global market for Bentonite as a paper retention aid is driven by the increasing demand for high-quality paper products and the need for efficient production processes. Bentonite's ability to improve drainage and retention in the paper-making process makes it a valuable component in the industry. Its natural and environmentally friendly characteristics also align with the growing trend towards sustainable and eco-friendly production methods. As the paper industry continues to evolve, the demand for Bentonite as a retention aid is expected to grow, driven by its effectiveness and environmental benefits.

Kaolin, Activated Bentonite, Calcium Bentonite in the Bentonite for Paper Retention Aid - Global Market:

Kaolin, Activated Bentonite, and Calcium Bentonite are three types of clays that play significant roles in the global market for Bentonite as a paper retention aid. Kaolin, also known as china clay, is a soft white clay that is an essential ingredient in the paper industry. It is used to improve the brightness, smoothness, and printability of paper. Kaolin's fine particle size and platy shape make it an excellent filler and coating material, enhancing the paper's overall quality. In the context of Bentonite for paper retention aid, Kaolin works synergistically with Bentonite to improve the retention of fillers and fine particles, leading to better paper formation and reduced material loss. Activated Bentonite, on the other hand, is Bentonite that has been chemically treated to enhance its adsorption properties. This type of Bentonite is particularly effective in improving the retention of fine particles and fillers in the paper-making process. The activation process increases the surface area and porosity of Bentonite, making it more effective in capturing and retaining particles. This results in improved paper quality and reduced production costs. Activated Bentonite is also valued for its ability to improve drainage and reduce the need for additional chemicals in the paper-making process, aligning with the industry's move towards more sustainable practices. Calcium Bentonite is another variant of Bentonite that is used in the paper industry. It is known for its high absorption capacity and ability to improve the retention of fillers and fine particles. Calcium Bentonite's unique properties make it an effective retention aid, enhancing the paper's quality and reducing raw material loss. Its natural and environmentally friendly characteristics also make it an attractive option for paper manufacturers looking to adopt more sustainable production methods. In the global market for Bentonite as a paper retention aid, these three types of clays play complementary roles, each contributing to the overall efficiency and quality of the paper-making process. As the demand for high-quality paper products continues to grow, the use of Kaolin, Activated Bentonite, and Calcium Bentonite as retention aids is expected to increase, driven by their effectiveness and environmental benefits.

Paper Production, Wastewater Treatment in the Bentonite for Paper Retention Aid - Global Market:

Bentonite is widely used in the paper industry as a retention aid, playing a crucial role in paper production and wastewater treatment. In paper production, Bentonite is used to improve the retention of fine particles and fillers, which are essential for producing high-quality paper. The retention of these particles is critical as it directly impacts the paper's strength, smoothness, and printability. Bentonite's unique properties, such as its high surface area and cation exchange capacity, make it an effective retention aid, enhancing the paper's overall quality and reducing raw material loss. By improving the retention of fillers and fine particles, Bentonite helps in reducing the need for additional chemicals, aligning with the industry's move towards more sustainable and eco-friendly production methods. In wastewater treatment, Bentonite is used for its excellent adsorption and flocculation properties. It is effective in removing impurities and contaminants from wastewater, making it a valuable component in the treatment process. Bentonite's ability to adsorb heavy metals, organic compounds, and other pollutants makes it an essential material for wastewater treatment facilities. Its natural and environmentally friendly characteristics also make it an attractive option for facilities looking to adopt more sustainable treatment methods. By improving the efficiency of the treatment process, Bentonite helps in reducing the environmental impact of wastewater discharge, contributing to the overall sustainability of the industry. As the demand for high-quality paper products and sustainable wastewater treatment solutions continues to grow, the use of Bentonite in these areas is expected to increase, driven by its effectiveness and environmental benefits.

Bentonite for Paper Retention Aid - Global Market Outlook:

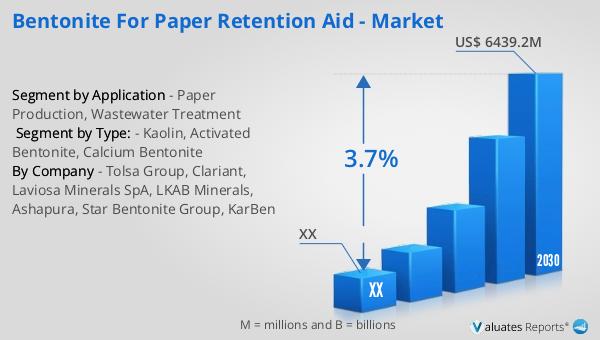

The global market for Bentonite as a paper retention aid was valued at approximately US$ 5008 million in 2023. It is projected to reach a revised size of US$ 6439.2 million by 2030, growing at a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2024 to 2030. This growth is largely attributed to the increasing awareness of environmental issues and the need for sustainable development. As industries worldwide strive to reduce their environmental footprint, the demand for eco-friendly retention aids like Bentonite is expected to rise. Bentonite's natural and environmentally friendly properties make it an ideal choice for paper manufacturers looking to adopt more sustainable production methods. Its ability to improve the retention of fine particles and fillers in the paper-making process not only enhances the quality of the paper but also reduces the need for additional chemicals, aligning with the industry's move towards more sustainable practices. As the global market continues to evolve, the demand for Bentonite as a paper retention aid is expected to grow, driven by its effectiveness and environmental benefits.

| Report Metric | Details |

| Report Name | Bentonite for Paper Retention Aid - Market |

| Forecasted market size in 2030 | US$ 6439.2 million |

| CAGR | 3.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Tolsa Group, Clariant, Laviosa Minerals SpA, LKAB Minerals, Ashapura, Star Bentonite Group, KarBen |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |