What is Lever Coffee Machine - Global Market?

Lever coffee machines are a fascinating segment of the global coffee machine market, known for their unique design and operation. These machines are distinguished by their manual operation, where the user exerts pressure on a lever to force hot water through the coffee grounds, producing a rich and flavorful espresso. The global market for lever coffee machines is characterized by a blend of tradition and innovation, appealing to both coffee enthusiasts and professional baristas. These machines are often seen as a symbol of craftsmanship and precision, offering a hands-on experience that many coffee lovers cherish. The market is driven by a growing appreciation for artisanal coffee-making methods and the desire for high-quality, customizable coffee experiences. As consumers become more discerning about their coffee, the demand for lever coffee machines is expected to grow, with manufacturers continually innovating to enhance functionality and user experience. The market is also influenced by trends in home brewing and the increasing popularity of specialty coffee shops, which often showcase lever machines as part of their premium offerings. Overall, the lever coffee machine market is a dynamic and evolving space, reflecting broader trends in the global coffee industry.

Manual Lever Coffee Machine, Semi-Automatic Lever Coffee Machine, Fully Automatic Lever Coffee Machine in the Lever Coffee Machine - Global Market:

Manual lever coffee machines are the most traditional type of lever machines, requiring the user to manually control the entire brewing process. These machines are prized for their ability to produce a highly customized espresso, as the user can adjust variables such as pressure and extraction time. This level of control allows for a personalized coffee experience, making manual lever machines a favorite among coffee purists and enthusiasts who enjoy the art of espresso making. However, they require a certain level of skill and practice to master, which can be a barrier for some users. Despite this, the satisfaction of crafting a perfect shot of espresso with a manual lever machine is unmatched for many coffee lovers. Semi-automatic lever coffee machines offer a middle ground between manual and fully automatic machines. They incorporate some automated features, such as temperature control and pre-infusion, while still allowing the user to manually control the lever to adjust pressure. This combination of automation and manual control makes semi-automatic machines appealing to both novice and experienced users, providing a balance of convenience and customization. These machines are often favored in settings where consistency and efficiency are important, such as in busy coffee shops or households with multiple coffee drinkers. Fully automatic lever coffee machines, on the other hand, are designed for maximum convenience, automating most of the brewing process. These machines are equipped with advanced features such as programmable settings, automatic grinding, and milk frothing, allowing users to create a variety of coffee drinks with minimal effort. Fully automatic machines are ideal for those who want the quality of a lever machine without the need for manual intervention. They are particularly popular in commercial settings, where speed and consistency are crucial, as well as in homes where convenience is a priority. Despite their higher price point, the ease of use and versatility of fully automatic lever machines make them a worthwhile investment for many coffee lovers. Each type of lever coffee machine has its own unique appeal, catering to different preferences and needs within the global market.

Coffee Shop, Family in the Lever Coffee Machine - Global Market:

Lever coffee machines are widely used in coffee shops and family settings, each offering unique benefits and experiences. In coffee shops, lever machines are often seen as a mark of quality and craftsmanship. They allow baristas to showcase their skills and create a personalized coffee experience for customers. The manual operation of lever machines enables baristas to fine-tune each shot of espresso, adjusting variables such as pressure and extraction time to achieve the desired flavor profile. This level of customization is highly valued in specialty coffee shops, where customers are willing to pay a premium for a unique and high-quality coffee experience. Lever machines also add a theatrical element to the coffee-making process, enhancing the overall ambiance of the coffee shop and attracting coffee enthusiasts who appreciate the artistry involved. In family settings, lever coffee machines offer a different set of advantages. They provide an opportunity for coffee lovers to engage in the art of espresso making at home, allowing them to experiment with different techniques and flavors. Manual lever machines, in particular, are popular among families who enjoy the hands-on experience and the satisfaction of crafting their own coffee. These machines encourage a deeper appreciation for the coffee-making process and can become a cherished part of family rituals and gatherings. Semi-automatic and fully automatic lever machines are also popular in family settings, offering a balance of convenience and quality. They allow family members to enjoy a variety of coffee drinks with ease, catering to different preferences and tastes. The versatility and user-friendly features of these machines make them suitable for households with multiple coffee drinkers, ensuring that everyone can enjoy their favorite coffee beverage. Overall, the use of lever coffee machines in coffee shops and family settings reflects a broader trend towards high-quality, customizable coffee experiences, driven by a growing appreciation for artisanal coffee-making methods.

Lever Coffee Machine - Global Market Outlook:

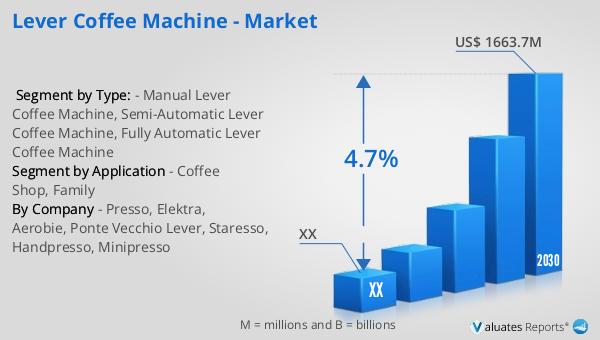

The global market for lever coffee machines was valued at approximately $1,208 million in 2023. This market is projected to grow significantly, reaching an estimated size of $1,663.7 million by 2030. This growth represents a compound annual growth rate (CAGR) of 4.7% during the forecast period from 2024 to 2030. This upward trend is indicative of the increasing demand for high-quality coffee experiences and the growing popularity of lever coffee machines among consumers. The market's expansion is driven by several factors, including the rising interest in artisanal coffee-making methods, the proliferation of specialty coffee shops, and the increasing number of coffee enthusiasts seeking to replicate café-quality coffee at home. As consumers become more discerning about their coffee preferences, the demand for lever coffee machines is expected to continue to rise. Manufacturers are responding to this demand by innovating and introducing new features to enhance the functionality and user experience of lever machines. The market's growth also reflects broader trends in the global coffee industry, where there is a growing emphasis on quality, customization, and sustainability. Overall, the lever coffee machine market is poised for continued growth, driven by a combination of consumer preferences and industry innovation.

| Report Metric | Details |

| Report Name | Lever Coffee Machine - Market |

| Forecasted market size in 2030 | US$ 1663.7 million |

| CAGR | 4.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Presso, Elektra, Aerobie, Ponte Vecchio Lever, Staresso, Handpresso, Minipresso |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |