What is Preventive Medicine - Global Market?

Preventive medicine is a branch of healthcare focused on preventing diseases rather than treating them after they occur. The global market for preventive medicine encompasses a wide range of products and services designed to maintain health and prevent illness. This market includes vaccines, screenings, health education, and lifestyle interventions aimed at reducing the risk of chronic diseases such as heart disease, diabetes, and cancer. The demand for preventive medicine is driven by the increasing awareness of the benefits of early detection and prevention, as well as the rising costs of healthcare. Governments and healthcare organizations worldwide are investing in preventive measures to improve public health outcomes and reduce the burden on healthcare systems. The preventive medicine market is also influenced by technological advancements, such as digital health tools and personalized medicine, which enable more effective and targeted prevention strategies. As a result, the global market for preventive medicine is expected to continue growing as more individuals and healthcare providers recognize the importance of prevention in achieving long-term health and wellness.

Public Health and General Preventive Medicine, Occupational Medicine, Military Preventive Medicine in the Preventive Medicine - Global Market:

Public Health and General Preventive Medicine is a specialty that focuses on promoting health and preventing disease across populations. This field involves a broad range of activities, including health education, policy development, and community health initiatives. Public health professionals work to identify health risks and implement strategies to mitigate them, often collaborating with government agencies, non-profit organizations, and healthcare providers. They play a crucial role in addressing public health challenges such as infectious disease outbreaks, chronic disease prevention, and health disparities. Occupational Medicine, on the other hand, is a branch of preventive medicine that focuses on the health and safety of workers. Occupational medicine specialists work to prevent work-related injuries and illnesses by assessing workplace hazards, implementing safety protocols, and promoting healthy work environments. They also provide medical care and rehabilitation for injured workers, helping them return to work safely. Military Preventive Medicine is a specialized field that focuses on the health and well-being of military personnel. This includes preventing and managing health issues related to military service, such as infectious diseases, environmental exposures, and mental health challenges. Military preventive medicine professionals work to ensure that service members are healthy and fit for duty, often in challenging and austere environments. They also play a critical role in disaster response and humanitarian missions, providing medical support and public health expertise in crisis situations. The global market for preventive medicine in these areas is driven by the need to protect and promote the health of diverse populations, from workers and military personnel to entire communities. As the world becomes more interconnected and complex, the demand for preventive medicine is expected to grow, with a focus on innovative solutions and collaborative approaches to health promotion and disease prevention.

Hospital, Clinic, Others in the Preventive Medicine - Global Market:

The usage of preventive medicine in hospitals, clinics, and other healthcare settings is essential for maintaining public health and reducing the burden of disease. In hospitals, preventive medicine plays a crucial role in infection control, patient education, and chronic disease management. Hospitals implement preventive measures such as vaccination programs, health screenings, and lifestyle counseling to prevent the spread of infectious diseases and manage chronic conditions. These efforts not only improve patient outcomes but also reduce healthcare costs by preventing complications and hospital readmissions. In clinics, preventive medicine is often the first line of defense against disease. Primary care providers offer a range of preventive services, including immunizations, screenings, and health education, to help patients maintain their health and prevent illness. Clinics also play a vital role in managing chronic diseases, providing ongoing care and support to help patients manage their conditions and prevent complications. Other healthcare settings, such as community health centers and public health departments, also play a critical role in preventive medicine. These organizations often focus on underserved populations, providing essential preventive services to those who may not have access to traditional healthcare. They offer programs such as smoking cessation, nutrition counseling, and exercise classes to promote healthy lifestyles and prevent disease. The global market for preventive medicine in these settings is driven by the increasing demand for cost-effective and accessible healthcare solutions. As healthcare systems worldwide face rising costs and growing patient populations, the focus on prevention is becoming more important than ever. By investing in preventive medicine, healthcare providers can improve patient outcomes, reduce costs, and promote long-term health and wellness.

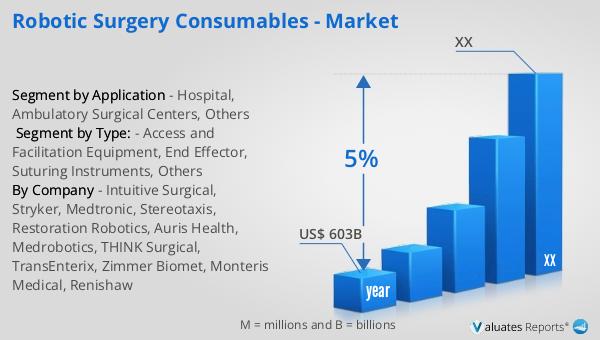

Preventive Medicine - Global Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare needs, and a growing emphasis on preventive care. As the global population continues to age and the prevalence of chronic diseases rises, there is a heightened demand for medical devices that can aid in early diagnosis, monitoring, and management of health conditions. Innovations in medical technology, such as wearable devices and telemedicine, are also contributing to the expansion of the market by providing more accessible and efficient healthcare solutions. Furthermore, the shift towards personalized medicine and the integration of artificial intelligence in healthcare are expected to enhance the capabilities of medical devices, making them more effective in preventing and managing diseases. As healthcare systems worldwide strive to improve patient outcomes and reduce costs, the role of medical devices in preventive medicine is becoming increasingly significant. This market outlook highlights the potential for growth and innovation in the medical device industry, as it continues to evolve to meet the changing needs of patients and healthcare providers.

| Report Metric | Details |

| Report Name | Preventive Medicine - Market |

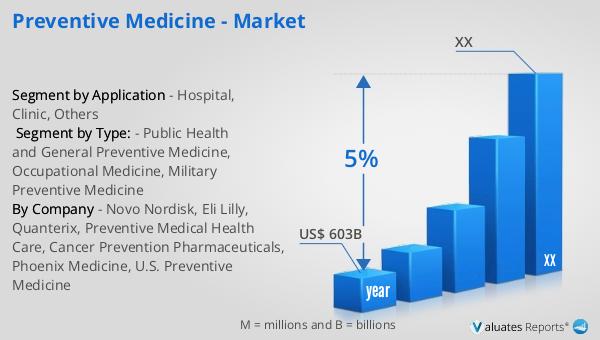

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Novo Nordisk, Eli Lilly, Quanterix, Preventive Medical Health Care, Cancer Prevention Pharmaceuticals, Phoenix Medicine, U.S. Preventive Medicine |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |