What is 1.5 T Superconductive Magnet MRI Syetem - Global Market?

The 1.5 T Superconductive Magnet MRI System is a crucial component in the global medical imaging market. MRI, or Magnetic Resonance Imaging, is a non-invasive diagnostic tool that uses powerful magnets and radio waves to create detailed images of the organs and tissues within the body. The "1.5 T" refers to the strength of the magnetic field, measured in Tesla, which is a unit of magnetic flux density. A 1.5 Tesla MRI is considered a standard strength in clinical settings, offering a balance between image quality and cost-effectiveness. Superconductive magnets are used in these systems because they can produce a strong magnetic field without the need for a continuous power supply, making them more efficient and reliable. The global market for these systems is driven by the increasing demand for advanced diagnostic tools, the rising prevalence of chronic diseases, and technological advancements in MRI technology. As healthcare providers seek to improve diagnostic accuracy and patient outcomes, the adoption of 1.5 T MRI systems is expected to grow, particularly in emerging markets where healthcare infrastructure is rapidly developing. These systems are essential for a wide range of medical applications, from routine examinations to complex diagnostic procedures, making them a vital part of modern healthcare.

8 Receiving Channels, 16 Receiving Channels in the 1.5 T Superconductive Magnet MRI Syetem - Global Market:

The 1.5 T Superconductive Magnet MRI System is available with different configurations of receiving channels, such as 8 and 16 channels, which play a significant role in determining the quality and speed of imaging. Receiving channels in an MRI system refer to the number of independent pathways through which the MRI signals are received and processed. An 8-channel system has eight such pathways, while a 16-channel system has sixteen. The number of channels directly impacts the system's ability to capture detailed images and the speed at which these images can be acquired. In an 8-channel system, the MRI machine can simultaneously process signals from eight different areas of the body, which is sufficient for many standard imaging procedures. However, a 16-channel system offers enhanced capabilities, allowing for faster imaging and higher resolution images. This is particularly beneficial in complex diagnostic scenarios where detailed visualization of small structures is required. The choice between 8 and 16 channels depends on various factors, including the specific diagnostic needs, budget constraints, and the level of detail required in the images. In the global market, the demand for higher channel systems is increasing as healthcare providers seek to improve diagnostic accuracy and efficiency. The 16-channel systems are particularly popular in advanced medical facilities where high throughput and detailed imaging are critical. These systems are also more adaptable to advanced imaging techniques, such as functional MRI and diffusion tensor imaging, which require higher resolution and faster data acquisition. As the technology continues to evolve, the distinction between 8 and 16-channel systems may become less pronounced, with newer systems offering even more channels and capabilities. However, for now, the choice between these configurations remains an important consideration for healthcare providers looking to invest in MRI technology. The global market for 1.5 T Superconductive Magnet MRI Systems is expected to continue growing as the demand for advanced diagnostic tools increases, driven by factors such as the rising prevalence of chronic diseases, aging populations, and the need for early and accurate diagnosis. As healthcare systems around the world strive to improve patient outcomes and reduce costs, the adoption of advanced MRI systems with multiple receiving channels is likely to become more widespread.

Head and Neck Examination, Abdomen Examination, Extremity Examination, Spine Examination, Others in the 1.5 T Superconductive Magnet MRI Syetem - Global Market:

The 1.5 T Superconductive Magnet MRI System is widely used in various medical examinations, including head and neck, abdomen, extremity, spine, and others. In head and neck examinations, the 1.5 T MRI system provides detailed images of the brain, skull, and surrounding tissues, making it an essential tool for diagnosing neurological conditions, tumors, and vascular abnormalities. The high-resolution images produced by the system allow for accurate assessment of complex structures, aiding in the diagnosis and treatment planning for conditions such as stroke, multiple sclerosis, and brain tumors. In abdomen examinations, the 1.5 T MRI system is used to visualize organs such as the liver, kidneys, pancreas, and spleen. It is particularly useful for detecting tumors, cysts, and other abnormalities, as well as assessing the extent of diseases such as liver cirrhosis and pancreatic cancer. The non-invasive nature of MRI makes it a preferred choice for patients who require frequent monitoring of chronic conditions. For extremity examinations, the 1.5 T MRI system provides detailed images of the joints, muscles, and bones, making it an invaluable tool for diagnosing sports injuries, arthritis, and other musculoskeletal conditions. The system's ability to produce high-resolution images of soft tissues allows for accurate assessment of ligament tears, cartilage damage, and other injuries that may not be visible on X-rays or CT scans. In spine examinations, the 1.5 T MRI system is used to assess the vertebrae, spinal cord, and surrounding tissues. It is particularly useful for diagnosing conditions such as herniated discs, spinal stenosis, and tumors. The detailed images produced by the system allow for accurate assessment of the extent of the condition, aiding in treatment planning and monitoring of disease progression. In addition to these specific areas, the 1.5 T MRI system is also used in a wide range of other medical examinations, including cardiac imaging, breast imaging, and whole-body scans. Its versatility and ability to produce high-quality images make it an essential tool in modern healthcare, enabling accurate diagnosis and treatment planning for a wide range of conditions.

1.5 T Superconductive Magnet MRI Syetem - Global Market Outlook:

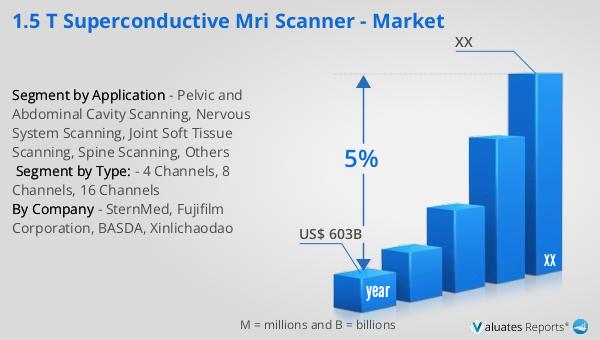

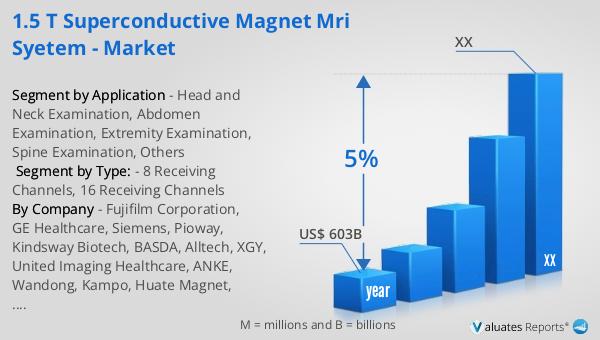

The global market outlook for the 1.5 T Superconductive Magnet MRI System is promising, with significant growth expected in the coming years. According to our research, the global market for medical devices is valued at approximately USD 603 billion in 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing demand for advanced diagnostic tools, the rising prevalence of chronic diseases, and technological advancements in medical imaging. As healthcare providers seek to improve diagnostic accuracy and patient outcomes, the adoption of 1.5 T MRI systems is expected to grow, particularly in emerging markets where healthcare infrastructure is rapidly developing. The 1.5 T MRI system offers a balance between image quality and cost-effectiveness, making it an attractive option for healthcare providers looking to invest in advanced diagnostic tools. The system's versatility and ability to produce high-quality images make it an essential tool in modern healthcare, enabling accurate diagnosis and treatment planning for a wide range of conditions. As the global market for medical devices continues to expand, the demand for 1.5 T MRI systems is expected to increase, driven by the need for early and accurate diagnosis, improved patient outcomes, and reduced healthcare costs.

| Report Metric | Details |

| Report Name | 1.5 T Superconductive Magnet MRI Syetem - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Fujifilm Corporation, GE Healthcare, Siemens, Pioway, Kindsway Biotech, BASDA, Alltech, XGY, United Imaging Healthcare, ANKE, Wandong, Kampo, Huate Magnet, Neusoft |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |