What is LCP Soft Board - Global Market?

LCP Soft Board, or Liquid Crystal Polymer Soft Board, is a specialized material used in various industries due to its unique properties. It is a type of flexible circuit board made from liquid crystal polymers, which are known for their excellent thermal and mechanical stability. These boards are lightweight, have high tensile strength, and are resistant to moisture and chemicals, making them ideal for demanding applications. The global market for LCP Soft Boards is expanding as industries seek materials that can withstand harsh environments while maintaining performance. These boards are particularly popular in electronics, automotive, and telecommunications sectors, where they are used to create compact and efficient devices. The demand for LCP Soft Boards is driven by the need for miniaturization and the increasing complexity of electronic devices. As technology advances, the need for materials that can support high-speed data transmission and high-frequency applications grows, further boosting the market for LCP Soft Boards. The global market is characterized by continuous innovation and development, with manufacturers focusing on improving the performance and reducing the cost of these boards to meet the evolving needs of various industries.

Single Layer, Dual Layers, Multi Layers in the LCP Soft Board - Global Market:

In the realm of LCP Soft Boards, the market is segmented based on the number of layers these boards possess, namely Single Layer, Dual Layers, and Multi Layers. Each type serves distinct purposes and is chosen based on the specific requirements of the application. Single Layer LCP Soft Boards are the simplest form, consisting of a single conductive layer. They are typically used in applications where space is limited, and the complexity of the circuit is minimal. These boards are cost-effective and easy to manufacture, making them suitable for basic electronic devices and simple circuits. Despite their simplicity, they offer the essential benefits of LCP materials, such as thermal stability and resistance to environmental factors. Dual Layer LCP Soft Boards, on the other hand, provide an additional layer of circuitry, allowing for more complex designs and increased functionality. This type is often used in applications that require a moderate level of complexity, such as in certain automotive and consumer electronics. The dual-layer configuration allows for more connections and components, enhancing the device's capabilities without significantly increasing its size or weight. Multi Layer LCP Soft Boards represent the most advanced and complex category. These boards can have multiple layers of circuitry, enabling highly sophisticated designs and functionalities. They are essential in high-performance applications where space is at a premium, and the device requires a high level of integration. Industries such as telecommunications, aerospace, and advanced computing often rely on multi-layer boards to meet their demanding specifications. The ability to stack multiple layers allows for intricate circuit designs that can handle high-speed data processing and transmission. The choice between single, dual, and multi-layer LCP Soft Boards depends on several factors, including the complexity of the circuit, the space available, and the specific performance requirements of the application. As technology continues to evolve, the demand for more complex and capable LCP Soft Boards is expected to grow, driving innovation and development in this market segment. Manufacturers are continually exploring new ways to enhance the performance of these boards, such as improving their thermal management capabilities and reducing their overall weight, to meet the ever-increasing demands of modern technology.

Semiconductor, Automotive, Electronic, Others in the LCP Soft Board - Global Market:

LCP Soft Boards find extensive usage across various industries, including semiconductors, automotive, electronics, and others, due to their unique properties and versatility. In the semiconductor industry, LCP Soft Boards are used to create flexible circuits that can be integrated into compact and complex devices. Their excellent thermal stability and resistance to environmental factors make them ideal for use in semiconductor applications, where precision and reliability are paramount. These boards help in miniaturizing semiconductor devices while maintaining their performance, which is crucial in the development of advanced electronic components. In the automotive industry, LCP Soft Boards are used in various applications, including in-vehicle infotainment systems, advanced driver-assistance systems (ADAS), and other electronic components. The automotive sector demands materials that can withstand harsh conditions, such as extreme temperatures and vibrations, making LCP Soft Boards an ideal choice. Their lightweight nature also contributes to the overall efficiency of the vehicle by reducing weight and improving fuel economy. In the electronics industry, LCP Soft Boards are used in a wide range of applications, from consumer electronics to industrial equipment. They are essential in the production of compact and efficient electronic devices, such as smartphones, tablets, and wearable technology. The ability of LCP Soft Boards to support high-speed data transmission and high-frequency applications makes them indispensable in the development of modern electronic devices. Other industries, such as telecommunications and aerospace, also benefit from the use of LCP Soft Boards. In telecommunications, these boards are used in the production of high-frequency antennas and other communication devices, where their ability to handle high-speed data transmission is crucial. In aerospace, the lightweight and durable nature of LCP Soft Boards makes them suitable for use in various applications, including satellite systems and avionics. The versatility and performance of LCP Soft Boards make them a valuable component in numerous industries, driving their demand in the global market.

LCP Soft Board - Global Market Outlook:

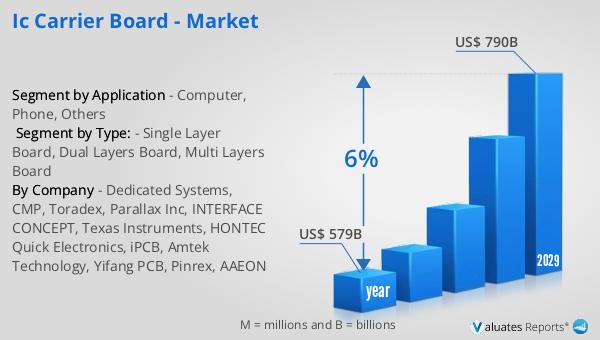

The global semiconductor market, valued at approximately $579 billion in 2022, is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, and telecommunications. The rapid advancement in technology and the growing trend of digitalization are key factors contributing to the expansion of the semiconductor market. As industries continue to innovate and develop new technologies, the need for advanced semiconductor components is expected to rise, further propelling the market's growth. The semiconductor industry plays a crucial role in the development of modern technology, providing the essential components needed for the functioning of electronic devices. The increasing adoption of technologies such as artificial intelligence, the Internet of Things (IoT), and 5G is expected to drive the demand for semiconductors, as these technologies require advanced and efficient components to operate effectively. The projected growth of the semiconductor market highlights the importance of continuous innovation and development in this sector to meet the evolving needs of various industries. As the market expands, companies are focusing on enhancing their production capabilities and investing in research and development to create more efficient and cost-effective semiconductor solutions.

| Report Metric | Details |

| Report Name | LCP Soft Board - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Micro Systems Technologies, NIPPON MEKTRON, Level Developments, MFLEX, Murata Manufacturing Co, Zhuyoudiangong, PS Electronics Co., Ltd, Career Technology, Avary Holdings, Helitai, Kingwang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |