What is Die Attach Film Tape - Global Market?

Die attach film tape is a specialized adhesive material used in the semiconductor industry to attach semiconductor dies to substrates or other components. This market is a crucial part of the electronics manufacturing process, as it ensures the stability and performance of semiconductor devices. The global market for die attach film tape has been growing steadily due to the increasing demand for electronic devices, such as smartphones, tablets, and other consumer electronics. These tapes offer several advantages, including high thermal conductivity, excellent adhesion properties, and the ability to withstand high temperatures, making them ideal for use in various electronic applications. The market is driven by technological advancements in semiconductor manufacturing processes and the growing trend towards miniaturization of electronic components. As the demand for smaller and more efficient electronic devices continues to rise, the need for reliable and high-performance die attach film tapes is expected to increase, further fueling the growth of this market. The market is also influenced by the increasing adoption of advanced packaging technologies, such as flip-chip and wafer-level packaging, which require high-quality die attach materials to ensure optimal performance and reliability.

Non-Conductive Type, Conductive Type in the Die Attach Film Tape - Global Market:

Die attach film tapes are categorized into two main types: non-conductive and conductive. Non-conductive die attach film tapes are primarily used in applications where electrical insulation is required between the die and the substrate. These tapes are designed to provide strong adhesion while preventing electrical currents from passing through, making them ideal for use in devices where electrical isolation is critical. Non-conductive tapes are often used in applications such as LED packaging, where maintaining electrical isolation between components is essential to prevent short circuits and ensure the longevity of the device. These tapes are also used in various consumer electronics, automotive electronics, and telecommunications equipment, where reliable electrical insulation is necessary to maintain device performance and safety. On the other hand, conductive die attach film tapes are used in applications where electrical conductivity between the die and the substrate is required. These tapes are designed to provide both strong adhesion and efficient electrical conduction, making them suitable for use in devices where electrical connectivity is crucial. Conductive tapes are often used in power devices, RF modules, and other high-frequency applications where efficient heat dissipation and electrical conduction are necessary to ensure optimal device performance. The choice between non-conductive and conductive die attach film tapes depends on the specific requirements of the application, including the need for electrical insulation or conductivity, thermal management, and mechanical stability. Both types of tapes are essential in the semiconductor industry, as they play a critical role in ensuring the performance, reliability, and longevity of electronic devices. The global market for die attach film tapes is expected to continue growing as the demand for advanced electronic devices increases, driven by technological advancements and the ongoing trend towards miniaturization and increased functionality in consumer electronics. As manufacturers continue to develop new and innovative die attach film tapes to meet the evolving needs of the semiconductor industry, the market is likely to see further growth and diversification in the coming years.

Die to Substrate, Die to Die, Others in the Die Attach Film Tape - Global Market:

Die attach film tapes are used in various applications within the semiconductor industry, including die to substrate, die to die, and other specialized uses. In die to substrate applications, the film tape is used to attach the semiconductor die to a substrate, such as a printed circuit board (PCB) or a lead frame. This application is critical in ensuring the stability and performance of the semiconductor device, as the tape provides both mechanical support and thermal management. The use of die attach film tapes in die to substrate applications is particularly important in high-power devices, where efficient heat dissipation is necessary to prevent overheating and ensure reliable operation. In die to die applications, the film tape is used to attach multiple semiconductor dies together, creating a multi-chip module or a stacked die package. This application is becoming increasingly important as the demand for more compact and efficient electronic devices continues to grow. Die to die applications require die attach film tapes that offer excellent adhesion, thermal conductivity, and electrical insulation to ensure the performance and reliability of the multi-chip module. Other applications of die attach film tapes include their use in advanced packaging technologies, such as flip-chip and wafer-level packaging. These applications require high-performance die attach materials that can withstand the rigors of the packaging process and provide reliable adhesion and thermal management. Die attach film tapes are also used in various consumer electronics, automotive electronics, and telecommunications equipment, where their ability to provide strong adhesion, thermal management, and electrical insulation is critical to device performance and reliability. As the demand for advanced electronic devices continues to grow, the use of die attach film tapes in these applications is expected to increase, driving further growth in the global market.

Die Attach Film Tape - Global Market Outlook:

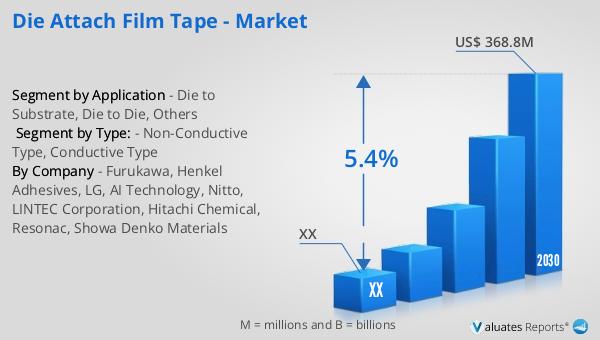

The global market for die attach film tape was valued at approximately $254 million in 2023, with projections indicating a growth to around $368.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.4% during the forecast period from 2024 to 2030. This growth trajectory highlights the increasing demand for die attach film tapes in the semiconductor industry, driven by the rising need for advanced electronic devices and the ongoing trend towards miniaturization. In 2021, the semiconductor market experienced a robust growth of 26.2%, but this was adjusted to a single-digit growth rate in 2022, reaching a total market size of $580 billion, marking a 4.4% increase. The Asia-Pacific region, which is the largest market for semiconductors, saw a decline of 2.0% in sales, amounting to $336.2 billion. In contrast, the Americas experienced a significant increase in sales, reaching $142.1 billion, up 17.0% year-on-year. Europe and Japan also saw positive growth, with sales reaching $53.8 billion and $48.1 billion, respectively, reflecting year-on-year increases of 12.6% and 10.0%. Despite the decline in the Asia-Pacific region, the overall growth in other regions underscores the global demand for semiconductor products and the critical role of die attach film tapes in supporting this demand.

| Report Metric | Details |

| Report Name | Die Attach Film Tape - Market |

| Forecasted market size in 2030 | US$ 368.8 million |

| CAGR | 5.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Furukawa, Henkel Adhesives, LG, AI Technology, Nitto, LINTEC Corporation, Hitachi Chemical, Resonac, Showa Denko Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |