What is Unmanned Driving System In Mining Areas - Global Market?

Unmanned Driving Systems in mining areas represent a significant technological advancement in the global mining industry. These systems utilize autonomous vehicles and machinery to perform tasks traditionally carried out by human operators. The primary goal is to enhance safety, efficiency, and productivity in mining operations. By removing human operators from potentially hazardous environments, these systems reduce the risk of accidents and injuries. Additionally, unmanned systems can operate continuously without breaks, leading to increased productivity and reduced operational costs. The global market for these systems is expanding as mining companies seek to leverage technology to optimize their operations. The integration of advanced sensors, artificial intelligence, and machine learning algorithms enables these systems to navigate complex mining environments autonomously. As the demand for minerals and resources continues to grow, the adoption of unmanned driving systems is expected to rise, offering a promising solution to the challenges faced by the mining industry.

5G, LTE in the Unmanned Driving System In Mining Areas - Global Market:

The integration of 5G and LTE technologies into unmanned driving systems in mining areas is revolutionizing the industry by providing robust and reliable communication networks. These technologies enable real-time data transmission, which is crucial for the operation of autonomous vehicles and machinery. 5G, with its high-speed data transfer capabilities and low latency, allows for seamless communication between the unmanned systems and the control centers. This ensures that the systems can respond quickly to changes in the environment and make informed decisions. LTE, on the other hand, provides a stable and widespread network coverage, ensuring that even remote mining areas have access to reliable communication networks. The combination of 5G and LTE technologies enhances the precision and efficiency of unmanned systems, allowing them to perform complex tasks with minimal human intervention. This technological advancement not only improves operational efficiency but also enhances safety by enabling remote monitoring and control of mining operations. The ability to transmit large volumes of data in real-time allows for better analysis and decision-making, leading to optimized resource extraction and reduced environmental impact. As the mining industry continues to evolve, the integration of 5G and LTE technologies into unmanned driving systems is expected to play a pivotal role in shaping the future of mining operations.

Coal Mine, Iron Ore, Building Materials Mine, Others in the Unmanned Driving System In Mining Areas - Global Market:

Unmanned driving systems are being increasingly utilized in various mining sectors, including coal mines, iron ore mines, and building materials mines, among others. In coal mines, these systems are employed to enhance safety and efficiency. The hazardous nature of coal mining, with risks such as gas explosions and cave-ins, makes it an ideal candidate for automation. Unmanned systems can navigate these dangerous environments without putting human lives at risk, while also improving productivity by operating continuously. In iron ore mines, the focus is on optimizing the extraction process. Unmanned systems can precisely navigate the mining site, ensuring that the extraction is done efficiently and with minimal waste. This not only increases the yield but also reduces the environmental impact of mining activities. In building materials mines, such as those extracting limestone or aggregates, unmanned systems streamline the transportation and processing of materials. By automating these processes, mining companies can reduce operational costs and improve the consistency and quality of the extracted materials. Other mining sectors are also exploring the use of unmanned systems to address specific challenges and improve overall efficiency. As the technology continues to advance, the application of unmanned driving systems in mining is expected to expand, offering innovative solutions to the industry's most pressing challenges.

Unmanned Driving System In Mining Areas - Global Market Outlook:

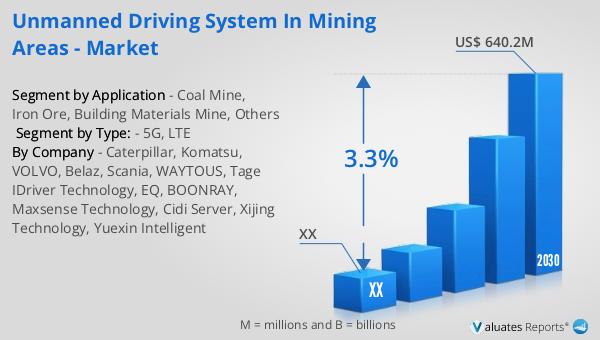

The global market for unmanned driving systems in mining areas was valued at approximately $426.4 million in 2023. It is projected to grow to a revised size of $640.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for automation and technological advancements in the mining industry. However, the market faces challenges, such as the decline in operating income of the construction machinery industry, which dropped by more than 12% in 2022, according to the China Machinery Industry Federation. This decline may impact the investment capacity of mining companies, potentially slowing down the adoption of unmanned systems. Despite these challenges, the market outlook remains positive, as the benefits of unmanned systems in terms of safety, efficiency, and cost-effectiveness continue to drive their adoption. As mining companies seek to optimize their operations and reduce risks, the demand for unmanned driving systems is expected to grow, contributing to the overall expansion of the market.

| Report Metric | Details |

| Report Name | Unmanned Driving System In Mining Areas - Market |

| Forecasted market size in 2030 | US$ 640.2 million |

| CAGR | 3.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Caterpillar, Komatsu, VOLVO, Belaz, Scania, WAYTOUS, Tage IDriver Technology, EQ, BOONRAY, Maxsense Technology, Cidi Server, Xijing Technology, Yuexin Intelligent |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |