What is Vehicle High Pressure Hydrogen Storage Bottles - Global Market?

Vehicle high-pressure hydrogen storage bottles are specialized containers designed to store hydrogen gas at high pressures, typically up to 700 bar, for use in fuel cell vehicles. These bottles are crucial components in the hydrogen fuel cell technology ecosystem, enabling the safe and efficient storage of hydrogen, which is a clean energy source. The global market for these storage bottles is driven by the increasing adoption of hydrogen fuel cell vehicles, which are seen as a sustainable alternative to traditional internal combustion engine vehicles. As countries strive to reduce carbon emissions and transition to cleaner energy sources, the demand for hydrogen storage solutions is expected to grow. These storage bottles are engineered to withstand high pressures and are made from advanced materials to ensure safety and durability. The market encompasses various types of storage bottles, each designed to meet specific requirements and standards. The growth of this market is supported by advancements in hydrogen production and refueling infrastructure, as well as government initiatives promoting clean energy. As the world moves towards a more sustainable future, the role of vehicle high-pressure hydrogen storage bottles becomes increasingly significant in the global energy landscape.

Type I, Type II, Type III, Type IV in the Vehicle High Pressure Hydrogen Storage Bottles - Global Market:

Vehicle high-pressure hydrogen storage bottles are categorized into four main types: Type I, Type II, Type III, and Type IV, each with distinct characteristics and applications. Type I storage bottles are made entirely of metal, typically steel or aluminum, and are the most basic form of hydrogen storage. They are robust and durable but tend to be heavier compared to other types, which can impact the overall efficiency of the vehicle. Due to their weight, Type I bottles are generally used in applications where weight is not a critical factor. Type II bottles are an improvement over Type I, featuring a metal liner reinforced with a composite wrap, usually made of glass or carbon fiber. This design reduces the weight of the bottle while maintaining its strength, making it more suitable for automotive applications where weight reduction is crucial for performance and efficiency. Type III storage bottles take this a step further by using a fully composite structure with a metal liner, typically aluminum, and a carbon fiber wrap. This combination offers a significant reduction in weight compared to Type I and Type II, while still providing the necessary strength to withstand high pressures. Type III bottles are commonly used in light-duty vehicles and are favored for their balance of weight and durability. Finally, Type IV storage bottles represent the most advanced technology in hydrogen storage. They feature a plastic liner, usually made of high-density polyethylene, fully wrapped with carbon fiber. This design offers the lightest weight option, making Type IV bottles ideal for applications where weight is a critical factor, such as in passenger vehicles and buses. The use of a plastic liner also reduces the risk of hydrogen embrittlement, a phenomenon that can occur in metal liners over time. The global market for these storage bottles is influenced by factors such as advancements in material technology, the growing adoption of hydrogen fuel cell vehicles, and the development of hydrogen refueling infrastructure. As the demand for cleaner energy solutions increases, the market for vehicle high-pressure hydrogen storage bottles is expected to expand, with each type offering unique benefits to meet the diverse needs of the automotive industry.

Cars, Hydrogen Refueling Station, Others in the Vehicle High Pressure Hydrogen Storage Bottles - Global Market:

Vehicle high-pressure hydrogen storage bottles play a crucial role in various applications, including cars, hydrogen refueling stations, and other sectors. In the automotive industry, these storage bottles are essential components of hydrogen fuel cell vehicles, which are gaining popularity as a sustainable alternative to traditional gasoline-powered cars. Hydrogen fuel cell vehicles use these bottles to store hydrogen gas, which is then converted into electricity by the fuel cell to power the vehicle. The lightweight and high-strength properties of advanced storage bottles, such as Type III and Type IV, make them ideal for use in passenger cars, where efficiency and performance are paramount. These bottles enable longer driving ranges and faster refueling times compared to battery electric vehicles, making them an attractive option for consumers seeking environmentally friendly transportation solutions. In hydrogen refueling stations, high-pressure hydrogen storage bottles are used to store and dispense hydrogen gas to fuel cell vehicles. These stations require robust and reliable storage solutions to ensure the safe handling of hydrogen, which is stored at high pressures to maximize storage capacity and minimize refueling times. The development of a comprehensive network of hydrogen refueling stations is critical to the widespread adoption of hydrogen fuel cell vehicles, and the demand for high-pressure storage bottles in this sector is expected to grow as more stations are established worldwide. Beyond automotive and refueling applications, high-pressure hydrogen storage bottles are also used in other sectors, such as industrial and aerospace applications, where hydrogen is utilized as a clean energy source. In industrial settings, hydrogen is used for various processes, including chemical production and metal refining, and high-pressure storage bottles provide a safe and efficient means of storing and transporting hydrogen gas. In the aerospace industry, hydrogen is being explored as a potential fuel for aircraft, and high-pressure storage solutions are essential for the development of hydrogen-powered aviation technologies. As the global focus on reducing carbon emissions and transitioning to cleaner energy sources intensifies, the usage of vehicle high-pressure hydrogen storage bottles is expected to expand across various sectors, driving innovation and growth in the market.

Vehicle High Pressure Hydrogen Storage Bottles - Global Market Outlook:

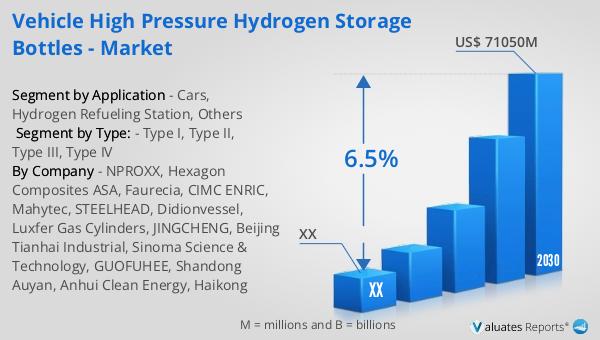

The global market for vehicle high-pressure hydrogen storage bottles was valued at approximately $45,720 million in 2023. Looking ahead, it is projected to reach an adjusted size of around $71,050 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.5% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for hydrogen storage solutions as the world shifts towards cleaner energy alternatives. Industry data suggests that from 2021 to 2050, the cumulative investment in domestic hydrogen refueling stations is anticipated to reach 83 billion yuan. This substantial investment underscores the commitment to developing the necessary infrastructure to support the widespread adoption of hydrogen fuel cell vehicles. The expansion of hydrogen refueling stations is crucial for facilitating the growth of the hydrogen economy, as it provides the necessary support for fuel cell vehicles to operate efficiently. As countries invest in hydrogen infrastructure and technology, the market for high-pressure hydrogen storage bottles is expected to grow, driven by advancements in material science and engineering that enhance the safety and efficiency of these storage solutions. The increasing focus on sustainability and reducing carbon emissions further fuels the demand for hydrogen storage technologies, positioning the market for significant growth in the coming years.

| Report Metric | Details |

| Report Name | Vehicle High Pressure Hydrogen Storage Bottles - Market |

| Forecasted market size in 2030 | US$ 71050 million |

| CAGR | 6.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | NPROXX, Hexagon Composites ASA, Faurecia, CIMC ENRIC, Mahytec, STEELHEAD, Didionvessel, Luxfer Gas Cylinders, JINGCHENG, Beijing Tianhai Industrial, Sinoma Science & Technology, GUOFUHEE, Shandong Auyan, Anhui Clean Energy, Haikong |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |