What is Turbidity Instruments - Global Market?

Turbidity instruments are essential tools used to measure the cloudiness or haziness of a fluid, which is caused by large numbers of individual particles that are generally invisible to the naked eye. This cloudiness is known as turbidity, and it is a critical parameter in various industries and environmental monitoring. The global market for turbidity instruments is driven by the increasing need for water quality monitoring, especially in regions facing water scarcity and pollution issues. These instruments are widely used in water treatment plants, environmental monitoring, and industrial processes to ensure that water quality meets regulatory standards. The market is characterized by a range of products, including portable, desktop, and other specialized turbidity instruments, each designed to meet specific needs and applications. As awareness of environmental issues and the importance of clean water continues to grow, the demand for turbidity instruments is expected to rise, driving innovation and development in this field. The market is also influenced by technological advancements that enhance the accuracy, efficiency, and ease of use of these instruments, making them more accessible to a broader range of users.

Portable, Desktop, Others in the Turbidity Instruments - Global Market:

Turbidity instruments come in various forms, including portable, desktop, and other specialized types, each serving distinct purposes in the global market. Portable turbidity instruments are designed for field use, offering convenience and flexibility for on-site measurements. These devices are compact, lightweight, and battery-operated, making them ideal for environmental monitoring, field research, and situations where immediate results are needed. They are commonly used by environmental scientists, water quality technicians, and researchers who need to assess water quality in remote or challenging locations. The portability of these instruments allows for quick and efficient data collection, enabling users to make informed decisions in real-time. On the other hand, desktop turbidity instruments are typically used in laboratory settings where precision and accuracy are paramount. These instruments are larger and more robust, often featuring advanced technologies and capabilities for detailed analysis. They are used in research laboratories, water treatment facilities, and industrial settings where comprehensive data is required for quality control and compliance with regulatory standards. Desktop instruments offer higher accuracy and a broader range of measurement capabilities compared to their portable counterparts, making them suitable for applications that demand rigorous testing and analysis. In addition to portable and desktop models, there are other specialized turbidity instruments designed for specific applications. These may include inline turbidity meters used in industrial processes to monitor water quality continuously, or specialized sensors integrated into larger systems for automated monitoring. These instruments are tailored to meet the unique needs of various industries, such as pharmaceuticals, food and beverage, and chemical manufacturing, where precise turbidity measurements are crucial for product quality and safety. The versatility of turbidity instruments in the global market is a testament to their importance across different sectors. As industries continue to prioritize water quality and environmental sustainability, the demand for these instruments is expected to grow, driving further innovation and development in the field. Manufacturers are continually working to enhance the performance, accuracy, and user-friendliness of turbidity instruments, ensuring they meet the evolving needs of their users. This ongoing innovation is crucial for addressing the challenges posed by water pollution and scarcity, as well as meeting the stringent regulatory requirements that govern water quality standards worldwide.

Environmental Friendly, Health Disease Control, Industry, Pharmaceutical Industry, Others in the Turbidity Instruments - Global Market:

Turbidity instruments play a vital role in various sectors, including environmental monitoring, health disease control, industry, and the pharmaceutical industry, among others. In the realm of environmental monitoring, these instruments are indispensable for assessing water quality in natural bodies of water, such as rivers, lakes, and oceans. By measuring turbidity levels, environmental scientists can detect changes in water quality that may indicate pollution or other ecological disturbances. This information is crucial for developing strategies to protect aquatic ecosystems and ensure the sustainability of water resources. In health disease control, turbidity instruments are used to monitor water quality in public water supplies and ensure that it is safe for consumption. High turbidity levels can indicate the presence of harmful microorganisms or pollutants, posing a risk to public health. By regularly testing water quality, health authorities can identify potential threats and take corrective actions to prevent waterborne diseases. In industrial applications, turbidity instruments are used to monitor and control processes that involve liquids, such as in the food and beverage industry, chemical manufacturing, and wastewater treatment. Accurate turbidity measurements are essential for maintaining product quality, optimizing processes, and ensuring compliance with environmental regulations. In the pharmaceutical industry, turbidity instruments are used to ensure the purity and quality of liquid products, such as injectable drugs and vaccines. Precise turbidity measurements are critical for detecting impurities that could compromise product safety and efficacy. Beyond these specific applications, turbidity instruments are also used in various other fields, such as agriculture, mining, and construction, where water quality is a concern. In agriculture, for example, turbidity measurements can help farmers assess the quality of irrigation water and make informed decisions about crop management. In mining, turbidity instruments are used to monitor the impact of mining activities on nearby water bodies, ensuring that environmental regulations are met. In construction, these instruments can help assess the impact of construction activities on local water quality, enabling developers to implement measures to mitigate any negative effects. Overall, the versatility and importance of turbidity instruments in the global market cannot be overstated. As industries and governments continue to prioritize environmental sustainability and public health, the demand for these instruments is expected to grow, driving further innovation and development in the field.

Turbidity Instruments - Global Market Outlook:

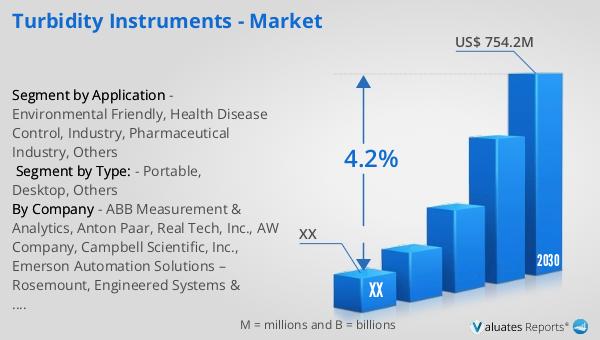

The global market for turbidity instruments was valued at approximately $550.1 million in 2023, and it is projected to reach an adjusted size of $754.2 million by 2030. This growth represents a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2024 to 2030. This positive market outlook reflects the increasing demand for turbidity instruments across various sectors, driven by the growing awareness of water quality issues and the need for accurate and reliable measurement tools. As industries and governments worldwide continue to prioritize environmental sustainability and public health, the demand for turbidity instruments is expected to rise, supporting market growth. The projected growth in the turbidity instruments market is also influenced by technological advancements that enhance the performance and capabilities of these instruments. Manufacturers are continually developing new and improved products that offer greater accuracy, efficiency, and ease of use, making them more accessible to a broader range of users. This ongoing innovation is crucial for addressing the challenges posed by water pollution and scarcity, as well as meeting the stringent regulatory requirements that govern water quality standards worldwide. As a result, the turbidity instruments market is poised for continued growth and development in the coming years.

| Report Metric | Details |

| Report Name | Turbidity Instruments - Market |

| Forecasted market size in 2030 | US$ 754.2 million |

| CAGR | 4.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ABB Measurement & Analytics, Anton Paar, Real Tech, Inc., AW Company, Campbell Scientific, Inc., Emerson Automation Solutions – Rosemount, Engineered Systems & Designs, Inc., Guided Wave, Inc., Hach, Hanna Instruments, Inc., HF scientific, KROHNE Messtechnik, GF Piping Systems, Global Water Instrumentation, Hangzhou Supmea, Harvard Bioscience, Inc., HORIBA Instruments, Inc., Horizon Environmental Engineering, Ltd., Fisher Scientific UK Ltd, Flowserve Gestra, Fluid Imaging Technologies, Forest Technology Systems (FTS), Foxcroft Equipment and Service Company, Inc., Galvanic Applied Sciences, Inc., GEI Works |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |