What is Ultrasonic Hemostatic Knifes - Global Market?

Ultrasonic hemostatic knives are specialized surgical instruments used in medical procedures to control bleeding and cut tissue with precision. These devices utilize ultrasonic energy to generate heat, which coagulates blood and seals blood vessels, minimizing blood loss during surgeries. The global market for ultrasonic hemostatic knives is driven by the increasing demand for minimally invasive surgical procedures, which offer benefits such as reduced recovery time and lower risk of complications. As healthcare systems worldwide continue to advance, the adoption of these innovative tools is expected to rise. The market is characterized by technological advancements, with manufacturers focusing on improving the efficiency and safety of these devices. Additionally, the growing prevalence of chronic diseases and the aging population are contributing to the increased need for surgical interventions, further propelling the demand for ultrasonic hemostatic knives. As a result, the market is poised for steady growth, with healthcare providers increasingly recognizing the value of these tools in enhancing surgical outcomes and patient care.

Disposable, Reusable in the Ultrasonic Hemostatic Knifes - Global Market:

In the global market for ultrasonic hemostatic knives, there are two primary categories: disposable and reusable knives. Disposable ultrasonic hemostatic knives are designed for single-use applications, offering convenience and reducing the risk of cross-contamination between patients. These knives are particularly favored in settings where infection control is a top priority, such as hospitals and surgical centers. The disposable nature of these knives ensures that each patient receives a sterile instrument, thereby enhancing patient safety. On the other hand, reusable ultrasonic hemostatic knives are crafted for multiple uses, provided they undergo proper sterilization between procedures. These knives are often preferred in healthcare facilities looking to manage costs effectively, as they can be used repeatedly, reducing the need for frequent replacements. However, the sterilization process must be meticulously followed to maintain the integrity and safety of the instruments. The choice between disposable and reusable knives often depends on factors such as the healthcare facility's budget, the volume of surgical procedures performed, and the emphasis on infection control. In recent years, there has been a growing trend towards the adoption of disposable knives, driven by the increasing awareness of infection risks and the need for stringent hygiene standards in medical settings. This shift is also supported by advancements in manufacturing technologies, which have made disposable knives more cost-effective and environmentally friendly. Despite the higher initial cost, many healthcare providers are recognizing the long-term benefits of disposable knives in terms of patient safety and operational efficiency. However, reusable knives continue to hold a significant share of the market, particularly in regions where healthcare budgets are constrained, and cost-saving measures are prioritized. The global market for ultrasonic hemostatic knives is thus characterized by a dynamic interplay between disposable and reusable options, with each offering distinct advantages and challenges. As the healthcare landscape continues to evolve, manufacturers are likely to focus on developing innovative solutions that address the needs of both segments, ensuring that healthcare providers have access to the most effective and efficient tools for surgical procedures.

Hospitals, Ambulatory Surgical Centers, Others in the Ultrasonic Hemostatic Knifes - Global Market:

Ultrasonic hemostatic knives are widely used in various healthcare settings, including hospitals, ambulatory surgical centers, and other medical facilities. In hospitals, these knives play a crucial role in a range of surgical procedures, from routine operations to complex surgeries. Their ability to precisely cut tissue and control bleeding makes them invaluable in ensuring successful surgical outcomes. Surgeons in hospitals rely on ultrasonic hemostatic knives to perform procedures with minimal blood loss, reducing the risk of complications and enhancing patient recovery. The use of these knives in hospitals is further supported by the availability of advanced surgical equipment and skilled medical professionals, who are trained to utilize these tools effectively. In ambulatory surgical centers, where outpatient surgeries are performed, ultrasonic hemostatic knives are equally important. These centers focus on providing high-quality surgical care with shorter recovery times, making the efficiency and precision of ultrasonic knives particularly beneficial. The use of these knives in ambulatory surgical centers allows for quicker procedures, enabling patients to return home sooner and reducing the overall cost of care. Additionally, the compact and portable nature of ultrasonic hemostatic knives makes them well-suited for use in these settings, where space and resources may be limited. Beyond hospitals and ambulatory surgical centers, ultrasonic hemostatic knives are also utilized in other medical facilities, such as clinics and specialized surgical units. In these environments, the knives are used for a variety of procedures, including dermatological surgeries, dental surgeries, and other specialized interventions. The versatility of ultrasonic hemostatic knives makes them a valuable asset in diverse medical settings, where they contribute to improved surgical outcomes and patient satisfaction. As the demand for minimally invasive surgical procedures continues to grow, the use of ultrasonic hemostatic knives is expected to expand across different healthcare settings, driven by their proven effectiveness and the ongoing advancements in surgical technology.

Ultrasonic Hemostatic Knifes - Global Market Outlook:

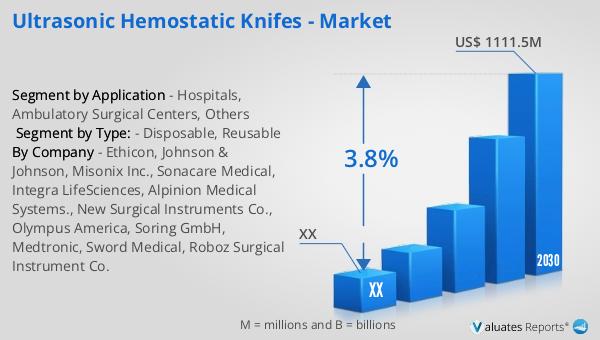

The global market outlook for ultrasonic hemostatic knives indicates a promising future, with the market valued at approximately US$ 875.4 million in 2023. It is projected to reach a revised size of US$ 1111.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing adoption of ultrasonic hemostatic knives in surgical procedures worldwide, driven by the demand for advanced medical devices that enhance surgical precision and patient safety. In comparison, the broader global market for medical devices is estimated to be worth US$ 603 billion in 2023, with an anticipated CAGR of 5% over the next six years. This highlights the significant role that ultrasonic hemostatic knives play within the medical device industry, as healthcare providers continue to seek innovative solutions to improve surgical outcomes. The steady growth of the ultrasonic hemostatic knives market is supported by factors such as the rising prevalence of chronic diseases, the aging population, and the increasing number of surgical procedures being performed globally. As healthcare systems continue to evolve and prioritize patient safety and efficiency, the demand for ultrasonic hemostatic knives is expected to remain strong, contributing to the overall growth of the medical device market.

| Report Metric | Details |

| Report Name | Ultrasonic Hemostatic Knifes - Market |

| Forecasted market size in 2030 | US$ 1111.5 million |

| CAGR | 3.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ethicon, Johnson & Johnson, Misonix Inc., Sonacare Medical, Integra LifeSciences, Alpinion Medical Systems., New Surgical Instruments Co., Olympus America, Soring GmbH, Medtronic, Sword Medical, Roboz Surgical Instrument Co. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |